Cost refers to the expenditure incurred by a producer on factor as well as non-factor inputs for given output of a commodity. It can be categorized into explicit ( Opportunity cost of hiring inputs from the market, measured in cash payments that firm make to others.) and implicit costs. ( Opportunity cost of using self-owned inputs, measured in terms of imputed costs of self owned resources.). It is also termed as selling ( expenditure caused due to promote sale of good.) and production costs ( expenditure on inputs to produce an output.)

Fixed costs are costs related to use of fixed factor of production in short period like, machines, license fee, land expenditure, etc. They do not change with change in output. Variable costs on other hand refer to expenditure by producer on use of variable factors of production like, costs of raw material, wages of workers, wear and tear expense, etc. They increase with increase in output and vice-versa. Graphical representation is given by-

Total cost is defined as sum of variable and fixed costs. Since total variable cost tends to increase at diminishing rate initially, meaning that less and less of additional cost is incurred in every additional output. This happens due to increasing return to a factor and eventually TVC increases at an increasing rate.

Relationship between TVC and MC:

i) Marginal cost is estimated as the difference between total costs of two successive units of output. Thus,

MCn = TCn – TCn-1

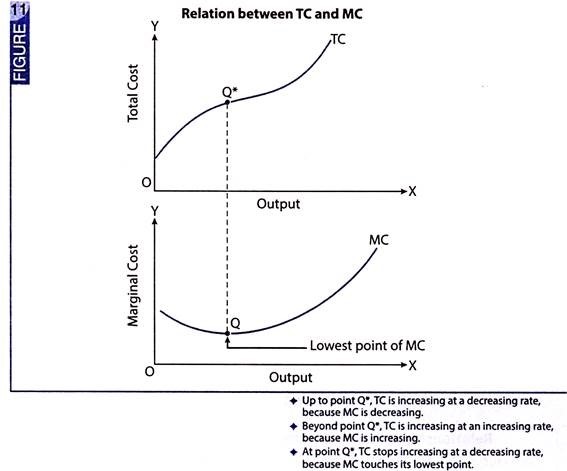

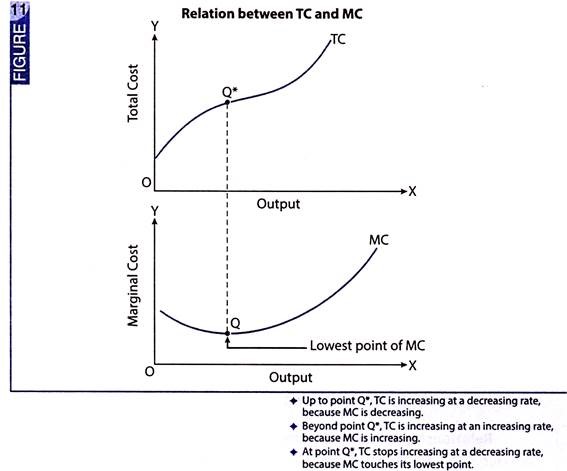

(ii) When MC is diminishing, TC increases at a diminishing rate.

(iii) When MC is rising, TC increases at an increasing rate.

(iv) When MC reaches its lowest point (point Q in Fig. 11), TC stops increasing at a decreasing rate (point Q* in Fig. 11).

Briefly, MC is the rate of TC.

{kind=link}