Section 375 of the Indian Criminal Code was created to protect women from rape. In Indian criminal law, in section 375 Men are said to commited rape if he : (a) pierce the penis in some way or force a “rape” on a woman’s vagina, mouth, urethra, or anus. (b) in some way insert an object or body part other than the penis into the woman’s vagina, urethra, or anus, or have the woman do so to him or others. (c) manipulate any part of a woman’s body to penetrate or penetrate the woman’s vagina, urethra, anus, or other parts of her body. (d) place the mouth in the woman’s vagina, anus, urethra.

Under Section 370 , If a person rape woman and do so in any of the following seven situations. 1) Against to their will. 2) Without their consent. 3)With consent and consent for fear of death or injury to them or those they are close to. 4) Consent is given because a man knows he is not her husband and believes that he is another man who is married, or that he is legally married. If so, with her consent 5) If she is under the age of 18, with or without her consent.

Abuse of power One of the famous sayings used in connection with Section 375 is “Men are guilty until proved innocent, and women are not guilty until proved innocent.” Laws enacted to empower women and reassure them in patriarchal societies soon turned into swords that killed the dignity of men in society by false accusations, or women misused laws and power made to protect them. The problem that is occurring in our world today is that women use verbal consent to have sexual intercourse and later refuse or refrain from having sexual intercourse or falsely accuse men that they had it without thier consent. In both cases, the man has the responsibility of proof and must prove his innocence.

According to an article published in The Times of India , only one person was convicted in each of the fourth cases of rape, and high probability that anyone who did not proven guilty after a full trial could be innocent. Leads to the high assumption that innocent people have been accused of rape. India’s conviction ratebin rape cases is 32%, which is self-evident from the fact that numerous false reports related to rape have been registered in India.

Being a victim of false rape allegations is as bad as being a victim of rape. You can’t imagine the shock, trauma, ridicule, and humiliation that someone experienced after being falsely accused of rape. Not only the man, but his family and close friends suffer from various consequences, and isolation and ridicule are just a few of them. Their future is shattered, the humiliation and shame that society suffers is enough to shatter it, and no one can think of them living as they used to.

What can be done ? The creators of Article 375 of the 2013 Act and the Criminal (Amendment) having only one vision in context to the problem, consider only the safety of women and have not developed any means of protecting innocent men in society. Therefore, there is usually a debate about what we can do to protect innocent people from society who are falsely accused. Provision (Section 375) cannot be said to be gender-neutral to remove the slight justice that this section offers, as it acts as a hurdle for women to file genuine rape cases. Then the question arises. What can you do? In such situations, the legislature and judiciary need to work together to strike the right balance between men and women so that the virtues of justice are provided to them equally.

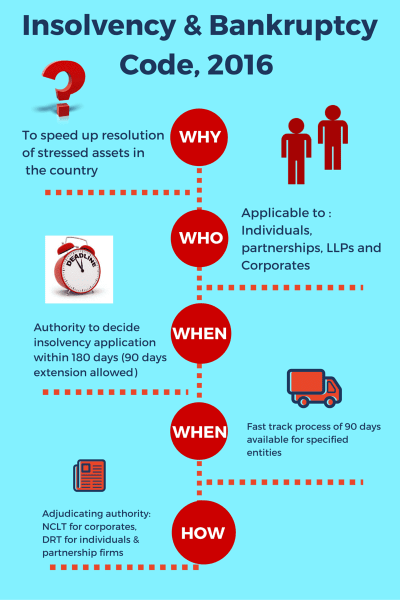

The Code was enacted in 2016 following decades of recommendations suggesting improvements to the previous insolvency regime, which was fragmented, fraught with delays and resulted in poor recoveries for creditors. [1]

The insolvency resolution process in India has in the past involved the simultaneous operation of several statutory instruments.

These include the Sick Industrial Companies Act, 1985, the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002, the Recovery of Debt Due to Banks and Financial Institutions Act, 1993, and the Companies Act, 2013.[2]

Broadly, these statutes provided for a disparate process of debt restructuring, and asset seizure and realization in order to facilitate the satisfaction of outstanding debts. [3]

As is evident, a plethora of legislation dealing with insolvency and liquidation led to immense confusion in the legal system, and there was a grave necessity to overhaul the insolvency regime.

All of these multiple legal avenues, and a hamstrung court system led to India witnessing a huge piling up of non-performing assets, and creditors waiting for years at end to recover their money. [5]

The Bankruptcy Code is an effort at a comprehensive reform of the fragmented regime of corporate insolvency framework, in order to allow credit to flow more freely in India and instill faith in investors for speedy disposal of their claims. [4]

The Code consolidates existing laws relating to insolvency of corporate entities and individuals into a single legislation.

The Code has unified the law relating to enforcement of statutory rights of creditors and streamlined the manner in which a debtor company can be revived to sustain its debt without extinguishing the rights of creditors[5]:-

1) The scheme of the Code marked a sea change from the previous regime. In respect of corporate entities, the Code introduced a creditor-in-control regime (with a focus on empowering financial creditors), a time-bound resolution process and reduced scope for judicial intervention, and established institutions such as the Insolvency and Bankruptcy Board of India, insolvency professionals and information utilities.[6]

Since the implementation of this new regime, the constitutional validity of various provisions of the Code has been challenged before various High Courts, and the Supreme Court.

Applicability

The Code provides creditors with a mechanism to initiate an insolvency resolution process in the event a debtor is unable to pay its debts. The Code makes a distinction between Operational Creditors and Financial Creditors. [7]

A Financial Creditor is one whose relationship with the debtor is a pure financial contract, where an amount has been provided to the debtor against the consideration of time value of money (“Financial Creditor”).

Recent reforms have sought to address the concerns of homebuyers by treating them as ‘financial creditors’ for the purposes of the Code. [7]

By a recently promulgated ordinance, the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2018 (“the Ordinance”), the amount raised from allottees under a real estate project (a buyer of an under-construction residential or commercial property) is to be treated as a ‘financial debt’ as such amount has the commercial effect of a borrowing.[7]

The Ordinance does not clarify whether allottees are secured or unsecured financial creditors. Such classification will be subject to the agreement entered into between the homebuyers and the corporate debtor.

In the absence of allottees having a clear status, there may be uncertainty about their priority when receiving dues from the insolvency proceedings. [7]

An Operational Creditor is a creditor who has provided goods or services to the debtor, including employees, central or state governments (“Operational Creditor”). A debtor company may also, by itself, take recourse to the Code if it wants to avail of the mechanism of revival or liquidation. [7]

In the event of inability to pay creditors, a company may choose to go for voluntary insolvency resolution process – a measure by which the company can itself approach the NCLT for the purpose of revival or liquidation. [7]

What was the judicial approach to the Insolvency and Bankruptcy Code?

SERIES OF JUDICIAL PRONOUNCEMENT

With almost more than two years since the introduction of the Code, there have been various challenges in the effective implementation of the Code. However, constructive interpretation by the judiciary coupled with effective amendments to the Code has helped in eradicating most of these teething issues. [8]

Some of the key judicial pronouncements are discussed below:

The Insolvency and Bankruptcy Board of India which is the regulatory and supervisory body in charge of the IBC, has done a commendable job in proactively spreading awareness and regulating the space. [9]

Many important judgments were pronounced throughout the year, including certain landmark cases, where in the Supreme Court has tried to ensure that the spirit of the Code is given primacy over procedural requirements. [9]

Suspended Board of Directors of Corporate Debtor Entity are entitled to access the resolution plan and other related documents:-

In a significant judgments delivered on January 31, 2019, the Hon’ble Supreme Court of India decided on an important aspect with respect to the rights of the suspended board of directors of the Corporate Debtor Entity to receive and access the resolution plan and other related documents, whose case has been admitted by the Adjudicating Authority under the relevant provisions of the Code. [10]

Facts of the Case:

In respect of Mr. Vijay Kumar Jain, Director of Corporate Debtor (‘Appellant’) vs. Standard Chartered Bank and Ors. (As ‘Financial Creditors’), the NCLT had approved the appointment of Resolution Professional (‘RP’) to conduct Corporate Insolvency Resolution Process of Corporate Debtor Company i.e. Ruchi Soya Industries Limited (‘RSIL’). [10]

The appellant, being a member of the suspended board of RSIL, was given notice and agenda for the first meeting of Committee of Creditors (‘CoC’) and was permitted to attend the meeting of CoC. The appellant alleged that he was not granted permission to participate in subsequent meetings of CoC. [10]

As a result, the appellant filed a miscellaneous application before the NCLT to allow his participation in the subsequent meetings of CoC. The appellant also executed a Non-Disclosure Agreement (‘NDA’) to keep information received through participation in the CoC meeting strictly confidential and even undertook to indemnify RP. [10]

However, NCLT vide its order dated August 1, 2018 dismissed the said application of appellant with liberty to the appellant to attend the COC meetings, but not to insist upon the CoC or RP to provide information which is considered as confidential by the CoC or RP. [11]

Against the said order of NCLT, the appellant filed an appeal before the Appellate Tribunal, which recognized the right of appellant to attend and participate on the CoC meetings but Appellate Tribunal vide its order dated August 9, 2018 [12] denied the prayer of the appellant to have access to certain documents including sensitive resolution plan.

The appellant aggrieved by the order of the NCLAT, filed an appeal before the Hon’ble Supreme Court of India. [13]

Apex Court Observations and Findings:

On advertising relevant provisions of the Code and arguments of parties to the dispute, the Supreme Court opined that notice of each meeting of the CoC will have to be given to the suspended board of directors of the corporate debtor entity. [14]

The Supreme Court further noted that the statutory scheme of IBC makes it clear that though the suspended board are not members of the CoC, yet, they have a right to participate in each and every meeting held by the CoC and also have a right to discuss along with members of the CoC, resolution plan that are presented at such meeting. [14]

The Supreme Court further observed that Section 31(1) of the Code make it clear once the resolution plan is passed by the Adjudicating Authority, it shall be binding on the corporate debtor together with guarantors and other stakeholders. [14]

This being the case, it is clear that the erstwhile board of directors, which consists of persons who may have given personal guarantees for the debts owed by the corporate debtor, will be bound by the resolution plan, and therefore, have a vital stake in what ultimately gets passed by the CoC’s.[14]

The Supreme Court also made it clear that so far as confidential information is concerned, RP can take an undertaking in the form of NDA from suspended board of directors of the corporate debtor entity with an objective to maintain strict confidentiality in regard to resolution plan and other related documents. [14]

Further, according to Regulation 39(5) of IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016, the RP shall forthwith send a copy of the order of the Adjudicating Authority approving or rejecting a resolution plan to the participants and resolution applicant. The term ‘Participants’ includes members of the erstwhile Board of Directors of Corporate Debtor. [14]

Thus in view of the above, the Supreme Court allowed the appeal and set aside the impugned order of the Appellate Tribunal. [14]

What was the result of Insolvency and Bankruptcy Code in the present scenario? Also cite relevant case laws.

IBC came into being repealing SICA (Sick Industrial Companies Act), SICA was repealed with effect from 1 December 2016. [15]

To know the background of IBC, it is important to know more about SICA and why it failed to prevail as a law. [15]

This is the exact rationale for the existence of The Insolvency and Bankruptcy Code in India which has been into effect since 2016. [15]

To know the background of IBC, it is important to know more about SICA and why it failed to prevail as a law. [15]

The journey from SICA to IBC

The SICA, 1985:-

The name SICA, itself connotes the reason for its actuality. India witnessed an atmosphere of rampant industrial sickness in the 1980s in furtherance of which the Government of India came up with key legislation i.e. the Sick Industrial Companies Act to combat the issue. [15]

Widespread industrial sickness affects the economy in a number of ways, thus The Act came into being to spot the sick or potentially sick companies owning industrial undertakings and take speedy remedial measures for their revival or in a scenario where there is no such measure, close such units. [15]

This was an action to get the locked up investment in such industrial units released and use them in a more productive manner. SICA was repealed and replaced by the Sick Industrial Companies (Special Provisions) Act of 2003, which diluted certain provisions of SICA and filled certain gaps. [15]

One of the main changes to the new law was that, in addition to combating occupational diseases, it also aimed to reduce the growing incidence by ensuring that companies do not use a medical certificate simply to evade legal obligations and access concessions granted to financial institutions to receive. [15]

The comprehensive performance of the Act did not live up to the expected results and thus, IBC was notified as on 28th May 2016 and the repeal of SICA came into full effect from December 1, 2016. [15]

IBC Kicks In

Mistakes of the past were taken in view and The Insolvency and Bankruptcy code came into being with a wider scope and aiming to resolve the issues via more effective provisions and implementation. It is an act to consolidate and amend the laws having reorganization and insolvency resolution issues as the subject-matter. [15]

The provisions of the Act shall apply to the following in case of insolvency, liquidation, voluntary liquidation or bankruptcy; [15]

“An Act to consolidate and amend the laws relating to reorganisation and insolvency resolution of corporate persons, partnership firms and individuals in a time bound manner for maximisation of value of assets of such persons, to promote entrepreneurship, availability of credit and balance the interests of all the stakeholders including alteration in the order of priority of payment of Government dues and to establish an Insolvency and Bankruptcy Board of India, and for matters connected therewith or incidental thereto.

Whether the expression “and” occurring in section 8(2)(a) may be read as “or”?

The Court held that the expression “and” occurring in section 8(2)(a) may be read as “or” in order to further the object of the statute and/ or to avoid an anomalous situation – once the operational creditor has filed an application, which is otherwise complete, the adjudicating authority must reject the application under Section 9(5)(2)(d) if notice of dispute has been received by the operational creditor or there is a record of dispute in the information utility – So long as a dispute truly exists in fact and is not spurious, hypothetical or illusory, the adjudicating authority has to reject the application – A “dispute” is said to exist, so long as there is a real dispute as to payment between the parties that would fall within the inclusive definition contained in Section 5(6). [16]

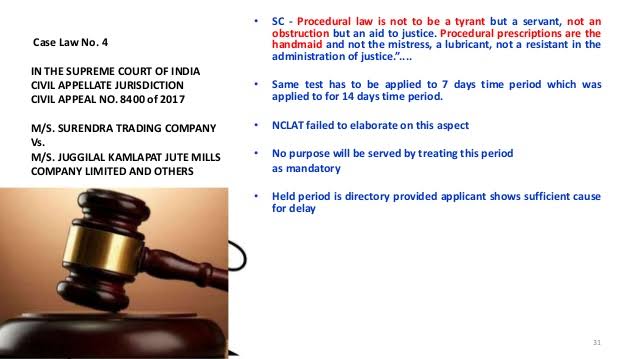

2) Surendra Trading Company Vs. Juggilal Kamlapat Jute Mills Company Ltd. & Others- Supreme Court:

The time limit prescribed in IBC, 2016 for admitting or rejecting a petition or initiation of CIRP under proviso to sub-sec. (5) of Sec. 9, is directory. [17]

The question before the NCLAT was to whether time of fourteen days under section 9(5) given to the adjudicating authority for ascertaining the existence of default and admitting or rejecting the application is mandatory or directory. [17]

NCLAT hold that the mandate of sub-section (5) of section 7 or sub-section (5) of section 9 or sub-section (4) of section 10 is procedural in nature, a tool of aid in expeditious dispensation of justice and is directory. [17]

Further question (with which supreme Court is concerned) was as to whether the period of seven days for rectifying the defects under proviso to sub-section (5) of Section 9 is mandatory or directory. The aforesaid provision of removing the defects within seven days is directory and not mandatory in nature. [17]

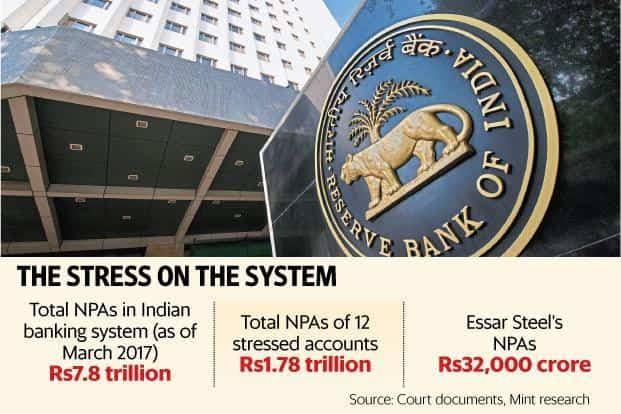

3) Essar Steel India Ltd. Vs. Reserve Bank of India-

RBI is authorized to direct any banking company to initiate insolvency resolution process- Gujarat High Court. [18]

A long-drawn legal battle for Essar Steel ends with this Supreme Court judgment. In one of the most discussed cases under IBC i.e. the case of Essar Steel Limited, the Supreme Court delivered its judgment which would probably be the final judgment of the case. Key highlights of the Essar Steel Supreme Court judgment are as follows: [19]

The requirement of completing the corporate insolvency resolution process within 330 days from the insolvency commencement date as introduced by the 2019 Amendment Act was held as non-mandatory. [19]

CoC can delegate its administrative powers or power of negotiation with the resolution applicants to a smaller committee (sub-committee) since such acts would be ultimately required to be approved and ratified by the CoC. [19]

Prospective resolution applicant has a right to receive complete information as to the CD, debts owed by it, and its activities as a going concern and as such it cannot suddenly be faced with “undecided” claims after the resolution plan submitted by it has been accepted. [19]

To put an end to uncertainty, parameters were laid down for limiting the scope of interference of Adjudicating Authority and Appellate Authority with the commercial decision taken by the requisite majority of CoC. [19]

The Supreme Court has re-emphasized the primacy of the commercial wisdom of the CoC in relation to resolution of the corporate debtor as well as difference in treatment of unequally placed creditors based on its earlier decisions in Swiss Ribbons and K. Sashidhar cases. [19]

Why are the judgments of the Insolvency and Bankruptcy cases pending with court?

The judgments of the cases are pending with the Court due to the Causes for the delays which range from frivolous challenges by operational creditors and promoters to basic issues like shortage of judges. [20]

There is no stipulated time-line for operational creditors to challenge the rejection of their claim, shortage of members at the bench, allowing intervention by promoters at the admission stage and long gaps between conclusion of hearing and passing of written orders are all causing delays,” said Sapan Gupta, national head banking and finance practice at Shardul Amarchand and Mangaldas. [20]

To be fair, delays are not a peculiarly Indian phenomenon. Many advanced countries struggle to provide quick, high-quality justice to citizens. But in India the scale of the problem is unprecedented. Focusing on capacity alone won’t reduce delays. [21]

A pervasive reason for the delays is adjournments. Many advanced countries struggle to provide quick, high-quality justice to citizens. But in India the scale of the problem is unprecedented.[21]

Conclusion

In conclusion, the Insolvency and Bankruptcy Code, 2016, is a progressive legislation that is intended to improve the efficiency of insolvency and bankruptcy proceedings in India. The new legislation provides for the early detection of financial distress and a time bound process for resolution. [22]

However, many details on the IBC’s implementation need to be worked out in the regulations, and its success will depend to a large extent on how quickly a high quality cadre of insolvency resolution professionals will emerge and on whether the time bound process for insolvency resolution will be adhered to in practice. [22]

The IBC has taken its first steps to regularize the insolvency process in India. It has amended over 11 legislations in India, bringing about one of the most significant changes to commercial laws in India in recent times. However, the 22 months of this nascent legislation have been ridden with controversies and speedy resolutions. [23]

It has also become a very important tool for banks to regularize multitudes of non-performing assets plaguing the country’s economy. Within 7 months of the enactment of the IBC, the Reserve Bank of India released a list of 12 companies which held about 25% of the gross non-performing assets of the country.[23]

With more than 11% of all loans in India being terms as bad loans, the IBC has become the need of the hour. The IBC has brought a plethora of changes to insolvency laws in India and aims to reduce the amount of bad loans that has saddled the economy over the last few years. [23]

We are beginning to see this through various companies successfully concluding their insolvency process. The first successful case of a CIRP was that of Bhushan Steel wherein TATA Steel agreed to purchase Bhushan Steel for Rupees Thirty-Two Thousand Five Hundred Crores. [23]

With many more insolvency resolution processes in the pipeline, only time will tell if the IBC will prove to be a successful tool with its objective of streamlining the insolvency process in India. [23]

1) Bankruptcy Law Reforms Committee, The Interim Report of the Bankruptcy Law Reforms Committee (2015).

2) Rule 2.1.1. of RBI Master Circular – Prudential Norms on Income Recognition, Asset Classification and Provisioning – Pertaining to Advances defines an NPA as ‘An asset, including a leased asset, becomes non-performing when it ceases to generate income for the bank. A ‘non-performing asset’ (NPA) was defined as a credit facility in respect of which the interest and/ or installment of principal has remained ‘past due’ for a specified period of time.

3) It must be noted that creditors having outstanding debts continue to have the right to approach an appropriate forum like civil courts or arbitral tribunals for recovery of debts which would be a contractual right of recovery.

4) As cited in the “Abstract” of “Emerging Jurisprudence on Corporate Insolvency” by Shipra Sayal Institute of Law, Nirma University, Ahmedabad, Gujarat, India.

5) As cited in the “Introduction” Para of “A Primer on the Insolvency and Bankruptcy Code, 2016” by Nishith Desai Associates:- The Legal and Tax Counseling Worldwide.

6) As cited in the “Introduction” para of “Understanding the Insolvency and Bankruptcy Code, 2016:- Analysing the developments in jurisprudence” by “Vidhi Bankruptcy Research Programme” at the Vidhi Centre for Legal Policy and the Legal Division of the Insolvency and Bankruptcy Board of India.

7) As cited in the “Applicability” Para of “A Primer on the Insolvency and Bankruptcy Code, 2016” by Nishith Desai Associates:- The Legal and Tax Counseling Worldwide.

8) As cited in the “4th Para ,viz, Series of Judicial Pronouncement” of “Series of Judicial Pronouncement – Insolvency and Bankruptcy Code, 2016” written by Rushabh Ajmera on TaxGuru.

9) As cited in the “Introduction” Para of “Insolvency and Bankruptcy Hotline:- ANALYSING 2018 THROUGH THE LENS OF THE INSOLVENCY CODE” written on January 17, 2019 by Nishith Desai Associates.

10) As cited in the “4th Para” viz, Series of Judicial Pronouncement” of “Series of Judicial Pronouncement – Insolvency and Bankruptcy Code, 2016” written by Rushabh Ajmera on TaxGuru Website India 11 months ago.

11) As cited in “NCLT pronounced order on August1, 2018”.

13) As cited in “Facts of the Case Para” of “Series of Judicial Pronouncement – Insolvency and Bankruptcy Code, 2016” by Rushabh Ajmera 11 Months ago on TaxGuru India Website.

14) As cited in ” Apex Court Observations and Findings Para” in “Series of Judicial Pronouncement – Insolvency and Bankruptcy Code, 2016” by Rushabh Ajmera 11 Months ago on TaxGuru India Website.

15) As cited in “IBC (Insolvency and Bankruptcy Code, 2016) – The Bankruptcy Law of India” written by Vidushi Trehan, LL.M from Symbiosis Law School, Pune , Intern at Khurana & Khurana, Advocates and IP Attorneys.

16) As cited in “Brief about decision para” in ” “and” occurring in section 8(2)(a) may be read as “or”- Mobilox Innovations (P) Ltd. Vs. Kirusa Software (P) Ltd.- Supreme Court” written by IBC LAWSon September 21, 2017.

17) As cited in “Case Name: M/S. Surendra Trading Company Vs. M/S. Juggilal Kamlapat Jute Mills Company Limited and Others” written by IBC LAWS on September 18, 2017

18) As cited in “RBI is authorised to direct any banking company to initiate insolvency resolution process- Essar Steel India Ltd. Vs. RBI- Gujarat High Court” written on July 17, 2017 by IBC LAWS.

19) As cited in “The Insolvency And Bankruptcy Code In 2019 : Recent Amendments And Key Judgments” written by Mayur Shetty and Chintan Gandhi of Rajani Associates on 12th March 2020.

20) As cited in “Delay becomes the norm in insolvency & bankruptcy cases” by Joel Rebello & Saikat Das, ET Bureau on Aug 15, 2019 at 11:25pm.

21) As cited in “Hidden factors that slow our courts and delay justice” written by Arghya Sengupta.

22) As cited in “Insolvency And Bankruptcy Code” written on 12 September 2017 by Samvad Partners.

23) As cited in “2016: Overview Of The Insolvency And Bankruptcy Code, 2016” written by Namrata Bhagwatula , Senior Associate on 20 September, 2018.

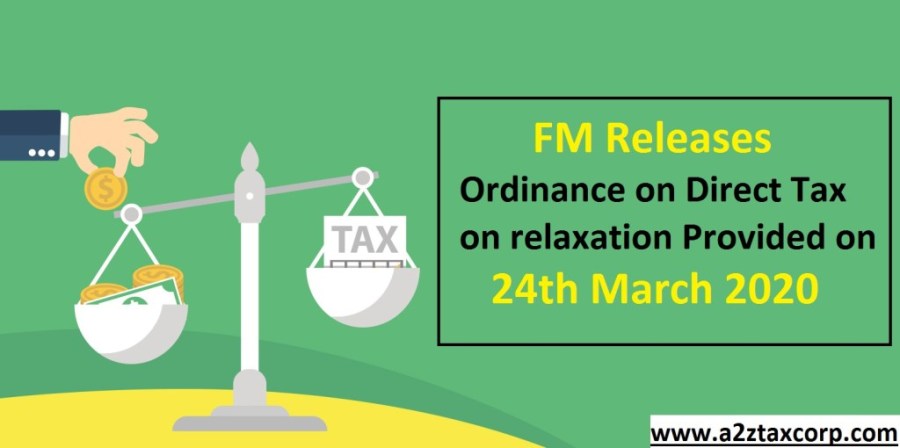

As the world battles the COVID-19 pandemic, countries are moving to stringent measures like lockdowns and curfews. With markets crashing, the global economy is staring at a deep distress.

Entire world is fighting against epidemic COVID 19 outbreak and Hon’ble Prime Minister of India Sh. Narendra Damodardas Modi has taken much need precautionary step of complete lockdown from midnight 12’o clock of 24th March, 2020 onwards for next 21 days and again extended to 3rd May, 2020 for another 19 days.

In this difficult environment, each regulatory body is releasing relief measures and guidelines for easing out the impact of COVID 19. On the financial and compliance front, announcements have been flowing from the Government authorities in the form of deferment of statutory due dates or relaxation in payment terms to overcome the financial crisis being faced due to lock-down.

Similar to several countries, the Government of India has begun working on an economic package to deal with the impact of the pandemic. Realising the hardships faced by its citizens, the Union Finance & Corporate Affairs Minister Smt. Niramla Sitharaman has announced several important relief measures on tax and regulatory aspects.

The Finance Minister also announced that necessary legal circulars and legislative amendments for giving effect to these relief measures will be issued by the concerned Authority.

Following is the summarised form of the key announcements made by the Finance Minister here below:

Direct Taxes

1. Extension of tax return filing deadline

The deadline for the following types of tax return have been extended from 31 March 2020 to 30 June 2020

Belated income-tax return for tax year 2018-19

Revised income-tax return for tax year 2018-19

2. The timeline for linking Aadhaar with PAN has been extended to 30 June 2020

3. Relief with regards to delay in payment of taxes

Interest at the reduced rate of 9% (i.e. 0.75% per month instead of 1/1.5 percent per month) will be charged on delay in respect of following payments made between 20 March 2020 and 30 June 2020:

Advanced tax

Self-assessment tax

Regular tax

Taxes withheld or collected at source

Equalization levy

Securities Transaction Tax and

Commodities Transaction Tax

Penalty and late fees in relation to the above mentioned payments are to be waived off

4. Extension of compliance due dates

In respect of the following, where the due dates fall between 20 March 2020 and 29 June 2020, the revised due dates shall be 30 June 2020:

Issue of notice

Intimation

Notification

Approval order

Sanction order

Filing of appeal

Furnishing of return, statements, applications, reports, any other documents

Completion of proceedings by the authority and

Any compliance by the taxpayer including investment in saving instruments or investments for roll over benefit of capital gains

5. The Direct Tax Vivad se Vishwas Act, 2020:

The timeline for payment of disputed arrears without attracting additional 10% amount under the Vivad se Vishwas Scheme extended from 31 March 2020 to 30 June 2020.

Indirect Taxes

1. Extension of GST return filing deadlines:

The last date for filing the forms GSTR-3B due in months of March, April and May 2020 (i.e. returns of February, March and April 2020) will be extended till 30 June 2020 (in staggered manner)

Date for filing GST annual returns of FY 18-19, which is due on 31 March 2020 is extended till the last week of June 2020

2. Relief in respect of payment of taxes

For those having aggregate annual turnover less than INR 50mn, no interest, late fee, and penalty will be charged for the period

However, for those having an aggregate annual turnover of more than INR 50mn, a reduced rate of interest @ 9% per annum will be charged from 15 days after due date (current interest rate is 18 % per annum) for the delayed payment between 20 March 2020 and 30 June 2020, but no late fee and penalty will be charged if complied before 30 June 2020

Last date for making payments by the Composition dealers for the quarter ending 31 March 2020 will be extended till the last week of June 2020

Payment under Sabka Vishwas Scheme shall be made without interest till 30 June 2020

3. Extension of compliances due dates

In respect of the following under GST law, where the due date falls between 20 March 2020 and 29 June 2020, shall be extended to 30 June 2020:

Issue of notice

Notification

Approval order

Sanction order

Filing of appeal and

Furnishing of return, statements, applications, reports, any other documents

4. Date for opting for composition scheme for the F.Y. 2020-2021 is extended till 30 June 2020

5. 24X7 Custom clearance till end of 30 June 2020

Corporate Laws

1. CARO 2020

Applicability of Companies (Auditor’s Report) Order, 2020 will be effective from FY 2020-2021

2. Board meeting

The mandatory requirement of holding Board meetings within prescribed interval provided by the Companies Act, 2013 (120 days) shall be extended by a period of 60 days till next two quarters i.e. till 30 September

3. Meeting of Independence Directors

For FY 2019-20, if mandatory one meeting of independent directors is not held, the same will not be treated as non-compliance

4. Form INC-20A- Declaration of commencement of Business

New Companies being given 6 more months for filing declaration of commencement of business

5. Debenture

Time line to invest 15% of debentures maturing in a particular year has been extended from 30 April 2020 to 30 June 2020

6. Deposit Reserve

Requirement of creating a Deposit Reserve (equal to 20%) of deposits maturing during FY 20-21, extended to 30 June 2020 instead of 30 April 2020

7. Minimum residency

Non-compliances with 182 days residency in India by Director will not treated as non-compliance

8. No Additional Fees

Moratorium period from 1 April 2020 to 30 September 2020, during which no additional fee would be charged in respect of any filing, irrespective of its due date

9. Insolvency and Bankruptcy Code 2016 (IBC)

Minimum amount of default required to initiate insolvency and liquidation on corporate debtors raised from INR 1 lakh to INR 1 crore, effective immediately, in order to prevent admission of MSMEs defaulting due to economic conditions in lieu of COVID-19

Proposed Suspension of new initiations of Corporate Insolvency Resolution Process under Sections 7, 9 and 10 of IBC for 6 months, contingent upon scenario beyond 30 April 2020 as a safeguard companies from defaults attributable to financial downturn pursuant to the COVID-19 pandemic

Among the measures announced late on Tuesday, the government extended the e-way bill validity for the second time since the lockdown was imposed. The e-way bill generated on or before March 24 and expiring during the March 20-April 15 period would now be valid till May 31. This is likely to help trucks stuck en route to reach their destinations.

Further, the notification extended by three months the deadline for furnishing the annual return and GST audit for financial year 2018-19 to September 30. Additionally, a taxpayer can now furnish monthly return GSTR-3B showing nil sales through SMS using the registered mobile number. This return would be verified by a registered mobile number based one-time password (OTP) facility, the notification said.

The Indian economy is one of the most robust economies in the World and one of the key components which constitutes it significantly is known as Job work. So what’s the definition of Job Work?

Definition

As per Section 2(68) of the CGST Act, 2017 Job Work is defined as ‘any treatment or process undertaken by a person on goods belonging to another registered person’.

Meaning

Job-work means it is the processing of goods supplied by principal. The job worker is required to carry out the process specified and it includes outsourced activities that may or may not culminate into manufacture.

The one who does the said job would be termed as ‘job worker’. The ownership of the goods does not transfer to the job worker but it rests with the principal.

About the Concept

The concept of job work is stated and explained in the Central Excise. It is a concept wherein a principal manufacturer can send an input or semi-finished good to a job worker for further processing.

Many facilities and procedural concessions have been given to the job workers as well as the principal supplier who sends goods for job work.

The whole idea behind this is that the principal must be made responsible for meeting the compliances on behalf of the job worker on the goods processed by the worker.

One must also consider the fact that typically the job-workers are small persons who are unable to comply with the discrete provisions of the law.

The most relevant and pertinent point is what are the Procedural aspects that have to be dealt with in regards to the Job Work?

Certain facilities with the specific conditions are offered in relation to job work some of which are as under:

a) A registered person (Principal) can send inputs/capital goods under intimation and subject to the certain conditions without payment of tax to a job worker and from there to another job worker and after completion of job work bring back such goods without payment of tax.

The principal is not required to reverse the ITC availed on inputs or capital goods dispatched to job worker.

b) Principal can send inputs or capital goods directly to the job worker without bringing them to his premises, still the principal can avail the credit of tax paid on such inputs or capital goods.

c) However, inputs and/or capital goods sent to a job worker are required to be returned to the principal within 1 year and 3 years,respectively, from the date of sending such goods to the job worker.

d) After processing of goods, the job worker may clear the goods to-

(i) Another job worker for further processing;

(ii) Dispatch the goods to any of the place of business of the principal without payment of

(iii) Remove the goods on payment of tax within tax;

(iv) India or without payment of tax for export outside India on fulfilment of conditions.

The facility of supply of goods by principal to the third party directly from the premises of the job worker on payment of tax in India likewise with or without payment of tax for export may be availed by the principal on declaring premise of the job worker as his additional place of business in registration. In case the job worker is a registered person under GST, even declaring the premises of the job worker as additional place of business is not required.

Before supply of goods to job worker, principal would be required to intimate the Jurisdictional Officer containing the details of description of inputs intended to be sent by the principal and the nature of processing to be carried out by the job worker.

The said intimation shall also contain the details of another job worker, if any. The inputs or capital goods shall be sent to the job worker under the cover of a challan issued by the principal.

The challan shall be issued even for the inputs or capital goods sent directly to the job worker. The challan shall contain the details specified in Rule 10 of the Invoice Rules.

The responsibility for keeping proper accounts for the inputs or capital goods shall lie with the principal.

Input Tax credit on goods supplied to job worker under Section 19 of the CGST Act, 2017 provides that the principal (a person supplying taxable goods to the job worker) shall be entitled to take the credit of input tax paid on inputs sent to the job- worker for the job work.

Further, the proviso also provides that the principal can take the credit even when the goods have been directly supplied to the job worker without bringing into the premise of the principal.

The principal need not wait till the inputs are first brought to his place of business.

Time Limits for return of processed goods

As per section 19 of the CGST Act, 2017, inputs and capital goods after processing shall be returned back to principal within one year or three years respectively of their being sent out.

Extended meaning of input

As per the explanation provided in section 143 of the CGST Act, 2017, where certain process is carried out on the input before removal of the same to the job worker, such product after carrying out the process to be referred as the intermediate product.

Waste clearing provisions

Pursuant to section 143 (5) of the CGST Act, 2017, waste generated at the premises of the job worker may be supplied directly by the registered job worker from his place of business on payment of tax or s such waste

may be cleared by the principal, in case the job worker is not registered.

Transitional provisions

Inputs or partially processed inputs which are sent to a job worker prior to introduction of GST under the provisions of existing law [Central Excise] and if such goods are returned within 6 months from the appointed day i.e. 1st July, 2017 no tax would be payable.

If such goods are not returned within prescribed time, the input tax credit availed on such goods will be liable to be recovered.

If manufactured goods are removed, prior to the appointed day, without payment of duty for testing or any other process which does not amount to manufacture, and such goods are returned within 6 months from the appointed day, then no tax will be payable.

For the purpose of these provisions during the transitional period, the manufacturer and the job worker are required to declare the details of such goods sent/received for job work in prescribed format GST TRAN-1, within 90 days of the introduction of the GST.

Conclusion

The tax treatment of job work under GST remains largely similar to the current regime. An important point to note is that the period within which inputs should be brought back or supplied from the job worker’s place is now 1 year instead of 180 days earlier.

Similarly, the period within which capital goods should be brought back or supplied is now 3 years instead of 1 year earlier. Also, GST will now be levied on processing charges charged by the job worker.

For the manufacturing industry, these provisions are positive and in line with the Government’s all-out support for the sector.

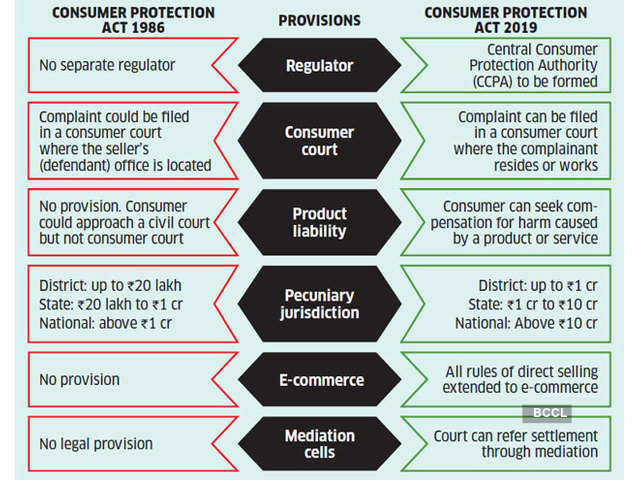

The Consumers can now cheer as the Consumer Protection Act, 2019 has recently replaced the three decade old Consumer Protection Act, 1986. The Consumer Protection Act, 2019 which came into effect on Monday (July 20) has replaced the earlier Consumer Protection Act, 1986.

The new Act as per the Experts say that “it gives more power to the consumers”. It seeks to revamp the process of administration and settlement of consumer disputes, with strict penalties, including jail term for adulteration and misleading ads by firms.

On July 20, 2020 certain provisions of the Consumer Protection Act, 2019 came into force as notified by the Central Government. Following the the key features of the relevant provisions:-

Key features of the Consumer Protection Act, 2019 which came into effect on July 20, 2020:-

1) Consumers can now institute a complaint from where they reside or work for gain.

2) The original pecuniary jurisdiction of the District Commissions has increased upto ₹1 crore from ₹20 lakh earlier.

3) The Pecuniary jurisdiction of State Commissions has been increased from ₹1 crore to Rs. 10 crore.

4) The National Commission can hear cases above ₹10 crore when compared to above ₹1 crore earlier.

5) While the provisions relating to e-commerce are not yet notified, a section relating to electronic service provider (covering software services, electronic payments) is notified.

6) The opposite party needs to deposit 50% of the amount ordered by the District Commission before filing an appeal before the State Commission. Earlier, the ceiling was a maximum of ₹25,000, which has been removed.

7) The limitation period for filing of appeals to the State Commission has been increased from 30 days to 45 days.

8) The Parties can be allowed to settle the disputes through mediation.

Following are the Sections which came into force:

Above mentioned provisions pertain to the Consumer Protection Councils, Consumer Disputes Redressal Forum, Mediation, Product Liability, punishment for manufacturing, selling, distributing etc spurious good or products which contain adulterant.

As per the rules, the e-commerce players will have to display the total ‘price’ of goods and services offered for sale along with break-up of other charges. Only a few certain miscellaneous provisions with regards and respect to the powers of the Central and State Government to make the rules and regulations have also been enforced.

On misleading advertisements there is provision for jail term and fine for manufacturers. There is no provision for jail for celebrities but they could be banned for endorsing products if it is found to be misleading.

For the first time there will be an exclusive law dealing with Product Liability. A manufacturer or product service provider or product seller will now be responsible to compensate for an injury or damage caused by the defective product or deficiency in services.

The Act has also defined an “e-commerce” as the buying or selling of goods or services including the digital products over digital or electronic networks. The existing definition of e-commerce has been adopted from India’s FDI Guidelines on e-commerce.

The definition of ‘e-commerce Entity’ as provided under the FDI Guidelines includes inventory and market place models.

There is also a provision for class action law suit for ensuring that rights of consumers are not infringed upon. The authority will have power to impose a penalty on a manufacturer or an endorser of up to 10 lakh rupees and imprisonment for up to two years for a false or misleading advertisement.

COMPANY COMPLIANCES DURING THE COVID-19 ERA: AN INTRODUCTION

The global outbreak of the novel coronavirus has taken the world by storm. While the issue pertaining to the public health is the talk of the town, the impact of COVID-19 on businesses and corporates seems to be least talked about.

Day to day business of the corporates is being affected due to decreased inflow of the human resource and a decrease in the workflow. While technologies have provided a relief to the human resource for physical attendances and conferences, there seemed to be unsettled trouble regarding legal compliances that required various filings and physical meetings.

Pursuant to the ongoing global COVID-19 pandemic and the Finance Minister, Ms. Nirmala Sitharaman’s announcements on March 24, 2020, the Ministry of Corporate Affairs (“MCA”) has issued various circulars to provide relief to companies from certain compliances under the Companies Act, 2013 (“Act”) and associated rules. This has been done as a measure to reduce the compliance burden on entities during the unprecedented health and economic situation caused by COVID-19. Following are the measures:-

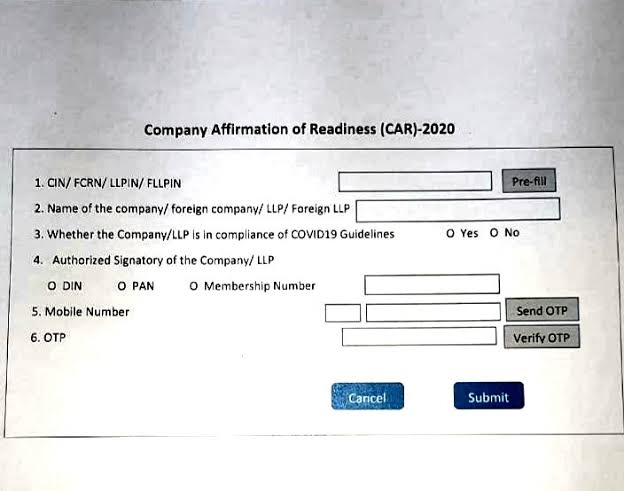

1. Company Affirmation of Readiness towards COVID-19

Social distancing has gained its importance as a way to contain the spread, morbidity, and mortality of COVID-19. Government of India (“GOI”), responsible for the public welfare at large, has realised that social distancing can be achieved in its true sense only if the employers of the Indian public make the same application in their respective premises.

Considering that major employers of the nation belong to the companies or limited liability partnership (“LLP”) type entity, GOI as part of disaster management have advised all companies/LLPs to put in place an immediate plan to implement the “work from home” policy as a temporary measure up till March 31, 2020.

Further, in case of a requirement of physical visits of the essential staff to such offices by the employers, staggered timings may be followed in order to minimize physical interactions of all kinds.

A simple webform for companies/LLP shall be deployed by MCA on March 23, 2020, in order to confirm the readiness of the employers to deal with COVID-19 threat. The webform shall be called CAR (Company Affirmation of Readiness towards COVID-19) and would be required to be signed and submitted by the authorised signatory of the company/LLP.

Therefore, it shall be expected by each company/LLP to ensure reporting of the compliance through CAR instantly from the date of its deployment.

2. Companies Fresh Start Scheme 2020

The MCA issued a circular on March 30, 2020, introducing the Companies Fresh Start Scheme, 2020 which, inter alia, grants a one-time opportunity to defaulting companies to complete all belated filings, including, without limitation, annual filings and filings required under IEPFA (Accounting, Audit, Transfer and Refund) Rules, 2016 in relation to transfer of money remaining unpaid or unclaimed for a period of seven years under Section 124(5) of the Act and transfer of relevant shares in the name of the ‘Investor Education and Protection Fund’ under Section 124(6) of the Act, with the MCA21 registry, without incurring additional fees on account of any delay.

This scheme came into force on April 1, 2020, and is valid till September 30, 2020. The application for seeking immunity for belated filings under this scheme should be made within a period of six months from September 30, 2020, through Form CFSS-2020. Thereafter, an immunity certificate will be provided by the designated authority on the basis of the declarations made in such form.

However, no immunity shall be provided under the scheme in a matter where (i) an appeal or management dispute is pending before any court or tribunal, or (ii) a court has ordered a conviction, or the adjudicating authority under the Act has imposed a penalty, and in respect of such orders, no appeal has been filed prior to the scheme coming into force.

Further, the scheme shall not apply: (i) where an application has been filed or an action for final notice for striking off the name of the company has already been initiated; (ii) where the company has been amalgamated; (iii) when application of obtaining dormant status has been filed; (iv) to vanishing companies; and/or (v) where charge related documents or an increase in authorised capital is involved.

3. CSR Spending

The MCA has by way of circular dated March 23, 2020 and the office memorandum dated March 28, 2020, clarified that the spending of CSR funds by companies in relation to COVID-19, including by way of contribution to the PM CARES Fund, is an eligible CSR expenditure under the Act.

The MCA has further clarified by way of FAQs dated April 10, 2020 that contributions made to the State Disaster Management Authority will also be eligible CSR activity, but contributions towards (a) ‘Chief Minister’s Relief Fund’ or ‘State Relief Fund for COVID-19’; and (b) payment of salary/ wages to employees and workers (including contract labour/ temporary/ casual/ daily wage workers) during the lockdown period will not be considered as eligible CSR expenditure.

However, ex-gratia payment over and above the disbursement of wages to temporary/ casual workers/ daily wage workers, specifically for the purpose of fighting COVID-19, will be admissible towards CSR expenditure, provided there is an explicit declaration to that effect by the board of the company, which is duly certified by the statutory auditor.

4. Meetings of Board and the Shareholders

The Companies (Meetings of Board and its Powers) Rules, 2014 were amended by a notification dated March 19, 2020, to enable companies to hold board meetings on the following matters (which earlier had to be necessarily held at a physical meeting) through video-conferencing or other audio-visual means (collectively “VCC”) till June 30, 2020: (i) approval of annual financial statements and board’s report; (ii) approval of prospectus; (iii) audit committee meetings for consideration of financial statements; and (iv) approval of amalgamation, merger, demerger, acquisition and takeover.

MCA has, by way of a general circular dated April 8, 2020, requested companies to pass all decisions of an urgent nature requiring shareholder approval, other than those of ordinary business or business where any person has right to be heard, through postal ballot/ e-voting in accordance with the relevant statutory provisions without holding a physical general meeting. However, in cases where holding an extraordinary general meeting (“EEGM”) is unavoidable, these have now been permitted to be held through VC until June 30, 2020. The circular further lays down certain conditions to be met for conducting an EGM through VC and the key conditions, inter alia, include: (i) attendance of at least one independent director (where a company is required to appoint one) and auditor (or his authorised representative who is qualified to be the auditor); (ii) maintenance of recorded transcripts of the EGM and, in case of a public company, such transcripts to be uploaded on the company website (if any); and (iii) e-voting facility being available. All other provisions relating to general meetings under the Act (and relevant rules) will continue to apply.

Due to difficulties faced by various stakeholders in serving and receiving notices/responses by post on account of COVID-19, the MCA, on April 13, 2020, provided that notice of EGMs to be held through VC (and for passing shareholder resolutions through postal ballot/ e-voting) may now be given to shareholders only through email addresses of the shareholders registered with the company or with the depository participant/ depository. This circular also specifies various conditions which companies must comply with while sending email notices to shareholders.

CONCLUSION

Business entities in India are requested and expected to keep an eye on the major government websites to ensure timely compliance with all such immediate requirements and mandates issued by GOI as need of the hour from time to time.

WEBSITES REFERRED:-

1) MCA General Circular No. 10/20 dated March 23, 2020 on Clarification on spending of CSR for COVID-19.

2) MCA General Circular No. 12/20 dated March 30, 2020 on Companies Fresh Start Scheme, 2020

3) MCA Notification dated March 19, 2020 on Companies (Meetings of Board and its Powers) Amendment Rules, 2020

4) MCA General Circular No. 14/2020 dated April 8, 2020 on Clarification on passing of ordinary or special resolutions by companies under the Companies Act, 2013 and rules made thereunder on account of threat posed by Covid-19.

5) MCA General Circular No. 17/20 dated April 13, 2020 on clarification on passing ordinary and special resolutions by companies under the Companies Act, 2013 and rules made thereunder on account of threat posed by COVID-19.

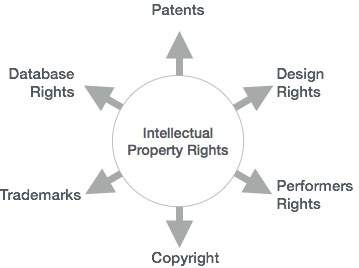

‘Intellect’ refers to the creations of the mind. Intellectual Property is a type of intangible property and includes inventions, literary and artistic works, symbols, names and paintings.

Intellectual Property Rights (IPRs) are the Rights granted to the creators of Intellectual Property (IP) by the Government. The nature of IPR is territorial. In any country an IP has to seek protection separately under the relevant laws.

Mechanisms which are Special in nature have been kept in place for various territories in order to provide protection to different types of IPRs. It confers an exclusive right to the inventor/ creator or assignee to fully utilize the invention/ creation for a given period of time.

It’s been established that the intellectual labor associated with the innovation should be given due importance so that public good emanates from it.

This is a strong tool, to protect investments, time, money, effort invested by the inventor/creator of an IP, since it grants the inventor/creator an exclusive right for a certain period of time for use of his invention/creation.

Hence it aids in the economic development of a country by promoting healthy competition and encouraging industrial development which shall also aid in the growth of the economy.

WHAT IS AN INTELLECTUAL PROPERTY?

Intellectual Property(IP) refers to creations of the mind; inventions; literary and artistic works; and symbols, names and images used in commerce.

IP is divided into two categories: 1) Industrial Property:- includes patents for inventions,trademarks, industrial designs and geographical indications. 2) Copyright:- covers literary works (such as novels,poems and plays), films, music, artistic works (e.g., drawings, paintings, photographs and sculptures) and architectural design.

In Intellectual property(IP), there are Rights which relates to the rights of performing artists in their performances, producers of phonograms in their recordings, and broadcasters in their radio and television programs are included.

WHAT ARE INTELLECTUAL PROPERTY RIGHTS?

So what do you mean by intellectual property rights? IP rights like any other property right allow creators, or owners, of patents, trademarks or copyrighted works to benefit from their own work or investment in a creation.

These rights are outlined in Article 27 of the UDHR which provides for the right to benefit from the protection of moral and material interests resulting from authorship of scientific, literary or artistic productions.

The importance of intellectual property was first recognized in the Paris Convention for the Protection of Industrial Property (1883) and the Berne Convention for the Protection of Literary and Artistic Works (1886). Both treaties are administered by the World Intellectual Property Organization (WIPO).

There are various pros which are more compelling than the cons.

1) The progress and well-being of humanity rest on its capacity to create and invent new works in the areas of technology and culture.

2) The legal protection of new creations and this encourages the commitment of additional resources for further innovation.

And Lastly the third pros is that the 3) Promotion and protection of intellectual property spurs economic growth, creates new jobs and industries, and enhances the quality and enjoyment of life.

An efficient and equitable intellectual property system can help all countries to realize intellectual property’s potential as a catalyst for economic development and social and cultural well-being. The intellectual property system helps strike a balance between the interests of innovators and the public interest, providing an environment in which creativity and invention can flourish.

INTELLECTUAL PROPERTY HOLDERS IN A QUANDARY DUE TO COVID-19 PANDEMIC

While experts are in a combat mode and the race is on to discover the cure for COVID-19, the claim of intellectual property rights for exclusive use of the cure poses a dilemma as it is not considered the most rational thing to do at the moment.

Carlos Correa addressed to organizations like WHO, WTO and WIPO via an open letter to seek support for WTO countries that invoke the ‘security exception’ contained in Article 73 of the Agreement on Trade Related Intellectual Property Rights (TRIPS) Agreement, to take ‘actions it considers necessary for the protection of its essential ‘security interests’ in the wake of COVID-19 threat.

It has been suggested that invocation of exception under Article 73 will be warranted to procure medical products and devices or to use the technologies to manufacture them as necessary to take cue of the present public health emergency.

By suspending the enforcement of any Intellectual Property right as given under Article 73(b) of TRIPS Agreement, an obstacle for the procurement or local manufacturing of the medical equipments shall be necessary in order to protect the population of the world will be outlasted.

The question which is raised due to the above is regarding IP rights which are aimed to aid the public by promoting technological advancement in return of providing the inventor an exclusive right over the invention, though for a limited time. Though the IP rights are at a standstill due to the outbreak the IP Registry offices all over have limited their functioning.

TYPES OF INTELLECTUAL PROPERTY

Trade Mark: –

A trademark is used in order to identify a business entity and it also differentiates the goods made or services offered by a company or an individual. Names, Words, Logos, Colors, Packaging, Sounds (audible), Signs (visual) or any combination thereof are considered and can be filed as trademarks.

A trademark must be Unique and Distinctive in nature and must also avoid adjectives for eg efficient and Names of person or places (E.g. India). Even Obscene words, Religious or Government words or symbols (E.g. OM) and Common Shapes (Square) should be avoided.

The Trade mark means a mark used in relation to goods for the purpose of indicating a connection in the course of trade between the goods and some person having the right as proprietor to use that mark.

The function of a trade mark is to give an indication to the purchaser or a possible purchaser as to the manufacture or quality of the goods, to give an indication to the trade source from which the goods come or the trade hands through which they pass on their way to the market.

The Trade Marks Act, 1999 is an act which provides for the registration and better protection of trademarks for goods and services and for the prevention of the use of fraudulent marks. A trade mark is valid for a period of 10 years.

Case Name: The Coca-Cola Company v. Bisleri International Pvt. Ltd Case Citation: Manu/DE/2698/2009

Copyright: –

Copyright is an exclusive legal right granted to the creators of an intellectual work. The owner of a Copyright has rights to reproduce, translate, adapt, perform, distribute and must be publicly allowed to display the work, etc.

Registration is not mandatory since copyright comes into existence as soon as the intellectual work is created but it is recommended to register a copyright for better enforceability, since registered copyrights have more evidentiary value in court.

(a) Types of Works covered under Copyright:-

(1) Literary including Software – Books, Essay, Compilations, Computer Programs.

(2) Artistic – Drawing, Painting, Logo, Map, Chart, Plan, Photographs, Work of Architecture.

(3) Dramatic – Screenplay, Drama.

(4) Musical – Musical Notations.

(5) Sound Recording – Compact Disc.

(6) Cinematograph Films – Visual Recording which includes sound recording.

(b) Duration of Copyright:-

(1) Literary, Dramatic, Musical or Artistic Works – Lifetime of the author + 60 years from the death of the author.

(2) Anonymous & Pseudonymous Works – 60 years from the year the work was first published.

(3) Works of Public Undertakings & Government Works – 60 years from the year the work was first published.

(4) Works of International Organizations – 60 years from the year the work was first published.

(5) Sound Recording – 60 years from the year in which the recording was published.

(6) Cinematograph Films – 60 years from the year in which the film was published.

Case Name:- Indian Performing Rights Society Ltd. v. Eastern India Motion Picture Association Case Citation: – 1977 SCR (3) 206

Designs: – The Design Act, 2000 states that it protects the aesthetic and ornamental features of an object. As per the Act a 2D or 3D pattern of a handicraft, a product, or even an industrial commodity.

The Unique Selling Point (USP), protects the looks and feels of the product and it prevents the duplication of the product. An industrial design helps in drawing a customer’s attention and helps in increasing the commercial value of an article.

Case Name:-Cello Household Products v. M/S Modware India and anr Case Citation:- Notice of Motion (L) No. 209/2017 in Suit (L) No. 48/2017

Patents On the 4th December, 2018, The Ministry of Commerce and Industry released the draft (rules amendment) for Patents Act 1970. These rules are mainly amended with respect to international applications, patent opposition and a few form related extensions. The Central Government proposes to make these amendments in exercise of the powers conferred by section 159 of the Patents Act, 1970.In order to align with TRIPS, inventions which are not patentable have been included even, wider rights of patentee is incorporated. Uniform period of protection is 20years. Case Name: Bajaj Auto Limited v.TVS Motor Company Limited. Case Citation: JT 2009 (12) SC 103

5. Integrated Circuits

Semiconductor Integrated Circuits Layout Design (SICLD) Act 2000 states the meaning of Semi conductor Integrated Circuit as, a product having transistors and other circuitry elements designed to perform an electronic circuitry function. There are 2 types of designs as per the act:-

(i) Layout Design – A layout of transistors and other circuitry elements including lead wires which connects semiconductor integrated circuits.

(ii) Layout-Design Registry (SICLDR) is the office where the applications on Layout-Designs of integrated circuits are filed for registration. The jurisdiction of this Registry is whole of India. The Registry, as per the guidelines laid down in the Semiconductor Integrated Circuits Layout Design (SICLD) Act 2000 and the Semiconductor Integrated Circuits Layout-Design (SICLD) Rules 2001, examines the layout-designs of the Integrated Circuits and issues the Registration Certificate to the original layout-designs of the Semiconductor Integrated Circuits.

Case Name: Sunil Alag v. Union of India and Others Case Citation: W.P. (C) 8152/2013

6. Biological Diversity

The Biological Diversity Act 2002 was enacted to realize the objectives enshrined in the United Nations Convention on Biological Diversity (CBD) 1992 which was passed by the Lok Sabha on 2nd December 2002 and by the Rajya Sabha on 11th December 2002.

It recognizes the sovereign rights of states to use their own Biological Resources due to the scarcity and also to conserve it. The Act provides for a mechanism for equal sharing of benefits arising out of the use of traditional biological resources and knowledge. It is a federal legislation enacted by the Parliament of India for preservation of biological diversity in India.

Case Name: Environment Support Group vs National Biodiversity Authority Case Citation: W.P. No.41532 / 2012

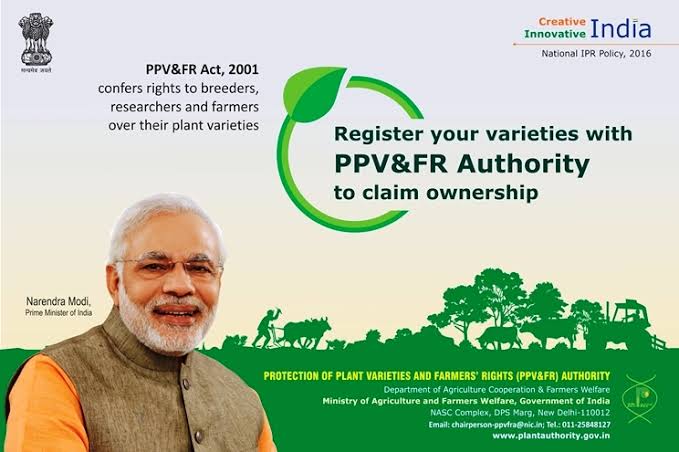

7. Plant Varieties and Farmers

Protection of Plant Varieties and Farmer’s Rights Act of 2001(PPV & FR Act, 2001) confers right to breeders, researchers and farmers over their plant varieties. Reaching legislation with regards to establishing rights for farmers to save, use, exchange and sell farm saved seed.

The Act establishes nine rights for farmers of which the most important in this regard are the right to “seed” and the right to “compensation” for crop failure (Art. 39). Not only does the 2001 Act protect the rights of framers to save, use, exchange and sell farm- saved seed, it also seeks to ensure that these seeds are of good quality, or at least that farmers are adequately informed about the quality of seed they buy.

In addition, safeguards are provided against innocent infringement by farmers. Farmers who unknowingly violate the rights of a breeder are not to be punished if they can prove that they were not aware of the existence of such a breeder’s right (Art 42).

Case Name:- Monsanto Technology LLC & Ors Vs. Nuziveedu Seeds Ltd & OrsHigh Court of Delhi Case Citation: CS (Comm) 132/2016

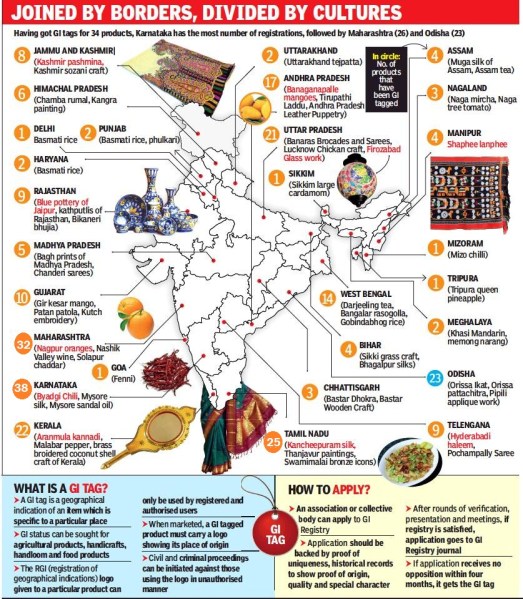

The Geographical Indication of Goods:- The Geographical Indications of Goods (Registration and Protection) Act, 1999 states Geographical Indication as it is primarily an agricultural or food product, natural or a manufactured product (handicrafts, Handloom textiles or industrial goods) originating from a definite geographical territory. A product is considered to be manufactured in a territory if any one of the activities of either the production or of processing or preparation of the goods takes place there. It promotes the producers prosperity of goods which have been produced in the geographical territory.

It helps the producer community to differentiate its products from other competing products that are present in the market and generate goodwill around its products. Hence, it acts as a signaling device by helping consumers to identify genuine quality products.

Case Name:- Tea Board Vs ITC Limited on 20 April, 2011 Case Citation:- GA No. 3137 of 2010 CS No. 250 of 2010

It has been suggested that invocation of exception under Article 73 will be warranted to procure medical products and devices or to use the technologies to manufacture them as necessary to take cue of the present public health emergency.

CONCUSION

The above overview clearly depicts that India has adopted and adhered to the latest IPR Regime and it has forayed into the global trade competition with a double edged sword.

You must be logged in to post a comment.