Citation

Danquah, I. O. (2026). The Concept of Susu and its Impacts on Livelihoods; Real Time Financial Investment and Analysis. International Journal of Research, 13(3). https://doi.org/10.26643/ijr/8

Isaac Odoi Danquah

diok1982@yahoo.com

Water Resources Engineer, Goldrain Mountain Company Limited, Koforidua, Eastern Region – Ghana.

ABSTRACT

Great riches and richness level attainment is procedural and is based on the concept of Susu. That is measuring according to your ability, strength, inflows and outflows of money in real life and moving to the next level thoughtfully. Moving to the next level is when there is stability in terms of resources and money and then measuring according to the same ability, strength, inflows and outflows of money in business or life. It becomes a continuous chain or cycle up to the highest point of self-actualization level in life. And finally becoming a seed or seed capital or startup capitals unto others for greatness or richness life attainment. This is the reason for this paper focusing on Susu concept and impacts on livelihoods towards greatness and rich life attainment in life. From this research, it is established that little drops of money make a pool of money for big future projects over a given period. A daily contribution of Gh₵500 or $500 on daily basis gives GH₵15000 or $15000 which is 96.774% as investment returns over a period of 31days from Susu principles. And the remaining 3.226% which is GH₵500 or $500 as commission per head amounting to wages for the Susu operator. This research and investment scenario is applicable to all currencies worldwide.

Keywords: Susu, money, investment, capital, livelihoods, operator, World, Bank, United, Nations, Financial, analysis, inflows, outflows, ability.

- INTRODUCTION

Meeting daily physiological needs is very important in our lives as food, water and shelter can keep mind, body and soul together towards reaching the self-actualization level in life through hard work. This definition and explanation is as indicated by the Maslow’s hierarchy of needs. Everybody on the planet earth who is serious in life and has greatness attainment instinct or have the eagerness attitude to make it in life or meet basic needs gets himself/herself with work on daily basis. With this in mind, everyone is a worker whether consciously aware or unconsciously aware of this fact. Even the illegal gold miner is working. This is justified by the declaration, I am going to work as everyone says to someone as he/she lives the house on daily basis. As for the size of the work; wages level, time spent at the work place; wealth generation level at the end of the year, experience level etc. Everything about it is work and the final justification is the wages amount or gross income or net income quantified in terms of real money terms that lands in the bank account at the end of the month is the final output. One main difference in here is the quantification in terms of government work, private work or private business.

Everybody in life receives salary at the end of the month. Whether young or old. The only exception here is justified for that little baby still breastfeeding but the little boy or girl who can talk is also a worker in one way or the other according to a school of thought. As a little girl in the house who sweeps, prepares dinner, fetches water, goes to the market and comes back with all necessary accoutrements for the kitchen and fills the fridge with all kinds of activities, drinks and vegetables does this on daily basis to the end of the month is working. The various task and activities done by this teenager is comparably same to the task and functionality of an employed maid in the house. The task executing ability and functionality of such a girl throughout the month is the same as the maid whose wages or salary will be quantified in real money terms at the end of the month in her account at the Bank. Is this little or teenage girl also not working? Can one not quantify her monthly wages or earning in terms of school fees paid by the father, mother or person she is living with. Is she not going to be feed throughout the month, can one talk about the shelter, health needs, clothing’s, having or living a luxurious life comparable to a graduate who is living in a single room and starting life on his/her own? Or again comparable to an employed graduate who is starting life and now living in a single room and having access to one student mattress with one bucket for water? And even a possibility of not even receiving the first 3 months salary or pay check and hence unable to feed but has to employ the concept of Susu. And that concept of Susu is measuring life at that point according to the inflows and outflows of money into his account or life? Such a little or teenage girls can also be seen as worker or employer by the mother, father, teacher, grandfather, grandmother or person who he or she is living with. Since she is going to work or get things done throughout the month and most of the activities done or accomplished by her will not be done by the father, mother or grandfather. So in a way she is functionally executing all kinds of task and getting work done which will have been the task and roles for a maid in the house. And employing such a maid is based on the concept of Susu. As the gross income or net income for a maid working in a very self-made rich man house will not be the same as the wages/salary in an average income earners rich man house in life.

Susu basically is the ability to measure for an outcome based on intelligent level, resources, inflows and outflows of money or accoutrements towards attainment of an output in life. In terms of finances and banking, Susu is measuring according to once strength, ability, intelligent, the inflows and outflows of money in business. The concept of Susu has been used over the years on daily basis towards saving of money to meet basic physiological needs as determined on the Maslow’s Hierarchy of needs. Everything about life is money and especially in the case of business running and banking, the money needs to be used intelligently and well accounted towards sustainability in business.

The concept of susu has helped a lot of people especially the low-income earner who makes money on daily basis through trading and not having a huge quantum of money for business. So with daily contributions into a susu business or account is subject to receiving some sizable amount of money or huge sums of money which can generate a huge output of results in the future.

This is basically the reason for this research paper at Nsutam and Bonsu communities as one investigates little drops of money forms pool of money towards great projects or great tasks executing in the future. Or on the other hand is looking at the susu concepts and its impacts on livelihoods at Nsutam and Bonsu as one invests a good sizable amount of money on daily basis for a period of thirty-one (31) days and earns a monthly income. This monthly gained income is towards further monthly investments or great tasks or project accomplishments in life. And finally looking at the possibility of obtaining tax component as a government and simulating it over the whole wide world as United Nations and World Bank Project for all. It will be beneficial to all mankind worldwide if one thoughtfully thinks through it so that it can be implemented for every country where taxing the business man/woman or trader is very difficult. This will give funds or money to create jobs for now and future generations.

- SUSU CONCEPTS AND ASSESSMENTS OF IMPACTS

2.1 Susu Concept

Susu has been part of Ghana’s micro financial system for at least three centuries (Williams, 2006; Anku, 2013). It forms part of the financial phenomena occurring beyond the functional scope of countries’ banking and other financial sector regulations (Jones et al., 2000; Aryeetey, 1998). Susu is an informal savings mobilisation mechanism where individual savings collectors help savers accumulate savings through daily deposits in consideration of a day’s activity or business of work. It involves a regular pickup of cash with unrestricted rights to withdraw it at a later date (Ashraf et al., 2005; Aryeetey et. al., 1995; Aryeetey 1994; Anku, 2023). Susu is commonly referred to as susu or esusu in West Africa where it is very popular (Alabi et al., 2007; Aryeetey et al., 1995). In Twi, Susu specifically means to measure accordingly to whatever adventure one involves himself or herself in. Central to the susu system is the provision of saving schemes to depositors, purposely to help them accumulate their savings over periods ranging between one month and two years. Even though credit is not the main objective of susu, it is quite common for depositors to be advanced when talking about crediting by a banking facility (Steel et. Al., 2003; Aryeetey, 1994; Anku 2013). In 1997, The World Bank’s report on informal financial markets and financial intermediation in four African countries observed that some susu collectors sometimes advanced monies to their clients before the end of the agreed period. (World Bank Group, 1997). Susu operates primarily on the savings side of the market and is based on a simple system devoid of bureaucratic procedures and complex documentation. It is operated by collectors who are mostly men operating from kiosks which are usually located in the markets. Other Susu operators also go rounds when it comes to daily collection from susu clients or contributors. The collections are often of low but regular value and are usually kept by the collector for each of his clients until the accumulated amount, minus one day’s collection (3.226%) out of 100% (which is 31days of work per head), and 96.774% is returned to the depositor or client. Whilst some collectors hold onto savings collections for safe keeping, others deposit them in their bank accounts. Others still invest them in their businesses or lend them to others (Jones et al 2000; Aryeetey 1994; Anku et al., 2013).

2.2 The Concepts of Susu in Ghana and World

The concepts of Susu have been in existence over several years and I personally an encounter and as a worker in the 2000’s. In Ghana alone, only 5% to 6% of the population is reported to have access to formal banking facilities (Basu et al., 2004). Micro and Small Enterprises (MSEs) are commonly believed to have very limited access to deposits, credit facilities and other financial support services provided by Formal Financial Institutions (FFIs). This is still same in the 21st century and in the Fanteakwa South district as most traders and people have to travel to another town or city before deposits can be made especially during international business transactions. And most traders and business men/women embarking on this on daily basis results in losses when talking about profits and losses in trading or business (Alabi et. al., 2007). The lack of formal banking facilities underpins the development of MSEs to a very large extent. This has serious implications for a country like Ghana where the economy is largely characterized by Micro and Scale Enterprises (MSEs) (Basu et al., 2004). The concept of Susu among the indigenous traders or market women solves this problem as most can access seed money or capital for the next business transaction or buying at the market, get a loan facility to expand business, or the possibility of releasing some sizable quantum of money as startup capital for a needy woman who approaches them for help or being employed in the buying and selling business (Alabi et. al., 2007). The troubling and pressures associated with money and accessing credit facilities from formal systems compel the poor and informal business enterprises to resort to different non-banking and informal arrangements to access funds for their operations and Susu among the traders is one of the strong determining platforms for accessing huge loans that amounts to GH₵20,000 for instance. Informal Financial Institutions operating outside the scope of banking laws and regulations in Ghana include money lenders, rotating savings and credit associations (ROSCA), and Susu savings collectors. These informal financial systems commonly assist Small Business Enterprises (SBE’s) or Medium Scale Enterprises (MSE’s) particularly, market traders, house wives and artisans to accumulate funds through daily or weekly deposits that are returned at the end of a specified period minus a small fee (World Bank, 1994). These arrangements are based on the ‘Susu’ system. The ‘Susu’ system requires no collateral and operates on a predetermined interest rate averaging 3.2258% – 10% depending on the type of Susu savings or money lending business philosophy (Alabi et. al., 2007).

2.3 Susu as a Sourcing Financial platform for SBE and MSB’s

One of the main sourcing financial platforms holding the trading, buying and selling business in Ghana and worldwide is the Susu Investment Business. With this opportunity, the Small Business Enterprise (SBE’s) and the Medium Scale Business (MSB’s) accesses principals, seed money or capital money, profits and loans for business startups for oneself and for others (Alabi et. al., 2007).

In the absence of Bank facilities and other formal sources, “Susu” has been a major source of fund mobilization for many Small Business Enterprise (SBE’s) and Medium Scale Business (MSB’s) in Ghana (World Bank, 1994). “Susu” is believed to have contributed largely to micro enterprise and small businesses enterprises, guaranteeing the depositors of “Susu” companies’ loan advances for their clients after some period of regular deposits normally six months. The 21st century has seen the Susu Business or cooperative in a better way as most are housed in a better business housing facility for better functionality towards financial gains and accomplishments (Alabi et. al., 2007). Susu is a financial gaining platform for immigrants to establish crediting and debiting instrument in an economically adverse environment. Historically, indigenous savings strategies represent the continuation of economic self-help, which indentured Africans brought to the U.S based on practice and experience to advance their lives in new land or world. Susu has evolved over the years in Ghana. A major component of finance for urban poor entrepreneurs in Ghana, particularly apprentices and artisans has been the daily or weekly contribution of fixed amounts through “susu”. These savings are accessed after a period of time for purchasing tools and equipment necessary for setting various artisans up in their vocational practices. Artisans who normally benefit from these include seamstresses, tailors, hairdressers, fitting mechanics, welders and carpenters among others. For many petty traders, market women, apprentices and artisans, “susu” is believed to have been a trusted, reliable and friendlier means of getting started and also for sustenance as well as growth of their businesses. “Susu” in some cases is believed to be the sole source of getting established for livelihood (World Bank, 1994). Barclays Ghana calls it the “Ghanaian Microfinance” and describes it as an unconventional mobile initiative which extends microfinance to the least affluent in Ghanaian society (Alabi et. al., 2007).

2.3 Susu and Impacts on Youth livelihoods in the Economy

Adulthood is one school of thought overwhelmed by a set of challenges that are not exempt from the youth of Ghana as we all are subject to old age one day. Questions, problems and focus on young people have become a global concern in 1965, when the General Assembly (UN) United Nations adopted the Declaration on the promotion of youth, gender equality, the right to peace, mutual respect and coordination between people; important role hammering young people in today’s world, especially its development costs (UNDPI 1995) (Ofoli, 2015). Young people and their problems have amassed considerable attention from all sectors of the national economy, despite a mantra with little or no understanding of their true ability to national development and how to deal with them as a government. It is on this basis that empowering the young entrepreneurs in Ghana is considered essential for the country’s economic progress (Ofoli, 2015). The youth of every country are very important and hence the need to have a little opportunity for them to anchor or attached great faith around it towards future greatness attainment or enrichment in life.

Traditional financial houses or institutions are indifferent to extend lines of credit to individuals, including youth, because of the risk of law and trapped in business performance that requires little capital, they are also unable to provide the necessary guarantees. This is due to no job, no savings or investment, no collateral and hence justified by the bank or investment institutions not to give in for such commitment as it could result in crush or collapse of their financial institutions (Ofoli, 2015). Susu microfinance programs therefore performs an important role in improving decision through participation in economic decision youth activities such as artistic job creation activities. Microfinance, advancing microcredit and other financial needs of the working poor economy, generally considered the key over the past decades of creation two and a half in terms of how to expand to poor and vulnerable populations (Montgomery Weis, 2006) including young entrepreneur in Ghana. Microfinance savings in terms of progress and has the power to convince young entrepreneurs in improving low developed nations (Schreiner et al., 2001). Low developed nations without resources to establish microfinance institutions or banking sectors highly depends on susu concept for daily and monthly savings, loans and investments. With the inception of the susu concept and its availability to the youth in Ghana today, it has created grounds to access the micro, small and medium enterprises in communities. It allows the entrepreneurs more importantly the youth entrepreneurs to get involved in banking transactions which in effect builds up the economic growth of the citizenship. The social lives of this cluster of people are also enhanced as a result of the susu scheme which enables them to save towards other livelihoods and or monetary demands (Ofoli, 2015).

2.4 Susu as Savings for Net Income or Gross Income

Contribution, investing or savings on daily basis amounts to monthly wages, salary or income. Analysing this or computing on the basis of monthly worker or government earner is justified and can easily amount to a gross income and through deductions for various commitments ends it as net income for the susu contributor. Susu is a popular form of savings in most developing economies. It is practiced in different forms and under different names and conditions in both developing and developed countries. In spite of its contribution to the Gross Domestic Products (GDP) and socio-economic development of both developing and developed countries, it remains under-researched. It shows that Susu is a complex and dynamic social phenomenon. It is discovered that susu shares similarities with other micro savings schemes such as rotating savings and credit schemes, accumulating savings and credit associations as well as Christmas hampers and Christmas clubs in England and the United States respectively. It establishes that similar to other micro savings schemes, the objective, aims and goals of Susu is to help rural, poor and low-income earners meet their economic, social or communal needs. This is because at the local rural settings or level, it is difficult to find a formal financial institutions (rural bank) or banking sector for financial transactions. It is even possible that one may not find a rural bank or international banks in some districts in Ghana in this 21st century (Ofoli, 2015).

2.5 Susu as an Association to improve Livelihoods

Micro savings in Ghana covers both Susu and group savings schemes also known as susu associations. The group schemes usually operate in the form of rotating savings and credit associations (ROSCAs) and accumulating savings and credit associations (ASCRAs) (Aryeetey et al., 1995). Steel and Andah (2003), in their study of rural and microfinance regulation in Ghana, identified two additional types of susu savings schemes which they described as susu clubs and susu companies (Anku, 2013). Amongst existing micro savings schemes, susu is the most prominent and widely participated by both low- and middle-income earners in Ghana (Anku, 2013). This is due to inability to access financial institutions for daily business and money transactions. The collectors mobilise a great deal of savings albeit without being prudentially regulated by any governmental body (Steel et. al., 2003). As a microfinance activity, micro savings form part of the financial component of informal economies. Portes, Castells & Benton (1989) refer to this as a phenomenon unregulated by the institutions of society in a legal and social environment in which similar activities are regulated. This is not the case in this 21st century as Ghana Co-operative Susu Collectors Association is regulating and cooperatively controlling the Susu Business under authorization by Bank of Ghana (BoG) even though there are some aspect of irregularities. The irregularities here is the Susu operators not going through registration process and operating illegally. The susu business or banking sector is improving lives positively as huge sums of money are obtained on daily, weekly and monthly basis to solve problems addressed by great banking sectors or institutions. (Anku, 2013). Little (1957) also identified friendly societies including the susu of Yoruba origin. The aim of these societies was limited to mutual aid and benefit to its members. In Ghana, he observed that the Nanamei Akpee society headquartered in Accra had over 400 members, most of whom were educated or semi-literate women readers. Members of this group paid monthly subscriptions for funeral expenses and other engagements like weddings (Anku, 2013).

- Research Zone and Area for Data

The investigating area for this study is at Nsutam and Bunso in the Eastern Region of Ghana. The people of Nsutam and Bunso are involved in gold mining activities, farming, trading. Cocoa Research Institute of Ghana has its activities which looks at various processes involved in the Cocoa industry at Bunso. Some of the farm products produced includes coconut, cocoa, plantain, yam, cassava, sugar cane, cashew nuts and all kinds of vegetables produced during the farming seasons. The huge amount of gold discovered in the Nsutam community has resulted in all kinds of illegal gold mining activities destroying water bodies, forest and lands. The Bunso Junction is the main point or centre stage when it comes to petty trading and Susu business. The Bunso junction is serving as taxi ranks or station for all kinds of travelling in and out of Nsutam and Bunso and for those going to Accra, Kumasi and beyond. The Nsutam community has a population of about 7000 (2021 population census) with the majority being immigrants due to the gold mining business, Linda Dor and Paradise Tourist business operations in the community. The Bunso community has the GPS address E5-1774-2247 at a point in Bunso and Nsutam community four has the GPS address E6-976-6246 at point in Nsutam. This GPS is in accordance with Ghana Post GPS in Ghana.

The illegal gold mining business at Nsutam has destroyed a lot lands resources, water resources, aquatic life’s, forest reserves, has resulted in relocation of most indigenous, leaving people faithless in the future in this 21st century, etc. The destroyed land needs reclamation process in order to restore the infertile lands back to more fertile rich soils which will support plant growth in order to support the hydrological cycle and exchanges of oxygen and carbon dioxide between man and plants. Restoration of the degraded lands will also promote afforestation and wildlife existence in the future for future generation and finally crop production. With high yields and better crops, petty trading among the people will be enhanced. Then one can think of doing business and resultant Susu business among all people in the two communities. It will also promote tourist attraction when vegetation’s are groomed and protected with the existence of wildlife’s. Danquah (2023) elaborates on how some of these illegal gold mining sites that have been destroyed can be converted into Eco parks as a tool to reclaim degraded lands whiles making money to help oneself and community and Ghana as a whole. The illegal gold mining canker coupled with the effects and impacts of ‘Akatie’ has affected the Cocoa business drastically and final output on the international market as whole.

Fig. 1: Map Showing the Study area Communities of Nsutam & Bunso

- Research Findings and Output

4.1 Susu as Driving force for Traders

Since the inception of daily or weekly susu in the lives of traders at community four, great quantum of wealth and big projects realization has been achieved to a greater extent. The new free senior high school education in Ghana has lessened the burden on parents and guardians. If not, the Susu concept and approach would have been one of the main key parameters to deal with offsetting, school fees, loans and financial burdens. Research findings indicates that petty traders are very much interested in the susu business as most have amassed wealth since its inception. A Susu business which started in March 2025 with 35 clients now stands at 365 clients regardless of being in good standing or not. This is just comparable to banking institutions setting as some people are always working with banks whiles others goes redundance or have the red line when the account becomes dormant. The good standing of the Susu accounts and redundancy has to do with business operations intelligence, the inflows and outflows of money in business, business advices, migrations issues, change of trade or trading interest and others. Depicted in the Table 1 & 2 below is the enrolment patten for the clienteles at Nsutam and Bunso into Glory Susu Business in Ghana.

Table 1: Clients Enrolment on monthly Basis [March – Aug. 2025]

| MONTH | March | April | May | June | July | Aug |

| № Of Clients | 35 | 97 | 157 | 190 | 199 | 212 |

Table 2: Clients Enrolment on monthly Basis II [Sept. – Feb. 2026]

| MONTH | sept | oct | nov | dec | jan | FEb | |

| № Of Clients | 125 | 266 | 290 | 302 | 332 | 365 | |

From the two Tables above, one can easily see that, Glory Susu at Nsutam started with 35 clients in March 2025 and cumulatively increased on monthly basis and currently at 365 in February 2026. Even though some have clients are not investing on monthly basis, it is comparable to banking sector activities, actions and inactions and impacts. Table 2 recorded decrease in number of clients due to some challenges faced in August after recording a total clientele of 212. Fig 2 below gives graphical representation of the various clientele registration for this research.

Fig 2: Clients accumulation against months of investing in Susu Business

4.2 Loanable funds and impacts

Life is all about relationship and depending on others before independence towards self-sustainability and accountability. And so is the reason for loaning unto another in business, for a project, for a transaction, towards a startup capital. As a mother loans her time, business and money to her baby till adulthood and working time, so will the child who becomes a parent one day loans her time, money and engagement to the mother at her old age.

With this declaration one will definitely go for a loan from an international bank, rural bank, microfinance or from Susu operator. And Glory susu is also involved with loaning to its real customers. Availability of resources either quantified in terms of money or goods and services is one of the main reasons for loaning unto other. By this assertion, even very rich and developed countries do go for loans from underdeveloped countries and these are usually quantified in terms of state resources and its availability.

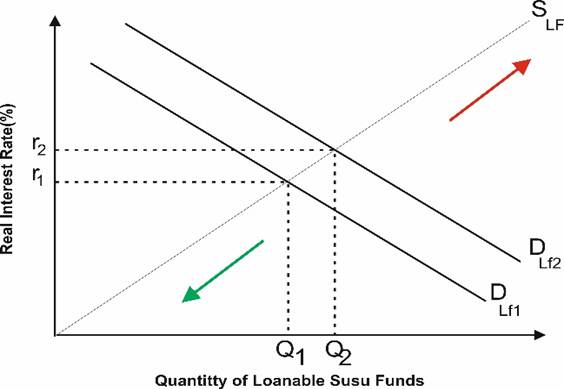

The loanable funds theory says that market interest rates are determined by the demand and supply of loanable funds rather than just money supply. Supply comes from susu savings and bank while demands is from investment into factories, business, machinery and individual borrowing for large purchases. From Fig 3, it can clearly be seen that as demands for loans from the Banks, from microfinance institutions and from Susu groups increases, interest rates goes high (shift from r1 to r2)). This is seen in the red arrow sign on the diagram above and once such things happens, then there will a lot of pressure in the system as more money are generated in the direction of banks and financial institutions. Traders will get little money after obtaining loanable funds for business at high interest rates and will be expected to pay more money to offset huge amounts of loans obtained from the banks. That will have negative impacts or effects on the Gross domestic Product (GDP) in the country.

On the other hand is the green arrow as can be seen in the diagram below. In a situation where people are willing to start business on loans and work assiduously towards living and doing business without loans over a period of time? Then there will be little pressures on banks, microfinance institutions and on susu groups when it comes to accessing loans for business. In that regard, the banking sector will have no option than to reduce interest rates on loans (shift from r2 to r1) and loanable funds will be low. Loanable funds will be low since just a few business men and business women will be approaching loans for business and transactions. And lower and further will the interest rates be as the number of business men/women approaching loans for business will be on a low rate. And hence a justification for low interest rate on the Fig. 3 below. This will see the green arrow in the diagram generating positive results on the economy when it comes to GDP as buying and selling of goods and offering of services, exchange rates will be on the low side. Such conditions in a country usually results in harsh governance but usually yields results for a country which is yearning towards self-independence and self-sustainability. This policy and governance goes for countries willing to build its own country and by that begins on the platform by making use of its internal natural resources and accoutrements and a country like Ghana yearning to be a country comparable to USA, Hong Kong, Germany as an independent developed country needs to do same in this regards towards national development to international standards in this 21st century.

Fig 3: Loanable Susu Funds and Interest Rates determinants

4.3 Glory Susu Loanable Funds

Table 3 below is explaining the Susu mobilization loanable funds that was accessed by Susu clienteles from July 2025 to February 2026. With Glory Susu and her aims and objective of enrichment unto now and future generations, various needs and demands are met on daily basis through the Glory Susu loan scheme.

Table 3: Charting Loanable funds to Glory Susu Clienteles

| MONTH & YEAR | LOANABLE AMOUNT (GH₵) | PAID FULLY |

| July 2025 | 19,000 | Paid |

| August 2025 | 8,900 | Paid |

| September 2025 | 9,600 | Paid |

| October 2025 | 6,200 | Paid |

| November 2025 | 13,500 | Paid |

| December 2025 | 23,600 | Paid |

| January 2025 | 22,570 | Paid |

| February 2025 | 41,070 | Month Under Review |

Loans from Glory Susu and most Susu operators are interest free for now as all clienteles are seen as part of the principal money or seed capital generating process.But the concept of ‘Susu’ still remains a goal and objective that is always used in every process of business transaction as loans are even given according to once or clienteles inflows and outflows in business, ability to contribute or save to the end of the month. And the principle of do unto others what you want others to do unto you is also another great principle and objective that is used in this business. The least amount of loan given so far as can be seen in the Table 3 is GH₵6,200 in the month of October 2025 and the highest is GH₵41,070 and that is in February 2026 which is the month under review. Various needs and demands are met whenever such loans are accessed at Glory Susu. This includes; as startup capitals for various businesses, education, travels, purchasing of lands, buying of cars/Tricycle (Pragia/Aboboya’s), renting of building appartments or housing systems, completion of building projects etc. All such projects are withing the jurisdiction of the United Nations and World Bank as various Sustainable Development Goals are met towards the goodwill of mankind. I strongly believe as clients acquire these loan facility to meet various demands, it’s their utmost aim of trying to work and live off loans in the future towards self-independence and self-sustainability just like the Sustainable development goals of the United Nations are met with serious work of addressing all needs worldwide.

4.4 Glory Susu Philosophy and Impacts on Livelihoods

Glory Susu and Susu in general wealth generating process basically involves investing an appreciable amount of money on daily basis for 31 days to obtain a return of 96.7742%. The remaining 3.2258% becomes the commission per head accumulating into monthly business profits or wages based on number of customers or clients engaged within that month. The interesting concept involved in the Glory Susu Investment is releasing or investing the money without feeling the economic value and hardship in the economy basing it on the amount of money invested per day. But the happy moments is the total amount of money generated at the end of the month with the sustainability of the business or operating shop not affected to any degree. With the GLORY SUSU INVESTMENT concept is the MINISTRY OF GOLDWAY establishment in government and as a world UNITED NATIONS and WORLD BANK project to serve now and future generations. For instance, an egg seller can contribute Gh₵30 and earn Gh₵900 with the remaining Gh₵30 generated as commission/wages for Glory Susu. On the high level will be the contribution of Gh₵400 to earn Gh₵12000 at the end of the month as sampled and indicated in Table 4. Glory Susu is for anyone willing to reap bumper harvest of money at the end of the month and not afraid of little drops of money makes a pool of money. Everyone has a philosophy or principle upon which his/her huge mansion is built. God believes in laying a strong foundation, laying the first basic unit block and using six days to create the world and finally resting on the seventh day. This is the philosophy of Glory Susu even though working in Glory susu is seven days in a week and 31days in a month.

Table 4: Sampled invested amount and Returns for Client and Glory Susu

| Type of Business | Daily Investment [Gh₵] | 31 days period Total Earning [Gh₵] | Investor Profit [96.7742%] [Gh₵] | Glory Susu Profit [3.2258%] [Gh₵] |

| Egg Seller | 30 | 930 | 900.00 | 30.00 |

| Hair Stylist | 40 | 1240 | 1200.00 | 40.00 |

| Shop Owner | 100 | 3100 | 3000.00 | 100.0 |

| Spot Owner | 200 | 6200 | 6000.00 | 200.0 |

| Wakye Seller | 500 | 15500 | 15000.0 | 500.0 |

| Distribution Points | 700 | 21700 | 21000.0 | 700.0 |

Table 4 gives the clear understanding and various scenarios that can be generated under different investing amounts and the appropriate end of month returns for investors and Glory Susu.

4.5 Glory Susu and its Projections for United Nations and World Bank and impacts

But this same concept can be used to generate income or wages for the seller or trader on monthly basis and effectively generate tax for government projects in Ghana and worldwide. This is where this Glory Susu concept and project is seen as UNITED NATIONS and WORLD BANK project for now and future generations and the establishment of ‘MINISTRY OF GOLDWAY’ WORLDWIDE. This will be collaboratively done with Ghana Revenue Authority and revenue collectors and simulated though out the world as a WORLD project for all. With this understanding, a monthly return after an appreciable amount of investment on daily basis based on measuring investment capability based on business size, inflows and outflows of money in business will be obtained.

Table 5: Sampled invested amount and Returns for Client (workers), Government and for project owner(s)

| Type of Business | Daily Investment [Gh₵] | 31 days Earning [Gh₵] | Investor Profit [83.4%] (Gh₵) | GoG and Project Owner % [16.6% ] Tax Rate (Gh₵) |

| Egg Seller | 30 | 930 | 775.62 | 154.38 |

| Hair Stylist | 40 | 1240 | 1034.16 | 205.84 |

| Shop Owner | 100 | 3100 | 2585.4 | 514.6 |

| Spot Owner | 200 | 6200 | 5170.8 | 1029.2 |

| Wakye Seller | 500 | 15500 | 12927 | 2573.0 |

| Distribution Point | 700 | 21700 | 18097.8 | 3602.2 |

After which there will be a Tax Component out of total amount generated in 31days into government account for government projects and project owners task executions. This is expatiated for better understanding in Table 5 below towards decision makings and conclusions.

- Conclusion

From one school of thought is little drops of water to make an ocean of water and little drops of money to make a pool of money towards great riches and great project or objectives attainment in life. This is the same concept of little drops of money resulting in a pool or quantum of money towards addressing specific needs and objectives within a time frame. This is the Susu concept in Ghana and foundation philosophy of Glory Susu at Nsutam, Ghana and Worldwide. And from the great riches and success story of Glory Susu to the United Nations will be to address the 17 Sustainable Development Goals of the UN worldwide. Great height attainment in a procedural way and through good standard operating procedure in the financial sector will be attained and great riches generated for all. By simulating this GLORY SUSU and INVESTMENT concept as UNITED NATIONS and WORLD BANK PROJECT under a ministry called the MINISTRY OF GOLDWAY is the ENRICHMENT UNTO GENERATIONS and peaceful creation of a world unto all worldwide for now and unborn generations.

Acknowledgement

Grateful I am to the Most High God for this divine wisdom and revelational knowledge towards the goodwill of mankind worldwide. I am grateful to my Wife, Rita Darko, two sons; Gates and Michael for their support and motivation. I am thankful to the Danquah family at Nsutam and Darko family at Kukurantumi for their encouragement and Support. I am so grateful to GLORY SUSU and her clienteles at Nsutam, Bonsu, Ghana and World wide for given me the opportunity and for being part of this United Nations and World Bank Project. Grateful I am also to the government of Ghana and the governing body. My final appreciation and thanks goes to the United Nations and World Bank worldwide. I am again grateful to Internation Journal of Research, pen2print in India and UK and all their branches worldwide. Bravo!! Hurray!! To us all. Stay blessed.

References

- Alabi J., Goski A., Ahiawodzi A., (2007), Effects of ““Susu”” – A traditional micro-finance mechanism on organized and unorganized micro and small enterprises (MSEs) in Ghana, African Journal of Business Management Vol.1 (8), Pg. 201 – 208.

- Alabi, G., Alabi, J. and Akrobo, S.T. 2007, ‘The Role of “Susu” A Traditional Informal Banking System In The Development of Micro And Small Scale Enterprises (MSEs) In Ghana’, International Business and Economics Research Journal, vol. 6, no. 12.

- Aryeetey, E. 1994, Informal Savings Collectors in Ghana, Can They Intermediate? Finance and Development Magazine, [Online] Retrieved on 4th September, 2006, Available at: http://www.allbusiness.com/public-administration/national-security-international/433294-1.html

- Aryeetey E. and Udry C. 1995, ‘The Characteristics of Informal Financial Markets in Africa’, Plenary Session of the Bi-Annual Research Conference of the African Economic Research Consortium, Nairobi, Kenya.

- Aryeetey, E. 1998, ‘Comparative Developments in African and Asian Financial Markets’, Research Newsletter Issue A, May, African Economic Research Consortium.

- Aryeetey, E. 1998, ‘Comparative Developments in African and Asian Financial Markets’, Research Newsletter Issue A, May, African Economic Research Consortium.

- Anku, O. T., 2013, Susu: A Dynamic Microfinance Phenomenon in Ghana, University of Ghana, Business School Department of Organization & Human Resource Management, Journal of Economics and Sustainable Development, Vol.4, No.3.

- Ashraf, N., Karlan. D. S. and Yin. W. 2005, Deposit Collectors, [Online] Retrieved on 26th March, 2006, Available at: http://people.hbs.edu/nashraf/DepositCollectors.pdf

- Basu A, Blavy R, Yulek M (2004). Micro finance in Africa: Experience and Lessons from IMF International Monetary Fund.

- Jones, H., Sakyi-Dawson, O., Hartford, N. and Sey, A. 2000, Linking Formal and Informal Financial Intermediaries in Ghana: Conditions for Success and Implications for RNR Development’, Natural Resources Perspective, no. 61, Overseas Development Institute.

- Ofoli T. J., (2015), The effects of ‘susu scheme’ on the economic empowerment of youth entrepreneurs within the Kumasi metropolis, Ghana , Research Gate.

- Steel, W. F. and Andah, D. O. 2003, Rural and Micro Finance Regulation in Ghana: Implications for Development and Performance of the Industry, Africa Region Working Paper Series, no. 49.

- Stoesz D., Gitau I, Rodriguez R., Thompson F., 2016, Capitalizing Development from the Bottom-Up Susu: Capitalizing Development from the Bottom Up, Kean University, Journal of Sociology and Welfare, Article 8, Volume 43, University, dstoesz@kean.edu.

- Schreiner M., Colombet, H.H. (2001) Microfinance, Regulation, and Uncollateralised Loans to Small Producers in Argentina in Douglas R. Snow, Terry Buss, and Gary Woller (eds) Microcredit and Development Policy, Nova Science Publishers: Huntington, NY.

- Williams, S. 2006, ‘Ghana: Susu Collectors Connect with Formal Banking’, New African, International Communications, [Online] Retrieved on 27th http://findarticles.com/p/articles/mi_qa5391/is_200608/ai_n21396714

- World Bank (1994). Findings Africa Region, Number 26, Washington DC.

- World Bank Group 1997, Informal Financial Markets and Financial Intermediation in Four African Countries, Findings, Africa Region, January, no. 79, Knowledge Networks, Information and Technology, World Bank, Washington D.C.

You must be logged in to post a comment.