Citation

Lakjeewa, D. R., & Sandeepa, N. G. C. (2026). Which Financial Literacy Skills Matter Most? Evidence From Small Enterprises Investment Decisions. International Journal of Research, 13(3), 158–174. https://doi.org/10.26643/ijr/10

Dompeyalage Ruwan Lakjeewa,

Department of Business and Management Studies,

Faculty of Communication and Business Studies,

Trincomalee Campus, Eastern University, Sri Lanka,

Trincomalee, 31000,

Sri Lanka,

Nagoda Gamage Chathushi Sandeepa

Department of Business and Management Studies,

Faculty of Communication and Business Studies,

Trincomalee Campus, Eastern University, Sri Lanka,

Trincomalee, 31000,

Sri Lanka.

ABSTRACT

In today’s complex economic environment, financial literacy is a critical determinant of effective investment decisions, particularly for small enterprises (SEs). Despite the recognized importance of financial literacy in shaping business decision – making, limited empirical attention has been given to identifying which specific financial literacy skills most strongly influence investment decisions among small enterprises in Sri Lanka. This study examines that which financial literacy skill has most influential capability on investment decisions among small enterprises in Sri Lanka, analyzing financial literacy through five dimensions such as: Financial Planning, Fixed Assets Management, Investment Knowledge, Budgeting Knowledge, and Financial Record Keeping. Data were collected from 100 small enterprises owners through structured questionnaires and analyzed using mainly multiple regression techniques. The results reveal Investment Evaluation Knowledge (p < 0.05; β = 0.122) and Financial Record-Keeping (p < 0.05; β = 0.257) were found to have a significant positive impact on investment decisions. In contrast, Financial Planning (p > 0.05; β = -0.026), Fixed Assets Management (p > 0.05; β = 0.064), and Budgeting Knowledge (p > 0.05; β = 0.014)were not statistically significant predictors of investment decision-making. The findings demonstrate that financial literacy is a critical determinant of investment performance among enterprise owners, with financial record- keeping competence and investment evaluation skills emerging as the most influential factors in optimizing investment outcomes. The study highlights the importance of targeted training programs and professional consultation to strengthen their financial capabilities and supports policymakers in developing initiatives to enhance Financial Literacy of the sector.

Keywords: Financial Literacy Skills, Investment Decisions, Small Enterprises, Kalutara District.

01. Introduction

Financial literacy is a critical factor in informed decision-making, especially in the increasingly complex global economy. Thereby influencing the profitability of investments for small enterprises, which play a vital role in Sri Lanka’s economy by contributing 52% to GDP and 45% to employment, financial literacy is essential (Ranasinghe, 2024). The increasing complexity of the global economy necessitates that individuals become adept at making informed investment decisions to manage the rising cost of living. Financial literacy, the ability to understand and effectively apply financial knowledge, behavior, and attitudes plays a vital role in enabling individuals and organizations to make informed and rational financial choices (Vitt, 2004; Atkinson & Messy, 2012; OECD, 2013). Investment activities are viewed as both engaging and essential since they involve making choices and observing their outcomes (Awais, Laber, Rasheed, & Khursheed, 2016). SMEs, defined variably by different countries based on criteria such as employee count and financial metrics, are critical to national economies. In Sri Lanka, SMEs are classified as small Businesses with fewer than 49 employees and medium-sized businesses with 50 to 99 employees, with further definitions based on annual turnover and debt levels (Weerakkody, 2013). Globally, the relationship between financial literacy and investment decisions has been widely recognized. Financially literate individuals demonstrate higher confidence, better investment diversification, and stronger risk management skills (Van Rooij, Lusardi, & Alessie, 2011; Becchetti, Caiazza, & Coviello, 2013). Conversely, inadequate financial literacy has been associated with poor investment outcomes, excessive debt, and economic vulnerability (Lusardi & Mitchell, 2011). Many governments and international organizations, including the OECD, have emphasized financial education as a key policy tool for promoting economic stability and sustainable growth (Atkinson & Messy, 2012).

The relationship between financial literacy and investment decision-making has been a widely explored topic across global contexts; however, several critical gaps remain in both the theoretical understanding and empirical application of this relationship, particularly in developing economies such as Sri Lanka. A considerable body of literature acknowledges that financial literacy influences individuals’ investment choices, saving behaviors, and financial planning abilities (Lusardi & Mitchell, 2014; Potrich et al., 2018).

This creates a significant research gap. While it is generally accepted that financial literacy influences investment behavior, it remains unclear which specific dimension of financial literacy most strongly influences SEs investment decisions. Without identifying and ranking the most influential predictors, policymakers and SEs development programs may struggle to design targeted and efficient financial education interventions. Therefore, the central research problem of this study is to determine which dimension of financial literacy exerts the strongest influence on SEs investment decisions and the rank these dimensions according to their predictive power.

The following research problem has been arisen,

- Which dimension of financial literacy most strongly influences investment decisions?

This approach offers a more holistic perspective than previous models, which often viewed financial literacy as a single-dimensional construct. The study’s multidimensional framework encompassing financial planning, fixed assets management, investment evaluation knowledge, financial record keeping, and budgeting knowledge enables a deeper understanding of how different aspects of financial literacy interact to influence entrepreneurial investment behavior. As such, the research not only extends the theoretical foundations established by Awais et al. (2016) and Baihaqqy et al. (2020) but also contextualizes them within the realities of small business management in a developing economy.

02. Literature Review and Conceptual Framework

Financial Literacy

The concept of financial literacy has evolved significantly over time, with its origins tracing back to the United States in 1787. John Adams, in a letter to Thomas Jefferson, emphasized the importance of financial literacy to address the widespread confusion and distress in America caused by a lack of understanding of credit, currency circulation, and the nature of coinage (Financial Corps, 2014).financial literacy as a “meaning-making process,” wherein individuals apply a mix of skills, resources, and contextual knowledge to interpret information and make decisions, with an awareness of the financial consequences of their actions (Mason & Wilson, 2000).

Financial Planning

Financial planning is a critical component of financial literacy that involves the development of strategies to manage one’s finances to achieve long-term financial goals. America (2003) highlights that the propensity to plan significantly impacts wealth accumulation differences among individuals. Mitchell and Lusardi (2011) demonstrate that American adults with a higher level of financial literacy are more likely to engage in retirement planning.

Fixed Assets Management

Fixed assets management refers to the processes and practices involved in managing a business’s tangible and intangible assets to maximize future economic benefits. Siegel, Dauber, and Shim (2005) emphasize the need for businesses to categorize their assets accurately to manage them effectively and prevent misappropriation or theft.

Investment Evaluation Knowledge

Investment evaluation knowledge are the guidelines used to assess the viability of investment opportunities, ensuring consistency with the goal of maximizing shareholder wealth. Danielson and Scott (2006) observed that small firms often evaluate projects using simple methods like the payback period or the owner’s intuition

Financial Record Keeping

Financial Record Keeping is the systematic process of documenting, organizing, and maintaining all financial transactions and records of a business. Financial record keeping involves the consistent documentation and maintenance of financial transactions, providing a reliable foundation for reporting, compliance, and informed decision-making within a business (Weygandt, Kimmel & Kieso, 2018).

Budgeting Knowledge

Budgeting knowledge encompasses the skills and understanding needed to develop, implement, and monitor budgets, helping organizations manage financial resources and achieve strategic objective (Shim & Siegel, 2012).

Investment Decisions

Kothari (2007) stated that investment decisions involve allocating financial resources to various projects or assets with the expectation of future returns. These decisions are critical for ensuring the financial stability and profitability of an enterprise, requiring a thorough analysis of risks and rewards.

Investment Strategy

Investment strategy refers to a set of rules, behaviors, or procedures designed to guide an investor’s selection of an investment portfolio. Effective investment strategies are tailored to meet specific objectives, such as capital appreciation, income generation, or risk minimization (Brinson, Hood & Bee, 1995).

Investment Behaviors

Investment behaviors encompass the psychological and emotional responses of investors to market movements and financial decisions. Understanding investment behaviors is crucial for managing the behavioral risks that can lead to suboptimal investment decisions (Kahneman & Tversky, 1979).

Risk Tolerance

Notably, it has been reported that risk tolerance individuals tend to invest less in risk free assets (Hariharan et al., 2000) or risk averse households are more likely to have a lower proportion of their assets allocated in risky assets (Cardak & Wilkins, 2009).

Frequency of investment

Frequency of investment can be understood as the regular interval at which investments are made, reflecting an investor’s pattern and consistency in deploying capital over time (Gitman & Zutter, 2015).

Investment Type

Investment types for SEs encompass diverse asset allocations such as fixed capital, technological enhancements, and financial securities, all aimed at fostering growth, efficiency, and competitive advantage (Berk & Demarzo, 2019).

Investment Amount

Investment Amount is the total capital committed by a business to finance assets, projects, or operations intended to yield returns and foster growth (Westerfeld & Jaffe, 2019).

Many studies employ generalized measures of financial literacy often limited to knowledge of basic financial concepts such as interest, inflation, and risk diversification while ignoring behavioral and application-oriented aspects such as budgeting, record keeping, or asset management. Consequently, the multidimensional nature of financial literacy remains insufficiently explored.

From a theoretical standpoint, many previous studies have failed to integrate behavioral and psychological dimensions into financial literacy research. Theories such as the Goal-Setting Theory and Expectancy Theory provide valuable insights into how motivation and goal orientation influence decision-making under uncertainty. However, their application in SEs-related financial studies remains limited. Similarly, prior research has often ignored the mediating role of behavioral factors such as risk tolerance and investment strategy in the link between financial literacy and investment decisions. This limitation suggests that current frameworks are insufficiently comprehensive to explain the complex interaction of cognitive, behavioral, and contextual variables influencing small enterprise owners’ investment decisions.

Conceptual Framework

Two variables were conceptualized as below such as Financial Literacy is the independent variable and Investment decision is the dependent variable for this study purpose.

2.1 Conceptual framework

Figure 2.1 Conceptual Framework

(Developed by Researchers)

Hypotheses

H1: Financial Planning has a significant impact on Investment Decisions.

H2: Fixed Assets Management has a significant impact on Investment Decisions.

H3: Investment Evaluation Knowledge has a significant impact on Investment Decisions.

H4: Financial Record Keeping has a significant impact on Investment Decisions.

H5: Budgeting Knowledge has a significant impact on Investment Decisions.

- RESEARCH METHODOLOGY

Research Approach

This study adopts a deductive research approach, in which established theories are used to formulate hypotheses that are empirically tested through systematic data collection and analysis (Sekaran & Bougie, 2010).

Sample Selection

The study employed clusters sampling to select respondents form small enterprises owners in the Kalutara District. Five geographical clusters were identified based on major business locations within the district: Baduraliya, Mathugama, Dodangoda and Kalutara.

An equal allocation approach was adopted, and 20 respondents were selected from each cluster using simple random sampling, resulting in a total sample size of 100 participants.

3.1 Table Sample Selection

| Town | Sample Size |

| Baduraliya | 20 |

| Mathugama | 20 |

| Dodangoda | 20 |

| Nagoda | 20 |

| Kalutara | 20 |

| Total | 100 |

(Source: Survey Data, 2024)

Measures and Analytical Tools

Analysis of Reliability

The reliability of the instrument was measured using Cronbach’s Alpha analysis. It measures the internal consistency of the instrument, based on the average inter-item correlation. The result of Cronbach’s alpha test is shown in Table 3.2 which suggests that the internal reliability of each instrument was satisfactory. Most the Cronbach’s Alpha Value is above 0.7 indicates an acceptable internal consistency of the scale (Sekaran & Bougie, 2016).

Table 3.2 -Decision Criteria for Reliability Analysis

| Range | Decision Attribute |

| r ≥ 0.9 | Excellent Reliability |

| 0.8 ≤ 0.9 | Good Reliability |

| 0.7 ≤ 0.8 | Acceptable Reliability |

| 0.6 ≤ 0.7 | Questionable Reliability |

| 0.5 ≤ 0.6 | Poor Reliability |

| r < 0.5 | Unacceptable Reliability |

(Source: Koonce & Kelly, 2014)

Data were collected using a structured questionnaire with Likert-scale and multiple-choice items to measure financial literacy dimensions and investment decision-making. Data analysis was performed using SPSS. Descriptive statistics (mean, frequency, and standard deviation) were applied to assess central tendencies and variability. Multiple regression analysis was employed to determine the predictive influence of financial literacy components on investment decisions, allowing the study to quantify the magnitude of effects while controlling for demographic factors.

The impact of financial literacy components on investment decisions was evaluated using multiple regression analysis:

Y = α + β1 FP + β2 FAM + β3 IEK + β4 FRK + β5BK + e

Y= Observation of the dependent Variable

β0= intercept term

FP- Correlation Coefficient of Financial Planning

FAM- Correlation Coefficient of Fixed Assets Management

IEK- Correlation Coefficient of Investment Evaluation Knowledge

FRK- Correlation Coefficient of Financial Record Keeping

BK- Correlation Coefficient of Budgeting Knowledge

e = Standard Error

04. Result & Discussion

Analysis of Reliability

The reliability of the independent and dependent variables was demonstrated using Cronbach’s Alpha coefficients. In this study (Table 4.1), the overall Cronbach’s Alpha for Financial Literacy was 0.829, with the individual dimensions showing the following values: Financial Planning (0.867), Fixed Assets Management (0.719), Investment Evaluation Knowledge (0.954), Financial Record Keeping (0.912), and Budgeting Knowledge (0.994). The Cronbach’s Alpha for Investment Decision was 0.851. According to the general guideline, a Cronbach’s Alpha coefficient above 0.70 is considered acceptable for reliability.

Table 4.1-Reliability Analysis for Overall Variables

| Variable / Dimensions | Cronbach’s Alpha Value | Number of Question Items |

| Financial Literacy | 0.829 | 25 |

| Financial Planning | 0.867 | 5 |

| Fixed Assets Management | 0.719 | 5 |

| Investment Evaluation Knowledge | 0.954 | 5 |

| Financial Record Keeping | 0.912 | 5 |

| Budgeting knowledge | 0.994 | 5 |

| Investment Decision | 0.851 | 17 |

(Source: Survey Data, 2024)

Demographic Variables

Business Activity

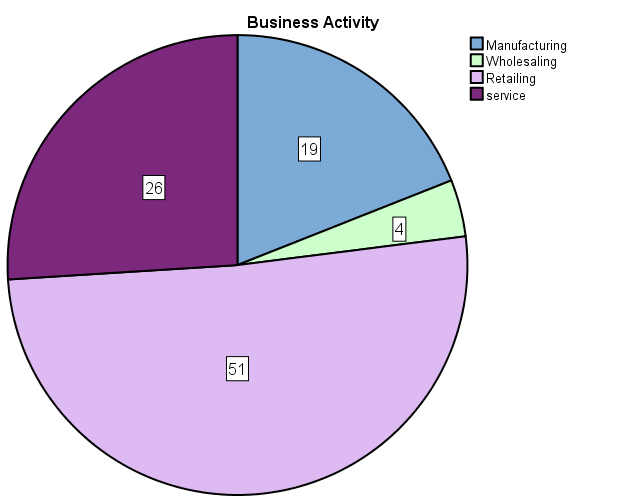

Most of the respondents are engaged in retailing, with 51% of small enterprise owners in the Kalutara District reporting this as their business activity. This is the highest proportion among the different business types. Following retailing, 26% are involved in service-based businesses, 19% in manufacturing, and 4% in wholesaling, which represents the lowest proportion. These results highlight that retailing is the dominant business activity in the district.

(Source: Survey Data, 2024)

Dimensions Coefficients

Table 4.2-Dimensions Coefficients

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | 95.0% Confidence Interval for B | |||

| B | Std. Error | Beta | Lower Bound | Upper Bound | ||||

| 1 | (Constant) | 1.168 | .187 | 6.246 | .000 | .797 | 1.539 | |

| Financial Planning | -.026 | .053 | -.061 | -.485 | .629 | -.131 | .080 | |

| Fixed Assets Management | .064 | .047 | .146 | 1.347 | .181 | -.030 | .157 | |

| Investment Evaluation Knowledge | .122 | .048 | .254 | 2.560 | .012 | .027 | .216 | |

| Financial Record Keeping | .257 | .077 | .409 | 3.326 | .001 | .103 | .410 | |

| Budget Knowledge | .014 | .055 | .026 | .258 | .797 | -.095 | .124 | |

| Dependent Variable: Investment Decision | ||||||||

As shown in Table 4.2, the regression results indicate that among the five dimensions of financial literacy, only Investment Evaluation Knowledge ((p<0.05); β = 0.122)and Financial Record-Keeping (p < 0.05; β = 0.257) have a significant positive impacton investment decisions. In contrast, Financial Planning (p > 0.05; β = -0.026), Fixed Assets Management (p > 0.05; β = 0.064), and Budgeting Knowledge (p > 0.05; β = 0.014) were found to have insignificant effects. According to the coefficient result, the regression model can be express as follows.

Y = α + β1 FP + β2 FAM + β3 IEK + β4 FRK + β5 BK + e

Y= 1.168 – .026FP + 0.064FAM + 0.122IEK + 0.257FRK + 0.014BK

Investment Decision= 1.168 – 0.026 Financial Planning + 0.064 Fixed Assets Management + 0.122 Investment Evaluation Knowledge+ 0.257 Financial Record Keeping+ 0.014 Budget Knowledge

Testing Hypotheses

Table 4.3-Testing Hypotheses

| Hypothesis | P-Value | Decision |

| H1- Financial Planning has a significant impact on Investment Decisions. | Sig 0.629 (p >0.05) | Rejected |

| H2 – Fixed Assets Management has a significant impact on Investment Decisions. | Sig 0.181 (p>0.05) | Rejected |

| H3- Investment Knowledge has a significant impact on Investment Decisions. | Sig 0.012 (p<0.05) | Accepted |

| H4- Financial Record Keeping has a significant impact on Investment Decisions. | Sig 0.001 (p<0.05) | Accepted |

| H1- Budgeting Knowledge has a significant impact on Investment Decisions.H1- Budgeting Knowledge has a significant impact on Investment Decisions. | Sig 0.797 (p>0.05) | Rejected |

(Source: Survey Data, 2024)

Discussion of Findings

Investment Evaluation Knowledge (p < 0.05; β = 0.122) and Financial Record-Keeping (p < 0.05; β = 0.257)were found to have a significant positive impact on investment decisions. This suggests that small enterprise owners who regularly maintain financial records and possess analytical skills in evaluating investment alternatives are more capable of making effective financial choices. Maintaining accurate records helps entrepreneurs track performance, manage cash flows, and evaluate profitability, while investment evaluation knowledge enables them to assess risk and return before committing resources. These findings are consistent with Lusardi and Mitchell (2014)and Fatoki (2014), who also found that financial literacy significantly improves the quality of investment behavior among entrepreneurs in developing economies.

In contrast, Financial Planning (p > 0.05; β = -0.026), Fixed Assets Management (p > 0.05; β = 0.064), and Budgeting Knowledge (p > 0.05; β = 0.014) were not statistically significant predictors of investment decision-making. Although these aspects are essential for overall business performance, their lack of direct influence suggests that many small enterprise owners may have basic awareness of planning and budgeting concepts but do not effectively apply them when making investment decisions. This finding aligns with Grohmann (2018), who noted that general financial management skills, while beneficial, often have limited direct impact on investment outcomes unless combined with specific analytical competencies.

The low overall level of financial literacy observed in this study mirrors the situation in many developing countries, where small business owners often rely on informal financial practices rather than structured knowledge. According to Ratnawati et al. (2022), limited access to formal financial education and advisory services contributes to this deficiency. In the Sri Lankan context, where SEs form the backbone of the economy, such a gap represents a significant constraint to growth and competitiveness.

From a theoretical standpoint, these findings validate the Goal-Setting Theory and Rational Expectations Theory that underpin this study. The Goal-Setting Theory posits that individuals with clear objectives and adequate knowledge are more likely to pursue purposeful actions, while the Rational Expectations Theory emphasizes the use of information and learning in forming optimal decisions. The current study confirms that financially literate entrepreneurs those capable of maintaining records and analyzing investments tend to make decisions consistent with rational and goal-oriented behavior.

05. Conclusions

Conclusions

The findings provide clear evidence that enhancing financial literacy among entrepreneurs leads to better investment outcomes. Practically, SEs owners should adopt systematic financial record-keeping practices, regularly evaluate investment opportunities, and utilize digital accounting tools. Incorporating these practices will foster informed decision-making and enable firms to withstand market uncertainties. For managers and business owners, financial literacy should be recognized as a strategic management resource. Training employees in record maintenance, investment analysis, and budgeting can create a financially disciplined culture that promotes transparency, accountability, and long-term competitiveness. Enterprises that prioritize financial education internally are more likely to secure funding and achieve sustainable growth. This research provides empirical evidence supporting the Goal-Setting Theoryand Rational Expectations Theory in the Sri Lankan SEs context. It shows that financial literacy equips entrepreneurs with the ability to set measurable investment goals, align expectations with market realities, and make rational choices grounded in data and financial reasoning.

Overall, the study concludes that strengthening financial literacy, especially in the areas of record keeping and investment evaluation is essential for small enterprise owners to improve the quality and effectiveness of their investment decisions. This study fills the empirical and variable gaps in the existing literature by providing localized evidence from Kalutara District, demonstrating that behavioral financial competencies can be systematically measured and linked to tangible investment outcomes.

References

Anthes, W. L. (2004). Financial illiteracy in America: A perfect storm, a perfect opportunity. Journal of Financial Service Professionals, 58(4), 20–29.

Atkinson, FA Messy. (2011). Journal of Pension Economics & Finance.

Awais, M., Laber, M. F., Rasheed, N., & Khursheed, A. (2016). Impact of financial literacy and investment experience on risk tolerance and investment decisions: Empirical evidence from Pakistan. International Journal of Economics and Financial Issues, 6(1), 73–79.

Berk, Jonathan B. and Richard C. Green, “Mutual Fund Flows and Performance in Rational Markets,” Journal of Political Economy, 2019, 112 (6), 1269–1295.

Cardak, B. A., & Wilkins, R. (2009). The determinants of household risky asset holdings: Australian evidence on background risk and other factors. Journal of Banking & Finance, 33(9), 1656-1668.

Gitman, Lawrence J. and Chad J. Zutter. 2015. Principles of Managerial Finance, Fourteenth Edition. United States: Pearson Education.

GP Brinson, LR Hood, GL Bee bower,1995. Financial Analysts Journal.

Kahneman, D., & Tversky, A. (2013). Prospect theory: An analysis of decision under risk. In Handbook of the fundamentals of financial decision making.

Kothari, S. P., & Warner, J. B. (2007). Econometrics of event studies. In Handbook of empirical corporate finance

Kumari, D. A. T. (2020). The impact of financial literacy on investment decisions: With special reference to undergraduates in Western Province, Sri Lanka. Asian Journal of Contemporary Education, 4(2), 1–10.

Kumari, D. A. T., Azam, S. M. F., & Khalidah, S. (2020). The impact of financial literacy on women’s economic empowerment in developing countries: A study among the rural poor women in Sri Lanka. Asian Social Science, 16(3), 1–10.

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and planning implications for retirement wellbeing. NBER working paper.

Lusardi, A. (2008). Financial literacy: an essential tool for informed consumer choice? National Bureau of Economic Research.

Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8.

Lusardi, A., & Mitchell, O. (2011). Financial literacy and planning implications for retirement wellbeing. NBER working paper, 17(4), 2-37.

Lusardi, A., & Mitchell, O. (2011). Financial Literacy and Retirement Planning in the United States. Journal of Pension Economics and Finance, 10(4), 509-525.

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy around the world: an overview. Journal of Pension Economics & Finance, 10(4), 497-508. Cambridge University Press

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy around the world: An overview. Journal of Pension Economics & Finance, 10(4), 497-508.

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. American Economic Journal: Journal of Economic Policy, 6(2), 97–138.

Mason, C. L. J., & Wilson, R. M. S. (2000). Conceptualising financial literacy. Occasional Paper.

MG Danielson, JA Scott. (2006). Journal of Applied Finance.

Musundi, K. M. (2014). The effects of financial literacy on personal investment decisions in real estate in Nairobi County. University of Nairobi.

Ratnawati, Kusuma et al. “Leveraging financial literacy into sustainable business performance: A mediated-moderated model.”

Sarraf, J., Irani, Z., & Weerakkody, V. (2018). The role of social capital in promoting financial literacy and financial inclusion. The British Academy of Management.

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill-building approach (7th ed.).

Shim, J. K., Siegel, J. G., & Dauber, N. (2008). Corporate controller’s handbook of financial management (2008-2009).

Shim, J. K., Siegel, J. G., & Shim, A. I. (2011). Budgeting basics and beyond.

Tversky, A., & Kahneman, D. (1988). Rational choice and the framing of decisions. In Decision making: Descriptive, normative, and procedural perspectives.

Vitt, L.A. (2004), “Consumers financial decisions and the psychology of values”, Journal of

Financial Service Professionals, Vol. 58 No. 6, pp. 68-78.

Weygandt, J. J., Kimmel, P. D., Kieso, D. E., & Aly, I. M. (2018). Managerial accounting: Tools for business decision-making.

About Authors

D. Ruwan Lakjeewa is a Senior Lecturer (Grade I) in Accounting at the Department of Business and Management Studies, Faculty of Communication and Business Studies, Trincomalee Campus, Eastern University, Sri Lanka. He holds an M.Sc. in Management from the University of Sri Jayewardenepura and a B.Sc. (Hons) in Accounting and Finance from Trincomalee Campus, Eastern University, Sri Lanka. His research interests include corporate governance, financial performance, human resource accounting, and financial literacy. He has published several journal articles and conference papers on aforementioned topics and serves as a reviewer and editorial contributor for academic conferences and journals.

Nagoda Gamage Chathushi Sandeepa is a Lecturer (Temporary Assistant) in the Department of Business and Management Studies, Faculty of Communication and Business Studies, Trincomalee Campus, Eastern University, Sri Lanka. She holds a B.Sc. (Hons) in Accounting and Finance with first class from Trincomalee Campus, Eastern University, Sri Lanka. Her research interests include financial literacy and Investment Decisions.

You must be logged in to post a comment.