Banks play an important role in financial stability and the economy of a country.

It is a financial institution that accepts deposits from the public and creates a demand deposit while simultaneously making loans.

Credit creation is one of the most important functions performed by commercial banks. It separates a bank from other financial institutions . In simple terms credit creation is the expansion of deposits. A bank expands the demand deposit into multiple cash reserves as demand deposits are the principal medium of exchange.

In words of Newly ” Credit Creation refers to the power of commercial bank to expand secondary deposits either through the process of making loans or through investment in securities “

Credit Creation is a situation in which banks give more loans to consumers and businesses with the result that the amount of money in circulation increases . In other words , it refers to the unique power of banks to multiply loans and advances and hence create credit on the basis of the primary deposit of the account holder .

According to G.N Halm ,

“The creation of derivative deposits is identical with what is commonly called the Creation of Credit .”

__________________________________________

Arguments Regarding Credit Creation .

There have been two views on the Credit Creation by bank by two economists

Hartley Withers

Walter Leaf .

According to Withers , banks can create credit by opening a deposit , every time they advance a loan . This is because every time a loan is sanctioned , payment is made through cheques . As long as a loan is due , a deposit of the amount remains outstanding in the books of the bank . This every loan creates a deposit .

Walter Leaf did not agree with this view . According to them, banks cannot create money out of thin air . They can lend only what they have in cash . Therefore , they cannot and do not create money .

The given argument was related to single bank and hence ,as pointed out by Prof Samuelson ,

“The banking system as a whole can do what each small bank cannot do : it can expand its loan and investments many times the new reserves of cash created for it , even though each small bank is lending out only a fraction of its deposits .”

Thus , banks are able to create credit or deposits by keeping a small cash in reserves and lending the remaining amount .

Basis of Credit Creation

Demand deposits are an important constituent of money supply and the expansion of demand deposits means the expansion of money supply . The entire structure of banking is based on credit . Credit basically means getting the purchasing power now and providing to pay at some time in the future .

Bank deposits form the basis of credit creation.

Bank deposits can be divided into two types :-

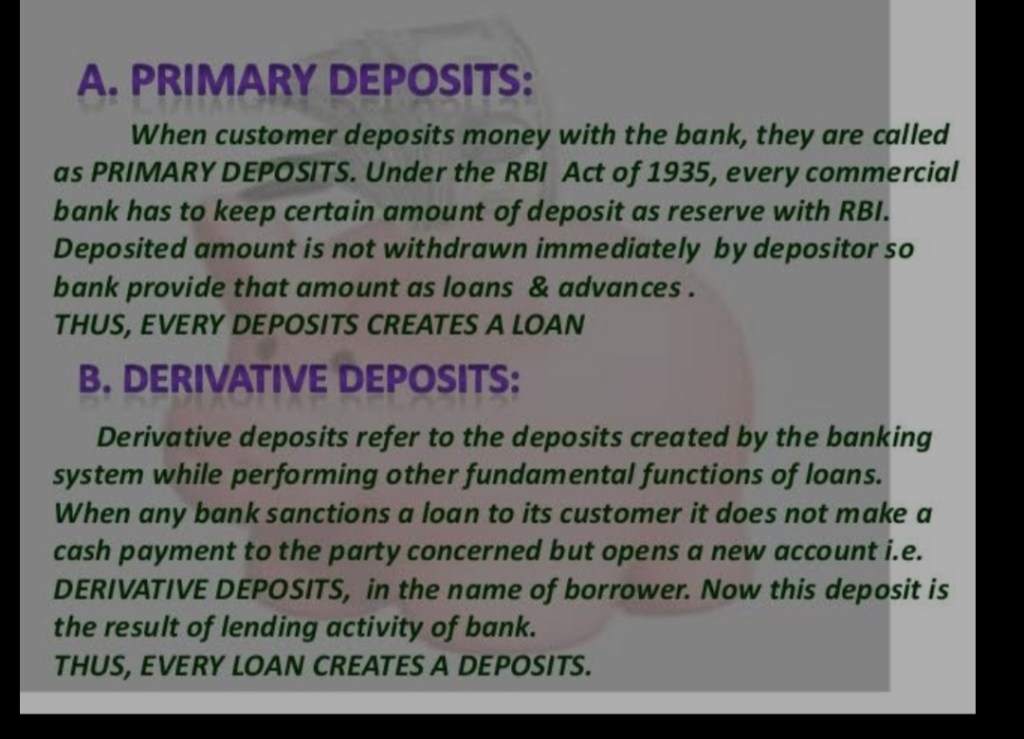

• Primary Deposits :- A bank accepts cash from the customer and opens a deposit in his name . This is a primary deposit . These deposits simply convert currency money into deposit money . These deposits form the basis for the creation of credit. These deposit creates a loan .

• Secondary or Derivative Deposit :- A bank grants loans and advances instead of giving cash to the borrower , opens a deposit account in his name . This is the secondary or derivative deposit . Every loan creates a deposit . The creation of a derivative deposit means the creation of credit .

Banks can expand their demand deposits as a multiple of their cash reserves because demand deposits serve as the principal medium of exchange .

Aspects of Credit Creation

The two important aspects of credit creation are :-

Liquidity :- The bank must pay cash to its depositor when they exercise their right to demand cash against their deposit .

Profitability :- Banks are profit – driven enterprises . Therefore a bank must grant loans in a manner which earns higher interest than what it pays on its deposit .

Assumptions :-

The bank’s credit creation is based on the assumption that during any time interval only a fraction of its customers genuinely need cash . The bank also assumes that all its customers would not turn up demanding cash against their deposit at the same time .

Concepts of Credit Creation.

• Bank deposit :- Bank deposits are the basis of credit creation . Bank deposits constituent of primary deposit and secondary deposit .

• Bank as a Business institution :- Bank is a business institution which tries to maximize profit through loans and advances from deposits.

• Borrowing rate :- The rate at which commercial banks accept deposits is known as the borrowing rate.

• Lending rate :– The rate at which the commercial banks lend money to the customers is known as the lending rate.

• Spread :- The difference between the lending rate and the borrowing rate is known as the spread.

Spread = Lending rate – Borrowing rate.

• Concept of Cash Reserve Ratio :- It is legally compulsory for the bank to keep a certain minimum fraction of the deposit as a reserve. This is known as Cash Reserve Ratio (CRR) or Legal Reserve Ratio (LRR).

Banks only keep a fraction of deposits as cash reserves because all depositors do not approach the bank for withdrawal of money at the same time.

There is a constant flow of new deposits into the banks.

• Excess Reserves :- The reserves over and above the cash reserves are the excess Reserves used for loans and credit creation .

• Concept of Credit Multiplier :- The credit multiplier or deposit multiplier measures the amount of money that the banks are able to create in the form of deposits with every unit of money that it keeps as a reserve.

It is calculate as,

Money Multiplier (MM or K) = 1/ CRR times

Given a certain amount of cash , a bank can create credit multiple times . In the process of multiple credit creation , the total amount of derivation deposits that a bank creates is a multiple of initial cash .

Mathematics representation of Credit Creation

Formula for Credit Creation :-

Total Credit Creation =

Cash deposit ( initial deposit ) X Credit Multiplier Coefficient .

where , credit multiplier coefficient = 1/ r

r = Cash Reserve Ratio .

Extending the above formula,

Total deposit = Cash Deposit + Credit Deposit .

Let ,

Cash Deposit = ∆ D

Cash Reserve Ratio = r

Total deposit = ∆ M

Derivation :-

∆ M = ∆ D + (1- r) ∆ D + ( 1- r ) ² ∆ D +( 1- r )³ ∆D +……….( 1-r ) ^ n-1 ∆ D .

– (i)

By multiplying both side by (1-r) in equation (i)

( 1- r) ∆M = (1-r ) ∆ D +(1-r)² ∆D + (1-r)³ ∆D ………..(1-r)^ n ∆ D.

-( ii )

Subtracting equation i and ii we get ,

( 1-r) ∆ M – ∆M = – ∆ D + ( 1- r) ^n ∆ D.

∆ M ( 1-r-1 ) = – ∆ D [ 1- ( 1-r) ^n ]

If n = ~

Then , (1-r) ^n =0

So ,

r ∆M = ∆ D ( 1-0 )

r∆ M = ∆ D

∆ M = 1/r × ∆ D .

Hence ,proved ,

Total deposit = Cash deposit × Credit Multiplier Coefficient.

Process of Credit Creation

There are two ways of analyzing the credit creation process:

• Single bank Credit creation system.

• Multiple bank Credit creation system.

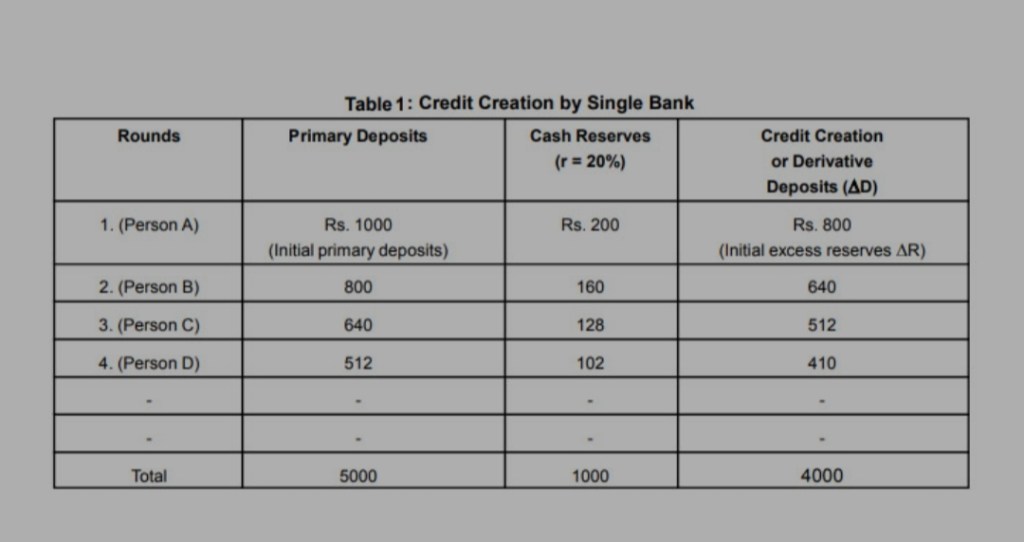

Single Bank Credit Creation:-.

In this system, one bank operates all the cash deposits and cheques.

Explanation with hypothetical example :-.

Assumption :-

Bank receives a cash deposit from person A , of Rs. 1000.

The bank requires a CRR of 20 percent.

The remaining money is lent to another person B , C , D …and so on.

Explanation :-

Person A deposits 1,000 rupees with the bank, then the bank keeps only 200 rupees in the cash reserve and lends the remaining 800 to another person B.

They open a credit account in the borrower’s name for the same.

Similarly, the bank keeps 20 percent of Rs. 800 (i.e. Rs. 160) and advances the remaining Rs. 640 to person C.

Further, the bank keeps 20 percent of Rs. 640 (i.e. Rs. 128) and advances the remaining Rs. 512 to person D.

This process continues until the initial primary deposit of Rs. 1,000 and the initial additional reserves of Rs. 800 lead to additional or derivative deposits of Rs. 4,000 (800+640+512+….).

Adding the initial deposits, we get total deposits of Rs. 5,000.

In this case, the credit multiplier is 5 (reciprocal of the CRR) and the credit creation is five times the initial excess reserves of Rs. 800.

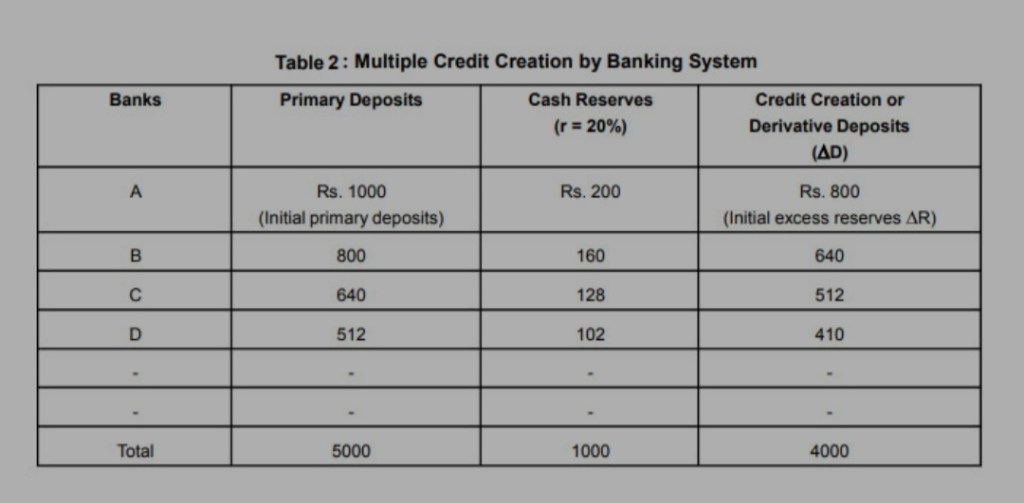

Multiple Credit Creation by the Banking System

In multiple credit creation by a bank , deposit of one bank is the gain of deposit for some other bank.

This transfer of cash within the banking system creates primary deposits and increases the possibility for further creation of derivative deposits

Multiple banking system includes the following assumptions :-

• There are. many banks , say A,B, C ,.etc.

• First Bank has a cash deposit of Rs. 1000.

• The bank requires a CRR of 20 percent.

• The remaining money is lent to another bank B , C , D …and so on.

The initial deposit of Rs. 1,000 with bank A leads to a creation of total deposits of Rs. 5,000.

Limitations :-

Commercial banks have limited power in the creation of credit . The following are the limitations on the power of commercial banks to create credit.

•The credit creation power of banks depends upon the amount of cash they possess .

• An important factor that limits the power of banks to create credit is the availability of adequate securities .

• The banking habits of the people also govern the power of credit creation on the part of banks .

• The minimum legal reserve ratio of cash deposits fixed by the central bank is an important factor which determines the power of banks to create credit.

• The process of Credit Creation is based on the assumption that banks stick to the required reserve ratio by the Central Bank .

• If there are leakages in the credit creation steam of the Banking system , credit expansion will not reach the required level.

• The power of credit creation is further limited by the behaviour of the other banks .

___________________________________________

Referral links :-Cash Reserve Ratio, Credit Multiplier.

You must be logged in to post a comment.