Maharashtra is home to some of India’s most prestigious universities, known for their academic excellence, research, and diverse programs. Here are the top universities in Maharashtra:

Indian Institute of Technology Bombay (IIT Bombay), Mumbai: One of India’s leading engineering and research institutions, renowned for its cutting-edge research, innovation, and top-ranked programs in engineering, technology, and sciences.

University of Mumbai, Mumbai: One of India’s oldest universities, offering a wide range of undergraduate, postgraduate, and doctoral programs in arts, science, commerce, law, and management.

Savitribai Phule Pune University (SPPU), Pune: A well-regarded public university offering a diverse array of programs in arts, science, commerce, engineering, and management, known for its research contributions.

Institute of Chemical Technology (ICT), Mumbai: A premier institute specializing in chemical engineering, technology, and applied sciences, known for its research and industry collaborations.

Tata Institute of Social Sciences (TISS), Mumbai: A prestigious institute offering programs in social sciences, humanities, public policy, and social work, with a strong focus on research and societal impact.

Symbiosis International (Deemed University), Pune: A leading private university offering diverse programs in management, law, humanities, and health sciences, known for its international collaborations and industry connections.

Narsee Monjee Institute of Management Studies (NMIMS), Mumbai: A top private university offering programs in management, engineering, commerce, law, and health sciences, with a focus on innovation and entrepreneurship.

Dr. Babasaheb Ambedkar Marathwada University, Aurangabad: A prominent public university offering a variety of programs in arts, science, commerce, law, and management, with a focus on regional development.

Maharashtra Institute of Technology (MIT), Pune: A leading private institute offering programs in engineering, technology, management, and humanities, known for its academic rigor and innovation.

Shivaji University, Kolhapur: A well-known public university offering programs in arts, science, commerce, and engineering, with a strong emphasis on research and community engagement.

These universities are recognized for their contributions to higher education, research, and innovation in Maharashtra, making them top choices for students across India.

Foreign Exchange (forex or FX) is the trading of one currency for another. For example, one can swap the U.S. dollar for the euro. Foreign exchange transactions can take place on the foreign exchange market, also known as the forex market.

The forex market is the largest, most liquid market in the world, with trillions of dollars changing hands every day. There is no centralized location. Rather, the forex market is an electronic network of banks, brokers, institutions, and individual traders (mostly trading through brokers or banks).

Understanding Foreign Exchange

The market determines the value, also known as an exchange rate, of the majority of currencies. Foreign exchange can be as simple as changing one currency for another at a local bank. It can also involve trading currency on the foreign exchange market. For example, a trader is betting a central bank will ease or tighten monetary policy and that one currency will strengthen versus the other.In the forex market, currencies trade in lots, called micro, mini, and standard lots. A micro lot is 1,000 worth of a given currency, a mini lot is 10,000, and a standard lot is 100,000. This is different than when you go to a bank and want $450 exchanged for your trip. When trading in the electronic forex market, trades take place in set blocks of currency, but you can trade as many blocks as you like. For example, you can trade seven micro lots (7,000), three mini lots (30,000), or 75 standard lots (7,500,000).

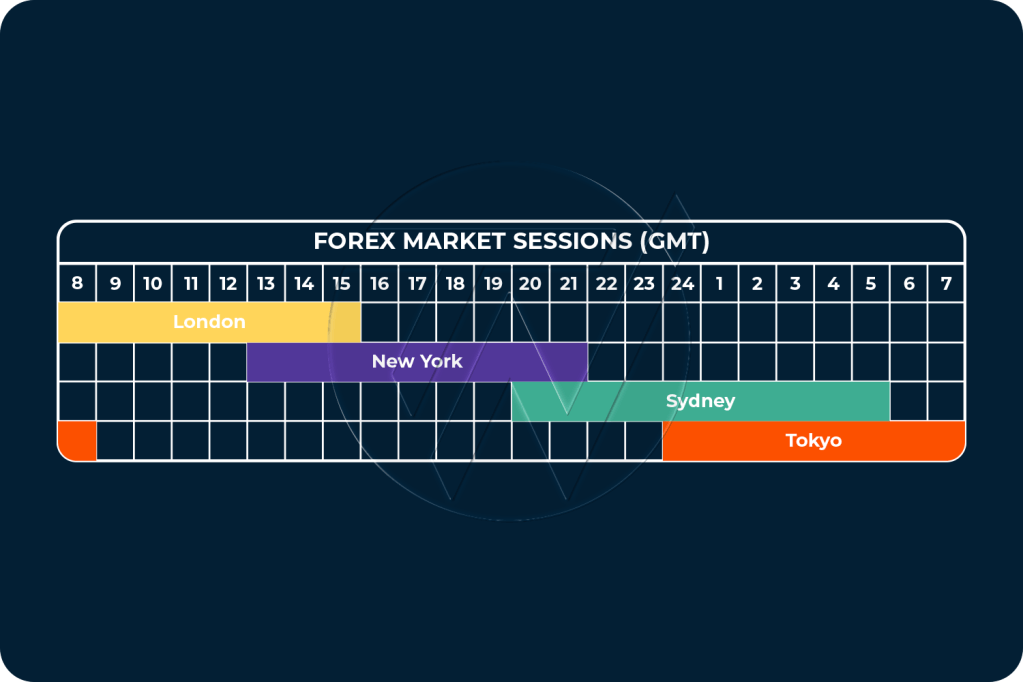

Images created and referenced from Trade Nation – What time does the forex market open. All distribution rights belong to the publisher and cannot be used without written permission.

The foreign exchange market is unique for several reasons, mainly because of its size. Trading volume in the forex market is generally very large. As an example, trading in foreign exchange markets averaged $6.6 trillion per day in April 2019, according to the Bank for International Settlements, which is owned by 63 central banks and is used to work in monetary and financial responsibility. The largest trading centers are London, New York, Singapore, Hong Kong, and Tokyo.

Trading in the Foreign Exchange Market

The market is open 24 hours a day, five days a week across major financial centers across the globe. This means that you can buy or sell currencies at any time during the day.

The foreign exchange market isn’t exactly a one-stop-shop. There are a whole variety of different avenues that an investor can go through in order to execute forex trades. You can go through different dealers or through different financial centers which use a host of electronic networks.

From a historical standpoint, foreign exchange was once a concept for governments, large companies, and hedge funds. But in today’s world, trading currencies is as easy as a click of a mouse—accessibility is not an issue, which means anyone can do it. Many investment companies offer the chance for individuals to open accounts and trade currencies however and whenever they choose.

When you’re making trades in the forex market, you’re basically buying or selling the currency of a particular country. But there’s no physical exchange of money from one hand to another. That’s contrary to what happens at a foreign exchange kiosk—think of a tourist visiting Times Square in New York City from Japan. They may be converting their (physical) yen to actual U.S. dollar cash (and may be charged a commission fee to do so) so they can spend their money while they’re traveling.

But in the world of electronic markets, traders are usually taking a position in a specific currency, with the hope that there will be some upward movement and strength in the currency that they’re buying (or weakness if they’re selling) so they can make a profit. Get the latest 1 US Dollar to Turkish Lira rate for FREE with the original Universal Currency Converter.

There are some fundamental differences between foreign exchange and other markets. First of all, there are fewer rules, which means investors aren’t held to as strict standards or regulations as those in the stock, futures, or options markets. That means there are no clearing houses and no central bodies that oversee the forex market.

Second, since trades don’t take place on a traditional exchange, you won’t find the same fees or commissions that you would on another market. Next, there’s no cutoff as to when you can and cannot trade. Because the market is open 24 hours a day, you can trade at any time of day. Finally, because it’s such a liquid market, you can get in and out whenever you want and you can buy as much currency as you can afford.

The Spot Market

Spot for most currencies is two business days; the major exception is the U.S. dollar versus the Canadian dollar, which settles on the next business day. Other pairs settle in two business days. During periods that have multiple holidays, such as Easter or Christmas, spot transactions can take as long as six days to settle. The price is established on the trade date, but money is exchanged on the value date.

Per an April 2019 foreign exchange report from the BIS, the U.S. dollar is the most actively traded currency.3 The most common pairs are the USD versus the euro, Japanese yen, British pound, and Australian dollar.4 Trading pairs that do not include the dollar are referred to as crosses. The most common crosses are the euro versus the pound and yen.

The spot market can be very volatile. Movement in the short term is dominated by technical trading, which focuses on direction and speed of movement. People who focus on technicals are often referred to as chartists. Long-term currency moves are driven by fundamental factors such as relative interest rates and economic growth.

The Forward Market

A forward trade is any trade that settles further in the future than spot. The forward price is a combination of the spot rate plus or minus forward points that represent the interest rate differential between the two currencies. Most have a maturity of less than a year in the future but longer is possible. Like with a spot, the price is set on the transaction date, but money is exchanged on the maturity date.

A forward contract is tailor-made to the requirements of the counterparties. They can be for any amount and settle on any date that is not a weekend or holiday in one of the countries.

The Futures Market

A futures transaction is similar to a forward in that it settles later than a spot deal, but is for standard size and settlement date and is traded on a commodities market. The exchange acts as the counterparty.

Example of Foreign Exchange

A trader thinks that the European Central Bank (ECB) will be easing its monetary policy in the coming months as the Eurozone’s economy slows. As a result, the trader bets that the euro will fall against the U.S. dollar and sells short €100,000 at an exchange rate of 1.15. Over the next several weeks the ECB signals that it may indeed ease its monetary policy. That causes the exchange rate for the euro to fall to 1.10 versus the dollar. It creates a profit for the trader of $5,000.

By shorting €100,000, the trader took in $115,000 for the short sale. When the euro fell, and the trader covered their short, it cost the trader only $110,000 to repurchase the currency. The difference between the money received on the short-sale and the buy to cover it is the profit. Had the euro strengthened versus the dollar, it would have resulted in a loss.

How Big Is the Foreign Exchange Market?

The foreign exchange market is extremely liquid and dwarfs, by a huge amount, the daily trading volume of the stock and bond markets. According to the latest triennial survey conducted by the Bank for International Settlements (BIS), trading in foreign exchange markets averaged $6.6 trillion per day in 2019.2 By contrast, the total notional value of U.S. equity markets on Dec. 31, 2021, was approximately $393 billion.5 The largest forex trading centers are London, New York, Singapore, Hong Kong, and Tokyo.

What Is Foreign Exchange Trading?

When you’re making trades in the forex market, you’re basically buying the currency of a particular country and simultaneously selling the currency of another country. But there’s no physical exchange of money from one hand to another. Traders are usually taking a position in a specific currency, with the hope that there will be some strength in the currency, relative to the other currency, that they’re buying (or weakness if they’re selling) so they can make a profit. In today’s world of electronic markets, trading currencies is as easy as a click of a mouse.

How Does Foreign Exchange Differ From Other Markets?

There are some fundamental differences between foreign exchange and other markets. There are no clearing houses and no central bodies to oversee the forex market which means investors aren’t held to the strict standards or regulations as those in the stock, futures, or options markets. Second, there aren’t the fees or commissions that exist for other markets that have traditional exchanges. There is no cutoff time for trading, aside from the weekend, so one can trade at any time of day. Finally, its liquidity lends to its ease of trading access.

A trading account is a financial account used to buy and sell securities like stocks, bonds, options, commodities, and other financial instruments. Here’s a breakdown of the key aspects:

Definition:

A trading account is typically opened with a brokerage firm or a financial institution that allows individuals or entities to execute trades in various financial markets. It serves as a gateway for investors and traders to access different exchanges and instruments.

How to Open:

Choose a Brokerage: Research and select a brokerage firm that suits your trading preferences, considering factors like fees, available markets, user interface, and customer support.

Application Process: Visit the brokerage’s website or office to fill out an application form. This usually requires personal information, identification, and financial details.

Funding: Once your account is approved, you’ll need to deposit funds into the trading account to start trading.

Margin Requirements:

What is Margin?: Margin is the amount of money required to open or maintain a leveraged position. It allows traders to control larger positions with a smaller amount of capital.

Margin Accounts: Some brokerages offer margin accounts, allowing traders to borrow funds to trade securities. The broker will have specific margin requirements, outlining the minimum amount of capital needed to open and maintain positions.

Margin Calls: If the value of the securities held in a margin account falls below a certain level (the maintenance margin), the broker may issue a margin call, requiring the trader to deposit more funds to cover potential losses or risk having their positions liquidated.

Remember, margin trading involves higher risk due to the amplified exposure to the market. It’s crucial to understand the risks and be well-versed in trading practices before engaging in margin trading.

Always consult with a financial advisor or do thorough research before opening a trading account or engaging in any trading activity. Regulations and specific requirements may vary based on the country and the brokerage.

To check the domestic prices and to ensure domestic food security, the Government has been taking measures to restrict export of rice from India. The export of non-basmati white rice was prohibited on 20thJuly 2023.

It has been noticed that despite restriction on certain varieties, rice exports have been high during the current year. Up to 17th August 2023, total exports of rice (other than broken rice, export of which is prohibited) were 7.33 MMT compared to 6.37 MMT during the corresponding period of previous year, registering an increase of 15.06%. There has been a spurt in the export of parboiled rice and Basmati rice; both of these varieties did not have any restriction on exports. While the export of parboiled rice has grown by 21.18% (3.29 MMT during the current year compared to 2.72 MMT during previous year), export of Basmati rice has increased by 9.35% (1.86 MMT during the current year compared to 1.70 MMT during previous year). Export of non-basmati white rice, which had an export duty of 20% since 9th September 2022 and has been prohibited w.e.f. 20th July 2023, has also registered an increase of 4.36% (1.97 MMT compared to 1.89 MMT during previous year). On the other hand, as per third Advanced Estimate of Department of Agriculture & Farmers Welfare, during the Rabi Season 2022-23, the production was only 158.95 LMT against 184.71 LMT during Rabi Season of 2021-22 i.e., there was a decline of 13.84%.

Internationally, due to strong demand from Asian buyers, production disruptions registered in 2022/23 in some major producing countries like Thailand, and fears of possible adverse effect of the onset of El Nino, international rice prices have also been rising continuously since last year. The FAO Rice Price Index reached 129.7 points in July 2023; its highest value since September 2011, registering an increase of 19.7% over past year levels. As the prices of Indian rice are still cheaper than the international prices, there has been a strong demand for Indian rice, resulting in record exports during 2021-22 and 2022-23.

The Government has received credible field reports regarding misclassification and illegal export of non-basmati white rice, export of which has been prohibited with effect from 20th July 2023. It has been reported that non-basmati white rice is being exported under the HS codes of parboiled rice and Basmati rice.

As the Agricultural & Processed Food Products Export Development Authority (APEDA) is responsible for regulation of export of Basmati rice and already has a web-based system in place for the purpose, the Government has issued following instructions to APEDA to introduce additional safeguards to prevent the possible illegal exports of white non-basmati rice in the garb of Basmati rice:

Contracts for Basmati exports with the value of USD 1200 per MT only and above should be registered for issue of Registration – cum – Allocation Certificate (RCAC).

Contracts with the value of below USD 1200 per MT may be kept in abeyance and may be evaluated by a committee to be set up by the Chairman, APEDA, for understanding the variation in prices and use of this route for export of non-Basmati white rice. It has been noted that there has been large variation in the contract price of Basmati being exported with lowest contract price being USD 359 Per MT in backdrop of average export price of USD 1214 per MT during the current month. The Committee should submit its report within a period of one month, whereafter a decision on lower price exports of Basmati planned by industry can be taken appropriately.

APEDA should hold consultations with trade to sensitize them about the matter and work with them to discourage any use of this window for export of non-basmati white rice.

With Fintech adoption rate at 87% against the global average of 64%, India has emerged as one of the largest digital markets in the world. Fintech Sector has huge potential in India, supported by an enabling policy and digital infrastructure framework.

As per industry estimate, India has over 676 million smartphone users, over 1.2 billion telecom subscribers (wireless + wireline) and 825 million internet subscribers of which approximately 39% belong to the rural areas (as on March 2021).

Further, total number of transactionsrelated to digital payments, a key enabler for expansion of digital markets, has increased from 2,071 crore in FY 2017-18 to 5,554 crore in FY 2020-21. As on date, more than 5179 crore transactions have been reported in the current financial year.

Furthermore, India now hosts the 3rd largest ecosystem for startups globally; 59,593 startups have been recognized by DPIIT across 57 unique industries, of which 1,860 startups belong to the FinTech sector. As of December 2021, India has over 17 Fintech companies, which have gained ‘Unicorn Status’ with a valuation of over USD 1 billion.

As regards to investment inflow in the Fintech sector, no such data is maintained centrally.

Government has taken several measures to increase investment inflows in Fintech sector.The Pradhan Mantri Jan DhanYojana (PMJDY) has been targeted at increasing financial inclusion in India by helping in new bank account enrollment of beneficiaries for direct benefits transfer and accessibility to a host of financial services applications. This has enabled Fintech startups to build technology products to penetrate the large consumer base in India.

Aadhar, the unique biometric identification system, allows the public to access government digital services thereby improving the availability and transparency for social payments including financial assistance to those in need.

Unified Payments Interface is single platform that merges various banking services and features under one umbrella and has been built as a scalable payments platform supporting digital payments in India.

Jan DhanYojana, Aadhar and Mobile (JAM trinity) alongwith Unified Payments Interface have been instrumental in bringing in transparency, integrity and timely delivery of financial benefits and services to the public.

Key initiatives undertaken by the Government for the Fintech ecosystem in India are listed below:

Jan DhanYojana has been targeted at increasing financial inclusion in India by helping in new bank account enrollment of beneficiaries for direct benefits transfer and accessibility to a host of financial services applications. This has enabled Fintech startups to build technology products to penetrate the large consumer base in India

India Stack is a societal initiative aimed at building public digital infrastructure to promote public and private digital initiatives including accelerated adoption of technology in finance

Aadhar, the unique biometric identification system, has allowed Aadhar Enabled Payment System and Aadhar Payment Bridge System:

Aadhar Enabled Payment System allows individuals to conduct financial transactions on a Micro-ATM by furnishing their Aadhaar number and verifying it with the help of their fingerprint/iris scan

Aadhar Payment Bridge System allows ease in bulk and recurring Government benefits and subsidy payments, facilitating operations from Aadhaar-linked bank accounts, using the biometric authentication

Development and roll-out of authentication solutions including digital KYC, video-based customer identification process, and digital signature on documentshas created various safeguards and a hassle-free system for Fintech startups and customers to leverage the technology-enabled solutions in the sector

A central repository, Central KYC, has been developed for reducing the hassle of undergoing multiple KYCs for different financial institutions. This allows the KYC process of consumers to be conducted only once unless there are any changes in consumer details

KYC and customer on boarding costs have been reduced significantly enabling expansion of financial services to rural India and opening their accounts

Unified Payments Interface has been built as a scalable payments platform supporting digital payments in India

License for Payments Banks has further helped in enhancing the financial inclusion drive in the country by allowing the setting-up of payments banks and expanding the access to payments/remittance services. In a bid to promote digital payments banks in the country, RBI has announced an increase to the maximum end of day balance for payment banks to Rs. 2 lakh

National Automated Clearing House System has been successfully used for making bulk transactions

Bharat Bill Payment System has helped in enhancing consumer convenience to pay bills across utilities and other segments and has been expanded to include all categories of billers who raise recurring bills (except prepaid recharges) as eligible participants, voluntarily

RBI has also developed a Payments Infrastructure Development Fund (PIDF) scheme to subsidise deployment of payment acceptance infrastructure in tier-3 to tier-6 centres

The RBI has created a regulatory framework around Peer-to-Peer (P2P) lending by recognising P2P lenders as Non-Banking Financial Companies (NBFCs), thus providing alternative credit access to the unbanked

IRDAI has undertaken various initiatives towards boosting the insurance penetration, such as permitting insurers to conduct video-based KYC, launching standardized insurance products and allowing insurers to offer rewards for low-risk behaviour

Government institutions such as the Health ministry and the NITI Aayog are also supporting the transformation in the insurance industry through the National Digital Health Mission (NDHM), the Digital Information Security in Healthcare Act (DISHA) and the National Health Stack

A world-class Fintech hub has been developed at the International Financial Services Centre (IFSC), GIFT City in Gandhinagar, Gujarat to further strengthen the vision of making India a global Fintech hub

Government has been making continuous effort to promote strong and sustainable industrial development in the country. Some of the key measures undertaken are listed below:

Startup India initiative was launched on 16th January, 2016 to build a strong eco-system for nurturing innovation and startups in the country that will drive sustainable economic growth and generate large scale employment opportunities. As on 26th November, 2021, more than 59000 startups have been recognized by DPIIT. The recognised startups have reported over 6.2 lakhs job created. To incentivize Startups, Fund of Funds for Startups Scheme (FFS), and Startup India Seed Fund Scheme (SISFS) schemes are being implemented by the DPIIT.

Government has put in place a liberal and transparent policy for attracting Foreign Direct Investment (FDI), wherein most of the sectors are open to FDI under the automatic route. Government reviews FDI policy on an ongoing basis and changes are made in the FDI policy regime, from time to time, to ensure that India remains increasingly attractive and investor-friendly investment destination. Measures taken by the Government on FDI Policy reforms have resulted in increased FDI inflows in the country, which year after year is setting up new records. India registered its highest ever annual FDI inflow of USD 81.97 billion (provisional figures) in the financial year 2020-21. These trends in India’s FDI are an endorsement of its status as a preferred investment destination amongst global investors.

Government is working to reduce compliance burden in order to spur investment in India. Government is also working to reduce compliance burden on citizen and business and the aim of this exercise is to simplify, decriminalize & remove redundant laws. In order to monitor large database of compliances across Central Ministries/Departments and States/UTs, Government has launched the Regulatory Compliance Portal on 1st January, 2021 (https://eodbrcp.dpiit.gov.in/). Based on data uploaded on Regulatory Compliance Portal, more than 25,000 compliances have been reduced by Central Ministries/Departments and States/UTs combined.

The Reserve Bank of India has come up with Regulatory Sandbox (RS) with the objective to foster responsible innovation in financial services, promote efficiency and bringing benefit to consumers. The RS allows the regulator, the innovators, the financial service providers (as potential deployers of the technology) and the customers (as final users) to conduct field tests to collect evidence on the benefits and risks of new financial innovations, while carefully monitoring and containing their risks. The RS is an important tool which enables more dynamic, evidence-based regulatory environments which learn from, and evolve with, emerging technologies.

The RBI has also created a Reserve Bank Innovation Hub (RBIH). The aim of Innovation Hub is to promote innovation across the financial sector by leveraging on technology and creating an environment which would facilitate and foster innovation, in collaboration with financial sector institutions, technology industry and academic institutions.

Production-Linked Incentive (PLI) Scheme for 14 key sectors (including Drones and Drone Components): Government has announced PLI scheme to enhance India’s manufacturing capabilities and exports. The schemes have been specifically designed to attract investments in sectors of core competency and cutting-edge technology; ensure efficiency and bring economies of size and scale in the manufacturing sector and make Indian manufacturers globally competitive so that they can integrate with global value chains. The PLI schemes are being implemented by the concerned Ministries/ Departments. There are targeted promotion activities being taken up by concerned Ministries/ Departments for identification of potential global and domestic investors by way of organizing investor networking events, investor roundtables, seminars and one-on-one meetings with potential investors.

PM GatiShaki launched on 13th October, 2021: It is a National Master Plan for multi-modal connectivity. Gati Shakti— a digital platform — to bring 16 Ministries including Railways and Roadways together for integrated planning and coordinated implementation of infrastructure connectivity projects.

Industrial Information System (IIS) – Government has developed an India Industrial Land Bank (earlier known as Industrial Information System) which provides a GIS-enabled database of industrial areas including clusters, parks, nodes, zones, etc. across the country to help investors identify their preferred location for investment. 4507 industrial parks/estates/SEZs in 5.15 lakh hectares have been mapped on India Industrial Land Bank (IILB) along with net land area availability.

Creating world class infrastructure through developing nodes across various Industrial Corridors. Industrial Corridor Programme is being developed in 04 phases (with 32 nodes) as part of the National Master Plan for providing multimodal connectivity infrastructure for creation of greenfield industrial smart cities with plug and play infrastructure in order to make India a manufacturing hub.

Investment Promotion activities are carried out by Government to attract more investments in the country. As a part of steps being taken to improve private interest and investment, ‘Make in India’ initiative was launched on September 25, 2014, to facilitate investment, foster innovation, building best in class infrastructure, and making India a hub for manufacturing, design, and innovation. Investment outreach is being done through Ministries, State Governments and Indian Missions abroad for enhancing international cooperation for promoting Domestic and Foreign Direct Investment (FDI) in the country.

In addition to ongoing schemes of various Departments and Ministries, Government has taken various other steps to boost domestic and foreign investments in India. These include reduction in Corporate Tax Rates, easing liquidity problems of NBFCs and Banks, improving Ease of Doing Business, FDI Policy reforms, Reduction in Compliance Burden, policy measures to boost domestic manufacturing through Public Procurement Orders, Phased Manufacturing Programme (PMP), Schemes for Production Linked Incentives (PLI) of various Ministries. To facilitate investments, measures such as India Industrial Land Bank (IILB), Industrial Park Rating System (IPRS), soft launch of the National Single Window System (NSWS), National Infrastructure Pipeline (NIP), National Monetisation Pipeline (NMP), etc, have also been put in place.

India registered its highest ever annual FDI inflow of US$ 81.97 billion (provisional figures) in the financial year 2020-21 despite the COVID related disruptions. In the last seven financial years (2014-21), India has received FDI inflow worth US$ 440.27 billion which is nearly 58 percent of the FDI reported in the last 21 years (US$ 763.83 billion). These trends in India’s FDI are an endorsement of the country’s status as a preferred investment destination amongst global investors.

The Minister of Commerce and Industry, Consumer Affairs, Food and Public Distribution and Textiles, Shri Piyush Goyal today urged political leadership, bureaucracy and industry leadership to focus their initiatives to reduce compliance burden, on principles of simplicity and timely delivery of services.

He was addressing the valedictory session of the ‘National Workshop on the next phase of reforms to reduce Compliance Burden’ in New Delhi today. It may be noted that more than 25,000 compliances have been reduced in the previous exercise implemented by the centre to reduce compliance burden and to promote Ease of Living and Ease of Doing Business.

Touching upon the infinite possibilities of technology, Shri Goyal said that technology must aid and abet initiatives to promote the Ease of Living and Ease of doing business and should not further complicate the system of compliances. He spoke of the need to develop indigenous solutions to problems that India faced.

The Minister asked policy makers to consider the wide disparity in income, literacy level and the gaps in infrastructure, especially connectivity, while planning the delivery of services, especially if technology is involved.

Speaking of the need to make monitoring mechanisms more robust, Shri Goyal said that monitoring of policies and programs must not become more cumbersome than the underlying problem that the initiatives were seeking to solve.

Shri Goyal opined that feedback from all stakeholders, especially users, had to be taken into account while designing compliance requirements and that ground realities must always be taken into consideration. He urged policymakers to use crowdsourcing to find out details of the compliances that were proving to be cumbersome and work on rationalizing them.

He spoke of the need to combine various services like the Digi locker and National Single Window System so that repetitive processes are rationalized, gaps are bridged and redundancies are eliminated when it comes to applying for approvals and permissions. He called for the creation of a single identification number for businesses and individuals by merging the several identification numbers that exist presently, such as Adhaar, PAN, TAN etc so that delivery of services becomes smoother and faster.

Speaking of the need to decriminalize Legal Metrology, the Minister urged industry participants to keep seeking reforms and improvements in processes and procedures. He also called for promotion of self- attestation, self- certification and self- regulation. He added that it is high time that compliance systems were built on trusting the integrity of the citizens.

Calling for big ticket reforms, the Minister said that the new structures must not shackle people. Underscoring the need to address information asymmetry among stakeholders, Shri Goyal called for, consolidation of the gains made so far in reducing compliance burden.

The day-long Workshop was divided into three parallel breakout sessions. The theme of the first was “Breaking Silos and Enhancing Synergies among Government Departments”. The second was based on the theme of “National Single Sign-on for Efficient Delivery of Citizen Services” while the third Breakout Session is themed ‘Effective Grievance Redressal’.

Speaking at the inauguration of the Workshop, Shri Anurag Jain, Secretary, Department for Promotion of Industry and Internal Trade (DPIIT) said that grievance redressal mechanisms must be humane and sensitive. He opined that in cases where grievances cannot be fully resolved due to rules and procedural aspects, the same must be conveyed to the complainant sensitively. Government departments could handle the genuine grievances with a human face, he added.

The Workshop witnessed wide participation from across Central Ministries and States/UTs. The ideas that took shape during the deliberations at the conference were presented to Shri Piyush Goyal and Cabinet Secretary, Shri Rajiv Gauba.

The Minister of Commerce and Industry, Consumer Affairs, Food and Public Distribution and Textiles, Shri Piyush Goyal today called for greater focus on nurturing entrepreneurship in the Tier 1 and Tier 2 cities of India. He was delivering the Keynote Address at the 3rd Meeting of National Startup Advisory Council virtually today.

It may be noted that 45% startups in India are from Tier 2 and 3 cities and 623 districts have at least 1 recognized startup. From 2018-21, almost 5.9L Jobs have been created by startups. In 2021 alone, almost 1.9L jobs have been created.

Department for Promotion of Industry and Internal Trade (DPIIT) had constituted the National Startup Advisory Council to advise the Government on measures needed to build a strong ecosystem for nurturing innovation and startups in the country to drive sustainable economic growth and generate large scale employment opportunities.

Besides the ex-officio members, the council has several non-official members, representing various stakeholders such as founders of successful startups, veterans who have grown and scaled companies in India, persons capable of representing interests of investors, incubators and accelerators into startups, representatives of associations of stakeholders of startups and representatives of industry associations.

The Minister said that 25th December, the birth anniversary of former Prime Minister Shri Atal Behari Vajpayee, is being celebrated as Good Governance Day in India. He expressed the hope that a robust Startup ecosystem would help formalize the economy and help in improving the Ease of Living and the Ease of Doing Business and in turn help promote the ideals of Good Governance. He observed that ‘Startup India’ movement had brought a ‘change in mindset’ from ‘can do’ to ‘will do’ and helped us move past traditional notions of entrepreneurship.

The Minister said that our startups turned COVID-19 crises into an opportunity and made 2021 the Year of unicorns with 79 Unicorns now thriving. Underscoring that India is now home to the 3rd largest startup ecosystem in the world, Shri Goyal said that he believed in the power of ideas. Simple solutions can make an extraordinary impact, he added.

Quoting Prime Minister Shri Narendra Modi, Shri Goyal said that the priority of the Government can be expressed in four words, “Minimum Government, Maximum Governance” and called for minimum Government interventions in the lives of citizens. He said that our vision is to build a New India committed to the economic progress and well-being of 135 crore Indians, especially those who have been left behind.

The Minister assured that the Government, as an enabler, is committed to develop a robust startup ecosystem by providing exceptional benefits such as 80% rebate in patent filing and 50% on trademark filing, relaxation in public procurement norms, Self-Certification under Labour and Environment Laws, Funds of Funds for startups of Rs. 10,000 Crore, Income Tax exemption for 3 out of 10 years, Seed Fund Scheme of Rs. 945 Cr and creating Open Network for Digital Commerce (ONDC), which will create new opportunities and remove some monopolistic tendencies in certain spheres.

Shri Goyal said that apart from mass jobs creation, our startups have the potential to catalyse India’s integration in Global Value Chains and increase our footprint in global markets. He urged successful entrepreneurs, especially unicorns to share their experiences with students and youth in order to inculcate startup culture and entrepreneurial spirit at grassroot levels, especially in regions like the North East of India. He asked academia, government and industry to work hand in hand to promote entrepreneurship at the grassroots level.

Urging the youth to take risks in entrepreneurship, the Minister said that you never know until you try, therefore, making mistakes should be normalised and failures should not be seen as the end of entrepreneurial journey. We must learn to celebrate failure too, he added.

Shri Goyal called upon startups to explore the unexplored areas like rural tourism in terms of agri-stays, hotels and homestays that would help create additional income for farmers. Shri Goyal opined that the youngsters of the nation must be encouraged to visit villages, experience rural life and come up with solutions to rural problems. He also asked successful startups to focus on rural economy and work on solutions such as drip irrigation, natural farming etc. to improve the lives of farmers.

Speaking of the need to augment Seed Capital, Shri Goyal said that we must encourage the flow of domestic capital in our startups. He added that there was a need to make ‘Startup India’ a symbol of Self Reliance and Self Confidence. The Minister called for a participative approach from all stakeholders to achieve such an ambitious target.

Six national programmes were presented to the Minister as part of the third National Startup Advisory Council meeting to strengthen the startup ecosystem in the country. The key interventions discussed were National Capacity Building Programme for Incubators, providing thrust to the startups engaged in manufacturing sector, empowering the larger pool of Family Offices and High Networth Individuals (HNIs) to invest in startups, accelerating Deep-tech Startups which would act as a catalyst in empowering pioneers, establishing an international platform and a gateway for Indian startups to go global, propelling participation of women in the startups and a holistic programme which aims at enabling global mentorship, market access, international opportunities and B2B connects.

The video conference was attended by several Startup leaders, investors, banks, senior government officials representing various ministries/departments and key stakeholders of the startup ecosystem.

The year 2020 witnessed turmoil due to COVID-19 pandemic which emerged as the biggest threat to economic growth. Indian economy has witnessed a sharp contraction of 24.4 per cent in Q1 and 7.3 per cent in Q2 of FY 2020-21.

To convert COVID pandemic related challenges into opportunity, a series of measures have been taken by the Government to improve the economic situation including inter-alia announcement of the Atmanirbhar package amounting to Rs.29.87 Lakh Crore. Targeted interventions were made to support the economy and livelihood. Moreover, the pace of structural reforms was expedited.

The major reforms undertaken under Atmanirbhar package include Credit guarantee for MSME loans, sectoral structural reforms, policy on strategic disinvestment of CPSEs, reforms in public procurement, setting up of Empowered Group of Secretaries and Project Development Cells for facilitating investment, reduction in compliance burden and single window system for clearances.

These measures, in addition to structural reforms taken up, have assisted the economy in its early revival. India, which was not producing N-95, PPE Kits, ventilators, etc. prior to Corona pandemic has started producing the same and even catering to world markets and became self-reliant. Government has started vaccination drive in January, 2021 and indigenously developed Covaxin vaccine in its fight against Covid pandemic. As on date more than 143 crore Covid doses have already been administered in India. This has not only saved the lives of people but also set momentum for early recovery of the economy.

Economy has started showing sign of recovery with GDP growth rebounding to 20.1 per cent in Q1 and 8.4 percent in Q2 of 2021-22. Several high frequency indicators like E-way bills, rail freight, port traffic, GST collections and power consumption have demonstrated a V-shaped recovery in the economy.

II. Industrial Performance

Industrial sector performance during 2020-21 declined considerably, by -8.4%, mainly due to nationwide closure of industries by the Government to limit the impact caused by Covid-19 pandemic on public health from March 2020 onwards. The Mining & Manufacturing sectors were majorly impacted as they declined by -7.8% & -9.6% respectively, whereas Electricity generation sector declined by -0.5%.

The cumulative Index of Industrial Production for April-October, 2020 declined by 17.3 percent. However, various measures undertaken by the Government including vaccination & the structural reforms and resilience of the Indian industry have helped early revival of the economy, which led to surge in IIP for same period in 2021 by 20.0 per cent. Similarly, the Mining, Manufacturing, and Electricity sector have registered growth of 20.4 percent, 21.2 percent, and 11.4 percent respectively during the same period.

III. Trends in Growth of Eight Core Industries

The Index of Eight Core Industries (ICI) measures the performance of eight core industries i.e. Coal, Crude Oil, Natural Gas, Petroleum Refinery Products, Fertilizers, Steel, Cement and Electricity. The industries included in the ICI comprise 40.27 per cent weight in the Index of Industrial Production (IIP).

During 2020-21, the ICI growth rate was -6.4 per cent compared to average growth rate of 3.0 per cent during last 3 years i.e. 2017-18 to 2019-20. The rate of growth has been robust during the current financial year (April to October, 2021-22) i.e. 15.1%. Out of Eight Core sectors, six of them have shown double digit growth with Cement and Steel sectors leading the pack with growth rates of 33.6% & 28.6% respectively. Whereas, Crude Oil & Fertilizers sector growth remain muted in the same period i.e. (April to October, 2021-22). These shows the revival of core industries.

IV. DPIIT has been spearheading a number of initiatives in this area, ‘To Make in India for the World’. The key steps taken in this regard are as follows:

1. Production Linked Incentive Scheme:

Keeping in view India’s vision of becoming ‘Atmanirbhar’ and to enhance India’s Manufacturing capabilities and Exports, an outlay of INR 1.97 lakh crore (US$ 26 billion) has been announced in Union Budget 2021-22 for PLI schemes for 14 key sectors of manufacturing starting from fiscal year (FY) 2021-22. These 14 sectors are namely: (i) Automobiles and Auto Components, (ii) Pharmaceuticals Drugs, (iii) Specialty Steel, (iv) Telecom & Networking Products, (v) Electronic/Technology Products, (vi) White Goods (ACs and LED Lights), (vii) Food Products, (viii) Textile Products: MMF segment and technical textiles, (ix) High efficiency solar PV modules, and (x) Advanced Chemistry Cell (ACC) Battery (xi) Medical devices (xii) Large scale electronics manufacturing including mobile phones (xiii) Critical Key Starting materials /Drug intermediaries and API; and (xiv) Drones and Drone Components.

The guidelines for all PLI schemes have already been issued and applications have also been received under a majority of the schemes.

While DPIIT is doing the overall coordination for PLI Schemes, it is the nodal Department for PLI scheme for White Goods (Air Conditioners and LED lights), which has an outlay of an outlay of Rs. 6238 Crore. The Scheme Guidelines was published on 4th June 2021. 42 applicants with committed investment of Rs 4,614 crore have been provisionally selected as beneficiaries under this PLI scheme. The selected applicants include 26 for Air Conditioner manufacturing with committed investments of Rs. 3,898 crore and 16 for LED Lights manufacturing with committed investments of Rs. 716 crore.

2. PM GatiShakti National Master Plan (NMP):

The Prime Minister launched Gati Shakti, a National Master Plan for Infrastructure Development, on 13th October, 2021. Gati Shakti is a digital platform which will bring 16 Ministries including Railways and Roadways together for integrated planning and coordinated implementation of infrastructure connectivity projects.

PM Gati Shakti aims to address the past issues through institutionalizing holistic planning for stakeholders for major infrastructure projects. Instead of planning & designing separately in silos, the projects will be designed and executed with a common vision. It will incorporate the infrastructure schemes of various Ministries and State Governments like Bharatmala, Sagarmala, inland waterways, dry/land ports, UDAN etc. Economic Zones like textile clusters, pharmaceutical clusters, defence corridors, electronic parks, industrial corridors, fishing clusters, agri zones will be covered to improve connectivity & make Indian businesses more competitive. It will also leverage technology extensively including spatial planning tools with ISRO imagery developed by BiSAG-N (Bhaskaracharya National Institute for Space Applications and Geoinformatics).

3. Start-up India Programme:

· The Start-up India initiative was launched by the Prime Minister on 16th January 2016 as a flagship initiative of Government of India. The initiative was intended to build a stronger ecosystem for nurturing India’s start-up culture that would further drive our economic growth, support entrepreneurship, and enable large-scale employment opportunities. With over 60,000 recognized start-ups, India has transformed into the third largest start-up ecosystemsupplementing employability as well as enhancing our self-reliance. Start-up India’s role has been vital in nurturing entrepreneurship beyond Tier 1 cities. The regional growth through the efforts of States and Union Territories (UTs) has created a national ecosystem to thrust our economic goals. While 55% of the recognised start-ups are from Tier-1 cities and 45% of the start-ups are from Tier-2 and Tier-3 cities respectively, 45% of start-ups are represented by women entrepreneurs. This shows the roots of startups have grown deep in the country.

· Recognized start-ups have made deep inroads into Tier-II and Tier-III cities. Startups are now spread across 633 districts with a total of 30 States and UTs with Startup Policies in place. DPIIT recognised start-ups have reported creation of close to 2 lakh jobs in 2021, the highest in four years. Cumulatively, more than 6.5 lakhs jobs have been generated since the launch of Start-up India initiative.

· Under the Fund of Funds for Start-ups (FFS), Rs. 6,495 crore has been committed to 80 Alternative Investment Funds (AIFs) and Rs. 8,085 crore have been invested by supported AIFs in 540 startups. For Start-up India Seed Fund Scheme (SISFS), 58 incubators have been selected and Rs. 232.75 crore have been approved as grant under the Scheme

4. Investment Promotion

Investment Clearance Cell:

While presenting Budget 2020-21, Union Finance Minister announced plans to set up an Investment Clearance Cell (ICC) that will provide “end to end” facilitation and support to investors, including pre-investment advisory, provide information related to land banks and facilitate clearances at Centre and State level. The cell was proposed to operate through an online digital portal.

Subsequently, DPIIT along with Invest India initiated the process of developing the portal as a National Single Window System (NSWS). Envisioned as a one-stop for taking all the regulatory approvals and services in the country, NSWS [www.nsws.gov.in], was soft-launched on 22nd September 2021 by the Commerce & Industries Minister, Shri Piyush Goyal.

This national portal integrates the existing clearance systems of the various Ministries/ Departments of Govt. of India and State Governments without disruption to the existing IT portals of Ministries/ Departments. Approvals of 18 Ministries/ Departments and 10 States Single Window Systems have been on-boarded in Phase I. Complete on-boarding of 32 Central Departments and 14 States would be in next phases, all remaining States will be on-boarded in a phase manner.

Ease of Doing Business:

DPIIT is continuously making efforts to improve ease of doing business in the country through the three major initiatives being pursued, focusing on – WorldBank’s Ease of Doing Business, State & District Reform Action Plan and systematic approach to reduce regulatorycompliance burden on businesses. As a result, India’s rank as per World Bank’s EoDB Report improved from 142 in 2014 to 63 in 2020.

In order to monitor large database of compliances across Central Ministries/Departments and States/UTs, DPIIT has launched the Regulatory Compliance Portal on 1st January, 2021 (https://eodbrcp.dpiit.gov.in/). Based on data uploaded on Regulatory Compliance Portal, more than 25,000 compliances have been reduced by Central Ministries/Departments and States/UTs combined.

DPIIT had identified 194 compliances for reductions pertaining to PESO, Boiler, IPR, NEIDS, Industrial Licensing. Out of these, 134 compliances have been ‘Reduced”, 31 are ‘under review’ and 29 have been ‘Retained’. Types of compliance reduced are: (i) Certificate, License and Permission (ii) Filings (iii) Inspection, Examination and Audits (iv) Registers and Records, (v) Display Requirements, (vi) Redundancy (vii) Decriminalization (viii) Technology and (ix) others.

Project Development Cells:

Project Development Cells (PDCs) have been set up in 29 Ministries/Departments to fast track investment in coordination between the Central Government and State Governments and thereby enhance the pipeline of investible projects in India and in turn increase domestic investment and FDI inflows.

India Industrial Land Bank (IILB):

The IILB is a GIS based portal developed by DPIIT as a one stop repository of all industrial infrastructure related information – connectivity, infra, natural resources & terrain, plot level information on vacant plots, line of activity and contact details. Currently, the IILB has approximately 4500 industrial parks mapped across an area of 5.11 lakh hectare of land serving as a decision support system for investors scouting for land remotely. The system has been integrated with industry-based GIS systems of 24 States/UTs namely Andhra Pradesh, Assam, Bihar, Chhattisgarh, Dadar & Nagar Haveli and Daman & Diu, Goa, Gujarat, Haryana, Himachal Pradesh, Jharkhand, Karnataka, Kerala, Maharashtra, Madhya Pradesh, Odisha, Punjab, Puducherry, Sikkim, Tamil Nadu, Tripura, Telangana, Uttarakhand, UP and have details of 2113 GIS enabled parks on a real-time basis. A mobile application (wherein login is not required) of IILB is also available on Android and iOS stores for the ease of investor.

6. Foreign Direct Investment

FDI policy provisions have been progressively liberalized and simplified across various sectors in the recent past to make India an attractive investment destination. Measures taken by the Government on FDI Policy reforms have resulted in increased FDI inflows in the country, which year after year is setting up new records. FDI inflows in India stood at US $ 45.15 billion in 2014-2015 and have continuously increased since then. FDI inflows increased to US $ 55.56 billion in 2015-2016, US $ 60.22 billion in 2016-2017, US $ 60.97 billion in 2017-2018, US $ 62.00 billion in the year 2018-19, US$ 74.39 billion in the year 2019-20 and India registered its highest ever annual FDI inflow of US$ 81.97 billion (provisional figures) in the financial year 2020-21. These trends in India’s FDI are an endorsement of its status as a preferred investment destination amongst global investors.

FDI policy reforms during 2021:

Insurance Sector: Government issued Press Note 2(2021) dated 14.06.2021 to raise the permissible FDI limit from 49% to 74% in Insurance Companies under the automatic route and allow foreign ownership and control with safeguards. This will facilitate an increased flow of long-term capital, global technology, processes and international best practices, which will support the growth of India’s insurance sector.

Petroleum & Natural Gas sector: Press Note 3 (2021) dated 29.07.2021 has been issued to permit foreign investment up to 100% under the automatic route in cases where the Government has accorded an ‘in-principle’ approval for strategic disinvestment of a Public Sector Undertaking (PSU) engaged in the Petroleum and Natural Gas Sector.

Telecom sector: Press Note 4 (2021) dated 06.10.2021 has been issued to permit foreign investment up to 100% under automatic route in Telecom services sector.

7. Intellectual Property Rights (IPR): Framework to attract foreign investors, disseminate creativity and encourage local innovators

An effective IPR framework is indispensable to attract foreign investors, disseminate creativity and encourage local innovators to invest in their own ideas. In this context, DPIIT is committed towards strengthening of the IP ecosystem in India. Major initiatives and steps taken during 2021 in this regard are given below:

Design (Amendment) Rules, 2021 notified in the Gazette of India on 25.01.2021 incentivize start-ups and small entities to seek protection of their designs and promote design filings, fees have been reduced on similar lines as under Patent and Trademark Rules.

Copyright (Amendment) Rules, 2021 notified on 30.03.2021, with the objective of bringing the existing rules in parity with other relevant legislations. It introduces a mandatory annual transparency report to be issued by Copyright Societies. It aims to ensure smooth and flawless compliance in the light of the technological advancement in digital era by adopting electronic means as primary mode of communication and working in the Copyright Office.

Patent (Amendment) Rules, 2021: Patent fees for educational institutions have been reduced by 80 percent by way of the Patents (Amendment) Rules, 2021, which came into effect on 21st September 2021. The amendment will provide the same level of support to educational institutions as MSMEs and start-ups and further ensure greater participation of the education institutions in IP ecosystem.

Since the adoption of the National IPR Policy, IP filing in India has witnessed a considerable amount of increase in filing. Despite the adverse Covid situation in India, no negative impact has been seen in the filing of the IPs. Further, the filing of application of Trademark and GI have drastically increased over the years.

8. One District One Product (ODOP)

Government of India is working on a transformational initiative to foster balanced regional development across all districts of the country. This is called the One District One Product (ODOP) initiative, with the objective of identifying and promoting the production of unique products in each district in India that can be globally marketed. This will help realise the true potential of a district, fueling economic growth, generating employment and rural entrepreneurship. ODOP initiative is operationally merged with the ‘Districts as Export Hub’ initiative being implemented by DGFT, Department of Commerce with DPIIT as a major stakeholder to synergize the work undertaken by DGFT. The major activities that are being facilitated by DPIIT with Invest India under ODOP initiative are manufacturing, marketing, branding, internal trade and e-commerce.

Ongoing expansion exercise entailing expansion of list from Phase-1 that consisted of 106 products from 103 districts to current Phase-2 that would consist of 739+ products covering 739 districts. Considerable success has been achieved for boosting exports under ODOP initiative.

11. Swachhata Campaign

During this special campaign, 49,686 files have been reviewed in DPIIT and its sub-organizations. Out of the reviewed files, 49,449 files have been weeded out. Due to weeding of files, 2222 sq ft area has been vacated/freed in DPIIT and its sub organizations. Due to disposal of redundant/obsolete items, 3277 sq feet of area has been vacated, which has improved cleanliness and hygiene conditions. Besides, revenue of Rs 5,60,000 has been generated.

The Department achieved 100% target in respect of public grievances by disposing of all 31 public grievances and 3 public grievances appeals. Further, out of 48 VIP reference, 29 cases have been disposed off. The Department had identified 194 rules/regulation for simplification under “Ease of Doing Business”. Out of these, 134 rules have been simplified.

Digitization of old files/records: Even before the special campaign, as per directions of the CIM digitization of old files/ records was undertaken on a priority basis. During the period, scanning/digitization of 12,387 files containing 19,53,666 pages have been completed and all the scanned files have been migrated to e-office for future reference.

Increasing Efficiency decision making in the Government on direction of Cabinet Secretary and advice of DARPG, with the approval of the Competent Authority,DPIIT has revised the Channel of Submission & Level of disposal, for increasing efficiency in decision making and reducing the level up to 4 (maximum). This will speed up the disposal of cases and improve decision making.

Review by CIM: CIM has reviewed the special drive continuously during the campaign period. After completion of the Special Drive on 31.10.2021, CIM is reviewing progress of the Cleanliness Campaign on weekly basis. CIM is also undertaking frequent rounds of Udyog Bhawan to review the cleanliness of the premises.

12. Events organised by DPIIT during India’s presidency of BRICS in 2021:

The 13th BRICS Summit was held under India’s Chairship in 2021. It was the third time that India hosted the BRICS Summit after 2012 and 2016. The theme for India’s Chairship was ‘BRICS @ 15: Intra-BRICS Cooperation for Continuity, Consolidation and Consensus’. During India’s presidency of BRICS, 4 events were organized by DPIIT on industry related issues namely- Industry Ministers Meeting, PartNIRMeeting (Partnership on New Industrial Revolution) to promote investment, industrialization, innovation, inclusiveness and digitization, 13th HIPO (Head of Intellectual Property Offices) meeting and Round Table of an interaction among the Trade and Investment agencies of BRICS.

13 DPIIT has organised following events under Azadi ka Amrit Mahotsav (AKAM):

Ministry of Commerce and Industry was allocated the week from 20.09.2021 to 26.09.2021. Accordingly, DPIIT has held various events during the ‘Udyog Saptah’ i.e. from 20th -26th September, 2021which was widely published by different platforms. Some of the events organized by DPIIT were:

Press Briefing addressed by Additional Secretary, DPIIT held on 21st September, 2021 on measures to ensure industrial safety in petroleum and explosives Sector as well as reducing cost of doing business and creating an enabling ecosystem for domestic as well as international investors.

Soft launch of National Single Window System on 22nd September, 2021 by Shri Piyush Goyal, for providing end-to-end facilitation, support, including pre-investment advisory, information related to land banks and facilitating clearances at Central and State levels and bring Transparency, Accountability & Responsiveness in the ecosystem and all information will be available on a single dashboard.

Startup India had coordinated with various States/UTs to organize/participate in startup events consisting of diverse programs, launch of key initiatives, inaugural of startup summits, and launch of startup policies, etc during 21.09.2021 to 26.09.2021 with the aim to foster entrepreneurship on the ground.

Northeast Business Roundtable held on 23th September, 2021 in the presence of Minister of State Shri Som Parkash to showcase the business and investment opportunities and deliberations on the reforms implemented in the region.

National Workshop on Reducing Compliance Burden held on 28th September, 2021 in the presence of Hon’ble Union Minister Shri Piyush Goyal, Minister of State Shri Som Parkash and Smt. Anupriya Patel. More than 25,000 compliances have been reduced by Union Ministries, States & UTs so far.

Industrial Park Rating System Report 2.0 was launched by MoS (Commerce and Industry), Shri Som Parkash on 5th October, 2021.

PM Gati Shaki launched by Prime Minister Shri Narendra Modi on 13th October, 2021 for multi-modal connectivity.

Good Governance Week during 20-25th December, 2021: DPIIT has organized a National Workshop on the “Next Phase of Reforms for Reducing Compliance Burden” on 22nd December, 2021 to realize the nation’s goals of improving “Ease of living” and “Ease of doing business”. Hon’ble Commerce and Industry Minister Shri Piyush Goyal addressed the workshop.

DPIIT will also be organising Innovation Ecosystem week (10th – 16th January, 2022): In the proposed event DPIIT will showcase efforts taken up for promotion of Unicorns and Start-ups. Event will be led by M/o Education.

You must be logged in to post a comment.