By Shashikant Nishant Sharma

The Unified Payments Interface (UPI) has emerged as a game-changer in India’s financial landscape, revolutionizing digital transactions. This critical essay assesses UPI’s evolution, highlighting its undeniable success in fostering financial inclusion and empowering users. UPI’s exponential growth, from millions to billions of transactions, underscores its widespread acceptance. UPI faces significant challenges. Security concerns and frauds pose threats, highlighting the need for robust cybersecurity measures. The digital divide and accessibility issues persist, raising questions about equitable access. Transaction costs burden small businesses, hindering widespread adoption. Regulatory complexities and concerns about market dominance call for a more transparent and equitable ecosystem. Additionally, privacy concerns surround the vast amount of transaction data generated. UPI’s impact on India’s financial landscape is undeniable, but it is essential to address its challenges. Balancing convenience, security, and affordability while ensuring accessibility for all, alongside robust regulations and privacy protection, will be crucial for UPI’s continued success.

The Unified Payments Interface (UPI) has emerged as a transformative force in the Indian financial landscape, revolutionizing the way people conduct transactions. Since its inception in 2016, UPI has garnered immense popularity and is hailed as one of India’s most successful fintech innovations. While UPI’s growth and impact on financial inclusion are commendable, it is crucial to critically examine its various facets to understand both its strengths and limitations.

The Rise of UPI

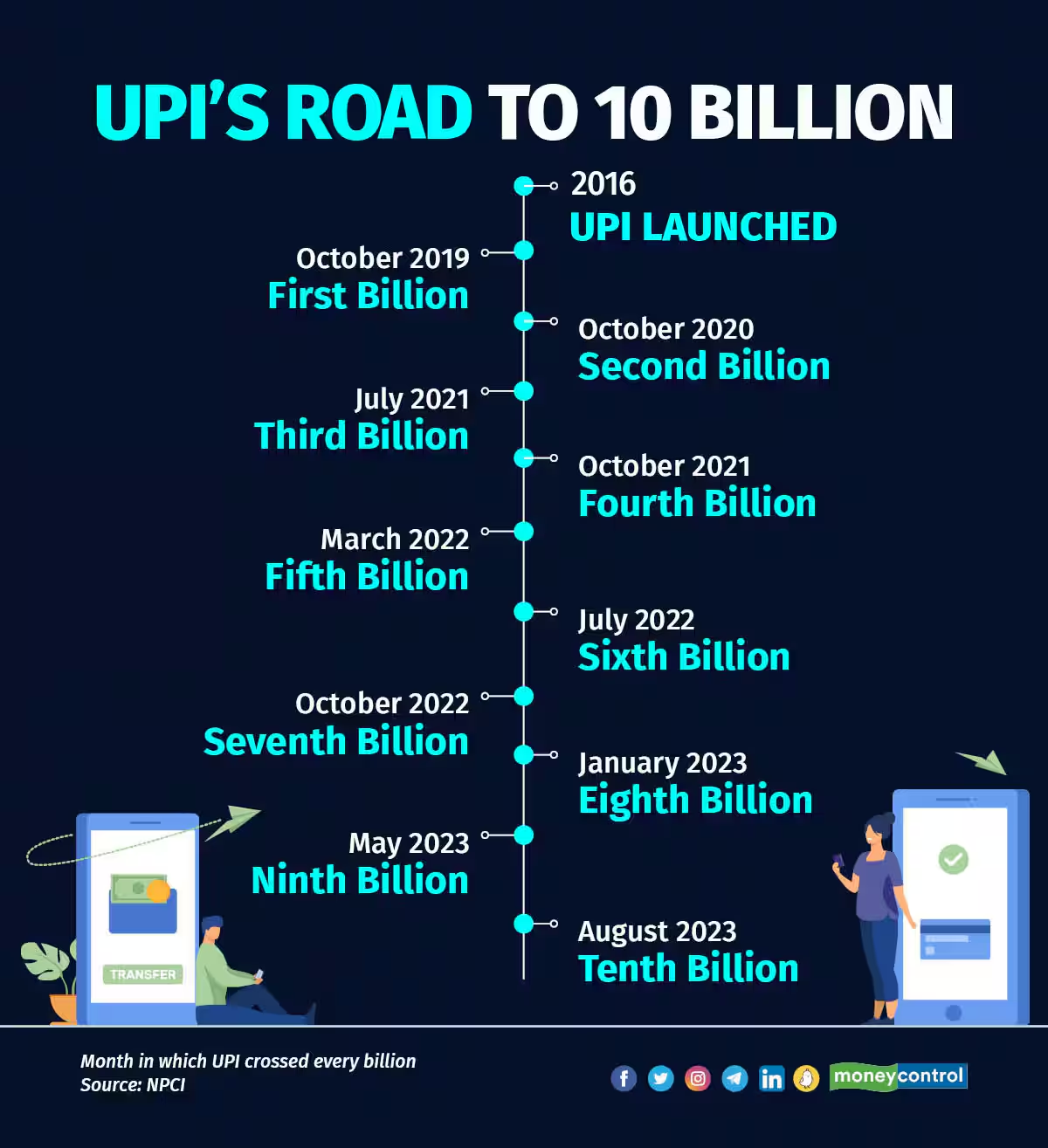

UPI’s success is indisputable. Its user-friendly interface and bank interoperability have made it accessible to millions of Indians. The rapid adoption of UPI can be attributed to its simplicity and convenience, enabling users to send and receive money seamlessly. Its growth from a mere 0.2 million transactions in August 2016 to over 10 billion transactions in August 2023 is a testament to its widespread acceptance.

Financial Inclusion: UPI’s Greatest Triumph

One of the most significant achievements of UPI is its role in furthering financial inclusion. It has allowed people in remote areas to access banking services, make digital payments, and participate in the formal financial system (Daya & Madar, 2018). The Jan Dhan Yojana and Aadhar integration have played pivotal roles in enabling this, but UPI has acted as the vehicle for reaching the underserved.

Security Concerns and Frauds

While UPI offers numerous benefits, it has its share of challenges. Security concerns and frauds have been a growing issue. Despite stringent regulations and guidelines, instances of phishing, social engineering, and unauthorized access have been reported. The ease of transferring funds via UPI has made it an attractive target for cybercriminals (Jajodia & Krishnaswamy, 2017).

Digital Divide and Accessibility

Another critical issue is the digital divide in India. While UPI has made banking services more accessible, it has also left behind a significant portion of the population that lacks access to smartphones, the internet, or digital literacy. The government must address these disparities to ensure that the benefits of UPI reach every citizen.

Transaction Costs and Merchant Concerns

For businesses, minimal vendors, UPI has been a double-edged sword. While it provides a platform for digital payments, the associated transaction fees can be burdensome, particularly for those operating on slim profit margins. This cost factor has led to a reluctance to adopt UPI, which is a concern for the broader goal of a cashless economy.

Regulatory Challenges

The regulatory framework governing UPI needs continuous refinement. Disputes over revenue sharing between various stakeholders and concerns about monopolistic behavior by certain players like Google Pay and PhonePe have highlighted the need for stricter regulation. An equitable and transparent ecosystem is essential to maintain UPI’s integrity.

Privacy Concerns

UPI transactions generate a significant amount of data, which raises concerns about user privacy. The potential misuse of transaction data for profiling or targeted advertising requires robust data protection regulations and practices.

Concluding Remarks

UPI’s emergence in India has undoubtedly transformed the country’s payment landscape and has contributed to greater financial inclusion. However, it is essential to critically assess its impact and address the challenges it faces. Striking the right balance between convenience, security, and affordability, while ensuring accessibility for all, is crucial for the continued success of UPI. Additionally, regulatory and privacy concerns must be addressed to safeguard users’ interests and maintain trust in this revolutionary payment system.

References

- Daya, H., & Mader, P. (2018). Did demonetisation accelerate financial inclusion. Economic & Political Weekly, 53(45), 17-20.

- Jajodia, N., & Krishnaswamy, A. (2017). A Cashless Society, Cyber Security and the Aam Aadmi. Economic and Political Weekly, 35-38.

- Shree, S. (2023). India’s fintech industry and the G20 summit. Economic and Political Weekly, 58(2). https://www.epw.in/journal/2023/2/letters/indias-fintech-industry%C2%A0and-g20-summit.html

- Singh, S. K., Singh, S. S., & Singh, V. L. (2022). The adoption of Unified Payments Interface in India. Economic and Political Weekly, 57 (48). https://www.epw.in/journal/2022/48/commentary/adoption-unified-payments-interface-india.html

You must be logged in to post a comment.