Cost refers to the expenditure incurred by a producer on factor as well as non-factor inputs for given output of a commodity. It can be categorized into explicit ( Opportunity cost of hiring inputs from the market, measured in cash payments that firm make to others.) and implicit costs. ( Opportunity cost of using self-owned inputs, measured in terms of imputed costs of self owned resources.). It is also termed as selling ( expenditure caused due to promote sale of good.) and production costs ( expenditure on inputs to produce an output.)

Fixed costs are costs related to use of fixed factor of production in short period like, machines, license fee, land expenditure, etc. They do not change with change in output. Variable costs on other hand refer to expenditure by producer on use of variable factors of production like, costs of raw material, wages of workers, wear and tear expense, etc. They increase with increase in output and vice-versa. Graphical representation is given by-

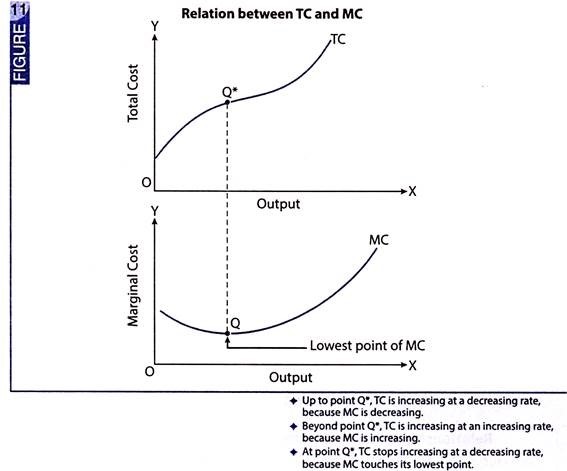

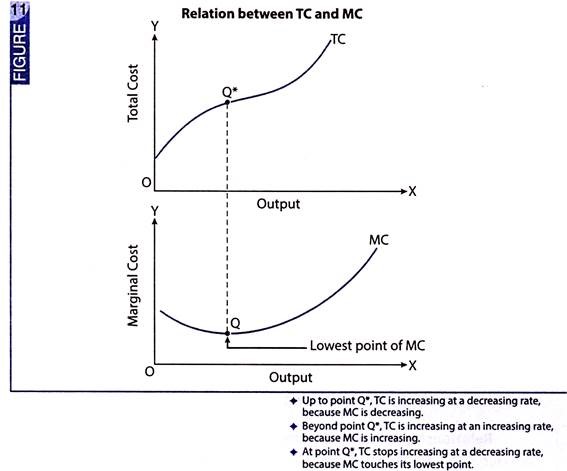

Total cost is defined as sum of variable and fixed costs. Since total variable cost tends to increase at diminishing rate initially, meaning that less and less of additional cost is incurred in every additional output. This happens due to increasing return to a factor and eventually TVC increases at an increasing rate.

Relationship between TVC and MC:

i) Marginal cost is estimated as the difference between total costs of two successive units of output. Thus,

MCn = TCn – TCn-1

(ii) When MC is diminishing, TC increases at a diminishing rate.

(iii) When MC is rising, TC increases at an increasing rate.

(iv) When MC reaches its lowest point (point Q in Fig. 11), TC stops increasing at a decreasing rate (point Q* in Fig. 11).

Medical and Engineering are most sought after courses after 12th Science in India.Parents and the society are the major contributors to this mentality in our country. Thousands of students flock examination centers to write prestigious NEET/JEE irrespective of whether they are interested or not.

Does this mean these are the only options available to students choosing the Science Stream?The Answer is NO.In Today’s advanced world there are plethora of career and course options for students to pursue and achieve success.In this blog we look at some of the prominent and promising non conventional career options in science stream.Lets get started!

Psychologists study the complex ways that people think, behave, feel, communicate, and perceive the world around them. Some psychologists focus on clinical work with patients, while others devote themselves to researching the nuances of psychological behavior; in any case, psychology is a vast discipline, with numerous career options to choose from. Students who complete graduate-level psychology degrees have great job opportunities. An MSc degree may lead to jobs as research and clinical assistants, while a doctorate is a necessity for those who wants to work with patients in a clinical setting and also to move into a research or an academic position. Many degree programs allow students to focus on a specialty area, including child development, abnormal psychology, counseling, social psychology, and cognition.The opportunities in research under this field are limitless.Psychology is a hot subject in developed nations like The United States and The United Kingdom where this course is sought after and valued.

2)FORENSIC SCIENCE

Forensic science is the application of scientific knowledge and methodology to criminal investigations and legal problems. Forensic Science is a multidisciplinary subject, it encompasses various fields of science such as chemistry, biology, physics, geology, psychology, social science, engineering, etc.Forensic science is used every around the world to protect public and society, to enforce criminal laws and regulations and to resolve civil problems.Various universities in India offer certificate, bachelor and master courses in Forensic Science. After the master degree is successfully completed , then the student can even go for a Doctoral Degree course in Forensic Sciences.Jobs are offered in government as well as private sectors.

3)Agricultural SCIENCES

Agriculture as a field is not just about the traditional aspects related to farming and irrigation. The focus is now shifted to various other dimensions like Horticulture, Poultry Farming, Pisciculture, Dairy Farming, Agricultural Biotechnology,Agronomy etc. Agriculture is also being commercialized as proper attention is being paid to the marketing, distribution, and packaging of its output. It’s possible to pursue a postgraduate degree programme in agriculture related subject which will broaden the scope such as specializing in agronomy, soil sciences, horticulture, plant breeding and genetics, entomology, plant pathology, animal sciences, plant biochemistry, agriculture economics, biotechnology etc. Masters in various above listed Agriculture programs is a 2-year course.This course can be taken up by a candidate who holds a BSc degree in agriculture/ horticulture/ forestry from a recognized university with some qualifying marks.Job opportunities are available both in Government as well as Private Sectors.

4)Aviation industry

The aviation sector is one of the most attractive and best-paid sectors in the economy. In India, The civil aviation industry is a larges domestic market in the economy.The commercial pilot is one the most glamorous and most rewarding job in the Aviation industry. Apart from the theoretical knowledge, a candidate must have practical knowledge to become a commercial pilot. A Commercial pilot must train to get a Commercial Pilot license in order to secure a job in the aviation sector. A commercial pilot or Ferry Pilot will have many chances of getting placed in both Governments and Private Airlines & chattered flights.The interested candidate must be fluent in English,medically fit and must have learnt Maths and Physics in High School.

5)Visual communication

Visual Communication is a combination of illustration and graphic design from a marketing perspective with great emphasis on screen-based workmanship.It involves digital marketing and business identity design , logos, animation, photography, web design, illustration, packaging design, art direction, and most degrees will also have a theory dissertation. It contains all the information to help one become a Graphic Designer, with a scope that allows to to specialize with more flexibility than a degree in design.In short, visual communication is an amazing field with unlimited growth potential. They get hefty pay.Further, with experience, your earnings are bound to increase.

These are just a few options listed from a sea of options.The aim of this blog is to make readers aware that the bucks do not stop at Engineering or Medicine.There are umpty number of career options to choose from and succeed.Everyone can not find happiness within the conventional options imposed by the society.Times are changing and so should our mentality.Students should be encouraged to follow their passion and pursue courses they want.Sky is the limit!

Do like the blog,if you all found it to be useful!

THE COVID-19 HAS LET US DO WHAT WE NEVER USED TO DO AND STILL WE ARE NOT ABLE TO IT COMPLETELY AND THAT IS NOTHING BUT SOCIAL DISTANCING . SOME OF US HAVE NEVER MET OUR FAMILY MEMBERS , OUR CLOSE FRIENDS AND WE ARE DYING TO MEET THEM , MUTUAL FEELING IT IS !.

WE ARE GOING THROUGH ECONOMIC DOWNTURN AND ALL THE BUSINESSES ARE URGING TOWARDS LOSSES . MARKETRES ARE SAD DUE TO LESS PROFIT AND HAPPY DUE TO MORE CONSUMPTION DEMAND .

AS THERE IS A NEED OF SOCIAL DISTANCING , EVERYONE IS FEARING TO SHOP THROUGH OFFLINE MODE , THOUGH , MAKING PURCHASES THROUGH ONLINE MODE IS TOO DANGEROUS , YOU DON’T KNOW HOW MANY HANDS HAVE TOUCHED IT BUT THEY TAKE CARE OF EVERY PRECAUTIONS THEY ARE TAKING AND WE ALL SHOULD ALSO SANITISE THE GIFTS DELVERED.

MARKETERS AND THE SERVICE INDUSTRIES ARE THE HAPPIEST , ONLINE STORES CATERING BASIC NECESSITIES ARE ON TOP AS IT IS HELPING IN SOCIAL DISTANCING .

BOOMERS , THE GENERATION FROM 1946 TO 1964 ARE PREFERING TO SHOP THE PRODUCTS ONLINE FROM THE ONLIINE STORES AND HAS RAISED THE CONSUMPTION DEMAND , FUND’S ROLLING HAS INCREASED IN THE ECONOMY .

THE GIANTS LIKE ZOMATO FOR FOOD , AMAZON FOR ALL THE COSUMERS PRODUCTS , FLIPKART , MYNTRA FOR YOUR WEARS , WHY I HAVE CALLED THEM AS GAINTS BECAUSE THEY ARE DELIVERING BEST SERVICES TO THE PEOPLE . SURVEY HAS SHOWED THAT THE SALES HAS INCREASED THROUGH ONLINE MODE COMPARING PRE LOCKDOWN . AMAZON IS THE BIGGEST GIANT AMONG ALL . I THINK NOW MARKETERS SHOULD FOCUS MORE ON SOCIAL MEDIA MARKETING TO GAHTER MORE CUSTOMERS , THEY WERE DOING IT , BUT NOW IT HAS BECOME NECESSITY. MORE FOCUS SHOULD BE ON WEB DESIGNING , THEIR WEBSITE SHOULD BE DESIGNED IN SUCH A WAY THAT CUSTOMER’S FIRST GAZE AT IT MAKE THEM KNOW WHAT WE ARE CATERING . CATCHY LINES SHOULD BE USED TO MAKE THE CUSTOMERS MORE RELATABLE AND REDUCE THEIR STRESS.

LASTLY , BEFORE DEVOLOPING THE PRODUCT , A MARKETER SHOULD UNDERSTAND THE NEEDS OF THE CUSTOMERS AND WHAT THEY DEMAND , THEN DEVOLOP THE PRODUCT .IT WILL HYPE THE CUSTOMERS , THE SALES AND THE SERVICES , A TREAT FOR OUR ECONOMY RECOVERY .

MOST OF US ARE FASCINATED TOWARDS SPORT WEARS , AS THEIR IS PHYSCHOLOGICAL PERCEPTION THAT IT MAKES US LOOK COOL AND BUILDS OUR PERSONALITY . WE FEEL THE DISTINCT VIBE ALTOGETHER . IF I LIST OUT THE BRANDS DELIVERING THE SPORT WEARS , THE LIST IS ENDLESS , STARTING FROM REEEBOK TO SKETCHERS AND THE LIST GOES ON . THE COMPETITION IS VERY TOUGH IN THIS MARKET , AS THE PRODUCTS ARE SUBSITUTE TO EACH OTHER , THE DIFFRENTIATION CAN ONLY BE MADE IN THEIR PRICES AND QUALITY . WE USUALLY BUY THE PRODUCT ONLY IF WE ARE SATISFIED WITH IT . SO , TO SATISFY THE CUSTOMERS , TO BUILD PROFITABLE RELATIONSHIPS WITH THE CUSTOMERS , TO UNDERSTAND THE NEEDS OF THE CUSTOMERS AND DEVOLOP THE PRODUCT , MARKETERS USE THE MARKETING PHILOSOPHIES AND DESIGN MARKETING STRATEGIES TO ENGAGE THE TARGET MARKET.

FIVE CONCEPTS

THE PRODUCTION CONCEPT

IN THIS CONCEPT , THE MAIN FOCUS OF THE MARKETER IS TO INCREASE THE VOLUME OF PRODUCTION AND ITS DISTRIBUTION TO THE CUSTOMERS. IT IS ASSUMED BY THE MARKETERS THAT THE PRODUCTS ARE AVAILABLE AND HIGHLY AFFORDABLE. THE ELEMENTS ARE LOW COST , HIGH PRODUCTION AND MASS DISTRIBUTION.

TAKING THE EXAMPLE OF REEBOK , IT IS SPORT COMPANY HAVING WIDE REACH TO THE CUSTOMERS AND TARGETING ALMOST ALL THE INCOME GROUPS IN THE COUNTRY. THE PRODUCTS ARE ALSO CHEAPER TO BUY COMPARED TO OTHER BRANDS OF SAME LINE.

THE PRODUCT CONCEPT

IN THIS CONCEPT , THE MAIN FOCUS OF THE MARKETER IS TO DEVOLOP THE PRODUCT INNOVATIVELY. THIS STRATEGY FAVOURS THE CUSTOMERS BY AIMING TO OFFER THE BEST PRODUCT QUALITY , PERFORMANCE AND ITS FEATURES. THE MAIN ELEMENTS OF THIS CONCEPT ARE PRODUCT INNOVATION AND CUSTOMER SATISFACTION.

TAKING THE EXAMPLE OF SKETCHERS , THEIR SHOES , TROUSERS , TEES AND PANTS ARE DIFFRENT FROM OTHER BRANDS. THEIR SHOES ARE FASHIONABLE , CAN BE WEARED IN ANY OCCASSIONS , EVEN FOR COLLEGE. THEY LOOK COOL AND CLASSY. THERE ARE VARIETIES OF COLORS IN PANTS AND TROUSERS WITH LOOSE POCKETS , GIVING IT A ROYAL WEAR LOOK.

THE SELLING CONCEPT

IN THIS CONCEPT , THE MARKETERS MAINLY FOCUS ON INCREASING THE VOLUMES OF SALES WITH STRONG SALES PROMOTION. THE CUSTOMERS CAN ONLY BUY THE PRODUCT IF IT’S IMAGE IS CREATED IN THEIR MINDS WHICH CAN ONLY BE DONE THROUGH RIGOROUS SALES PROMOTION.

I MOST OF THE BUSINESSES USE THIS SO AS TO GAIN SALES . ALSO , NOT EVERY GOOD IS CONSUMED BY THE CUSTOMERS . THIS IS THE BEST STRATEGY TO IMPLEMENT THE SALES OF PRODUCT , NOT IN THE INTRESTS OF BUYERS , FOR INSTANCE , BLOOD DONATIONS , LIFE INSURANCE ETC.

THE MARKETING CONCEPT

IN THIS CONCEPT , THE MAIN FOCUS OF THE MARKETER IS THE ACHEIVEMENT IN THE ORGANSATIONAL GOALS . THE PRIORITY OF THE ENTERPRISES FOLLOWING THIS STRATEGY IS TO UNDERSTAND THE NEEDS OF THE CUSTOMERS , WANTS OF THEIR TARGET MARKET IS WHAT THE ORGANISATIONAL GOALS DEPENDS UPON.IT IS NOT A PRODUCT CENTRED PHILOSOPHY THAT IS MAKE AND SELL PHILOSOPHY . BUT , A CONSUMER CENTRED STRATEGY , SENSE AND RESPOND PHILOSOPHY . THE IDEA BEHIND IS NOT TO FIND RIGHT CUSTOMERS FOR THEIR PRODUCTS BUT TO DEVOLOP RIGHT PRODUCT FOR THE CUSTOMERS.

THE SOCIETAL MARKETING CONCEPT

IN THIS CONCEPT , THE MAIN FOCUS OF THE MARKETER IS THE LONG TERM PROFITS AND LONG TERM SATISFACTION OF THE CUSTOMERS. THIS CONCPT HOLDS THE STRATEGY TO DELIVER VALUE PRODUCTS TO THE CUSTOMERS FOR LONG TERM TO EARN LONG TERM PROFITS . AND IMPROVES BOTH CUSTOMER’s AND SOCIETY’s WELL BEING . BASICALLY , IT IS TO SELL THE PRODUCT TO SATISFY THE CUSTOMERS AND WITH A STRONG MESSAGE TO BRING CHANGE IN THE SOCIETY.

IT IS CALLED AS SUSTAINABLE MARKETING , SOCIALLY AND ENVIROMENTALLY RESPONSIBLE MARKETING .

Article name:A Study of University Students’ Motivation and Its Relationship with Their Academic Performance.

Student motivation is the element that leads students’ attitude towards learning process.God-gifted talents, best teachers and best schooling facilitate the academic performance and students’ motivation is prerequisite for students’ accomplishment. This study attempts to identify the influence of students’ motivation on their academic performance.So come on research enthusiasts let’s look into the why,how and what of student motivation through this review!

This outstanding Research article by Ali and colleagues has been published in the International Journal of Business and Management.This study attempts to identify the influence of students’ motivation on their academic performance.The sample consisted of 342 university students of different programs in various universities of Islamabad and Lahore, Pakistan.The students were asked about how motivated they are about their university experience and what really motivated them to study.

METHODOLOGY

The questionnaire was distributed among both male and female students. There were 82% male and 18% female students in the survey with an average age of 20 years.“The University Student Motivation and Satisfaction Questionnaire version 2″ (TUSMSQ2) instrument was developed by Neill (2004) to measure student’s motivation. TUSMSQ2 instrument contains 30-items.

WHAT WAS TESTED?

The questions measure both Intrinsic and Extrinsic motivation of students. There were two intrinsic motivators; Self-exploration and Altruism and four extrinsic motivators;rejection of Alternative options, career and qualifications, Social enjoyment, and Social pressure in the questionnaire. The questions were based on five point Likert scale. For each item, students rated themselves on a scale of 1 to 5; 1 being “Very False”, towards, 5 being “Very True”

BASIS/THEORY OF THE STUDY

Motivation is state of mind that stimulates activities and human body actions.Student motivation is often separated into two types: Intrinsic motivation and extrinsic motivation.

Intrinsic motivation: A student is intrinsically motivated when he or she is motivated from within. Intrinsically motivated students keenly engage themselves in learning out of oddity, interest, or enjoyment, or in order to achieve their own scholarly and personal goals.Thus students with intrinsic motivation are more enthusiastic, self driven, challenging and feel pleasure in their studies.Intrinsically motivated students tend to prefer challenging tasks.

Extrinsic motivation: It is commonly viewed that extrinsically motivated student engages in learning purely for attaining a reward or for avoiding some punishment.Extrinsic motivation means to obtain some reward or avoid some punishment external to the activity itself such as grades, stickers or teacher approval.Students with extrinsic motivation try to drag themselves with academic assignments, feel compelled to learn, and always put minimal efforts to achieve maximum appreciations.

Results

The results indicate that academic performance amplifies between the ranges of 23 percent and 34 percent due to extrinsic motivation and intrinsic motivation.Also the comparisons of variables on individual bases indicates that those students who adapt self-exploratory variable and altruism variable, rejection of alternative options variable tend to perform better, whereas student who adapt career and qualifications variable, social enjoyment variable and social pressure variable tend to perform less then expected.Also the study found positive and mutually causal relationship between student’s motivation and student’s academic performance. This relationship is reciprocal, meaning students who are more motivated perform better and student who perform better become more motivated.

implications

Any research article would be a waste without implications.This study helps in identifying the factors that will help educational thinkers to know students’ attitudes towards learning, what facilitates learning and what hinders in learning.Thus it will lead to better teaching methods and facilities to suit the student’s need thereby increasing their job competence.

So,this was a comprehensive review of a wonderful research article.Click the below button to read the article:

WELL AWARE OF HOW OUR INDIAN ECONOMY IS DETORIATING AND WILL KEEP ON DIMMING IN THE MONTHS AHEAD AS DECLARED BY INTERNATIONAL MONETARY FUND IN 2019 THAT INDIA WILL BE THE WORST EFFECTED COUNTRY FROM THE GLOBAL ECONOMIC SLOWDOWN. OUR GDP GROWTH IS 4.2% AND FORECASTES TO LOWER DOWN IN NEGATIVE . THE GOVERNMENT IS TAKING BOLD STEPS AND ENSURING TO BRING THE ECONOMY AT THE FAST PACE BY TRYING TO UPLIFT THE PROFIT MAKING. RECENTLY , YOU HEARED OF PRIVATISATION IN RAILWAYS SECTOR , AS DUE TO THE UBIQUITOUS QUALITY OF THE PRIVATE SECTOR , THE INTREST BEING ONLY IN THE ANTICIPATION OF PROFITS . IN MY OPINION , THERE IS NEED OF INCREASE IN PUBLIC INVESTMENT IN THIS SITUATION AS INFLATION IS HIGH DUE TO WHICH , WE ARE FACING ECONOMIC SLOWDOWN AND PEOPLE ESPECIALLY LOWER CLASS AND LABOURS ARE GOING THROUGH THE HARD TIME . ATLEAST WE ARE SITTING AT HOME AND WORKING , BUT , THEY ARE JOBLESS AND VULNERABLE , TIED UP WITH UNEMPLOYMENT AND POVERTY . THEY ARE LEFT SHATTERED , I THINK IF YOU WANT GROWTH , YOU NEED TO ERADICATE POVERTY BECAUSE WHEN IT BACKFIRES , IT WILL MAKE ECONOMY LOOSE ITS BREATH , WHICH IS UNDENIABLY HARMFUL FOR THE COUNTRY . PRIVATISATION EYES ONLY ON MAKING PROFITS WITHOUT GIVING ANY PERKS AND INCENTIVES TO THE EMPLOYEES AS IN PENSIONS AFTER RETIREMENT ETC . ATLEAST GOVERNMENT JOBS ARE SAFE IN THIS ASPECT. MULTINATIONAL COMPANIES WILL OPEN THEIR BRANCHES HERE AND HIRE OUR PEOPLE. THEY WILL MAKE INVESTMENT IN OUR COUNTRY AND PROVIDE LIQUIDITY TO OUR COUNTRY . IS IT WE DON’T HAVE ENOUGH FUNDS WITH US OR INVESTMENTS ARE MADE ONLY IN CORRUPTION JUST TO IBNCREASE THEIR WORTH ? .

THEY GOVERNMENT HAS COME UP WITH THE IMPLEMENTATION OF THE SCHEME NAMED ” ATMA NIRBHAR BHARAT ” WITH THE STRONG MESSAGE OF MAKING “A SELF RELIANT INDIA ” . I THINK IT SHOULD HAVE BEEN DONE EARLIER ,NOT AT THE TIME OF DIFFICULTY , SO THAT WE COULD HAVE NOT FACED THIS ICEBERG IN OUR PATH . THE SCHEME IS GRANTING FUNDS FOR DIFFRENT SECTORS , BUT , THIS MUCH IS NOT SUFFICIENT , THAT’s WHEN THE PRIVATISATION ENTERS. HERE , I AM GOING TO REIMAGINE THE EVENTS AND PUT IT IN FRONT OF YOU .

MAIJOR FUELS

LARGE BUSINESSES ARE THE BEST CONTRIBUTOR IN GENERATING A HUGE SHARE TO GDP , ENHANCING THE GROWTH IN THE ECONOMY . WE ALL KNOW IN OUR COUNTRY , MAIJORLY BUSINESS HOUSES ARE THE ECONOMIC DRIVERS.

MICRO , SMALL , MEDIUM ENTREPRISES ARE LIFELINES TO OUR ECONOMY AS IT TARGETS MIDDLE INCOME POPULATION OF THE ECONOMY WHICH IS ABUNDANT IN OUR COUNTRY.

THE TREND OF START UPs HAS A HUGE CONTRIBUTION TO THE ECONOMIC GROWTH AND DEVOLOPMENT. IT IS THE MEANS OF INJECTING INNOVATIONS AND NEW TECHNOLOGIES IN OUR COUNTRY ALONG WITH THE CREATION OF EMPLOYMENT OPPORTUNITIES.

WE ALSO HAVE PEOPLE LIVING ABROAD AND ARE RESIDENTS OF INDIA , BRINGING BUNDLE OF INVESTMENTS IN INDIA , WHICH IS ADDING TO OUR ECONOMY.

SUPPORT TO FUELS

GOVERNMENT IS SUPPORTING LARGE BUSINESSES TO SUPPORT THEIR OPERATIONS BY WAY OF GRANTING THEM TAX INCENTIVES , PROCUREMENT OF RAW MATERIALS AND OTHER GOODS AND SERVICES , POWERING CONSUMER DEMAND AND FUNCTIONING OF VENDORS , MSME’s.

RSERVE BANK OF INDIA , ANOTHER HELPING HAND WE ALSO CALL IT THE LENDER OF LAST RESORT , PROVIDE RESTRUCTURING OF LOANS TO ALL THE BANKS , SO THAT THEY CAN GIVE LOANS TO SMALL ENTREPRISES TO START OFF THEIR BUSINESSES.

PREPARATION OF FIVE YEAR PLANS BY THE GOVERNMENT AS 60% OF THE COMPANIES IN CHINA HAVE MOVE OUT FOR INVESTING IN INDIA . IT IS A GOOD NEWS BUT WHAT ABOUT SELF RELIANT INDIA?.

FRAMEWORK OF GLOBAL TRADING OPERATIONS FROM INDIA , A GLOBAL TRADING HUB. EXPORTING FINISHED GOODS OUTSIDE INDIA , YES, IT IS A STEP TO SELF RELIANCE.

ESTABLISHMENT OF INDEPENDENT INDUSTRIAL CELLS , COMMERCIALS , MARK SPACE MANUFACTURING , EDUCATION , RESIDENTIAL AND IMPROVING SOCIAL INFRASTRUCTURE.

THEY ARE TOTAL TEN SECTORS THAT RESIDE IN MAKE IN INDIA , FOCUSING IN ATTAINING SELF RELIANCE – ELECTRICAL , PHARMACEUTICAL , MEDICAL DEVICES , AUTOMOTIVE , MINING , ELECTRONICS , HEAVY ENGINEERING , FOOD PROCESSING , RENEWABLE AND CHEMICLA TEXTILES . THIS WILL HELP US TO ACHIEVE THE SUSTENANCE. COUNTRIES LIKE JAPAN , USA , SOUTH KOREA HAVE SHOWN INTREST IN INDIA .

SUNRISERS

ENCOURAGING NATURAl RESOURCES INDUSTRIES SUCH AS BATTERY MANUFACTURE , SOLAR PANEL , BLOCK CHAIN , ROBOTICS , ARTIFICIAL INTELLIGENCE , MACHINES LEARNING , AUGMENTED REALITY , DATA ANALYTICS AND CYBER SECURITY .

AS I SAID EARLIER , THE BENIFITS OF HAVING START UPS IN OUR COUNTRY . THERE IS NEED TO SUPPORT START UP SYSTEMS AS PILING UP OF PRESSURE DUE TO LACK OF LIQUIDITY . THIS RESULTS IN DRIVING INNOVATION AND JOB CREATIONS .

THE CONTRIBUTION TO AUTOMOBILE INDUSTRY , CONTRIBUTING 9% TO GDP , REDUCING GST RATES , OLD VEHICLE SCRAP POLICY AND TABLE THE TAX INCENTIVES EMPHASISING DEMAND CREATION FOR NEW VEHICLES .

MAHARASTRA HAS COME OUT WITH THE PLUG AND PLAY MODEL FOR FOREIGN INVESTORS THAT STATES MUST ACT TOGETHER IN LAND ACQUISITION , LABOUR LAWS , PROVIDING SOCIAL ENVIROMENT AND INFRASTRUCTURE.

REFORMS IN LABOUR LAWS , PROVIDING FACILITIES TO THE TO THEM AND MANTAINING DISCIPLINE WITHIN FACRTORY PREMISES, DEMANDING HIGHER PRODUCTIVITY , PROVIDING HEALTH INSURANCE FACILITIES.

NRI’s AND OCI’s INVESTING IN INDIA IN DIVIDENDS AND INTRESTS OF INDIAN COMPANIES . DIRECT INVESTMWENT SHOULD BE INCENTIVISED . REDUCTION IN CURRENT RATE OF DIVIDENDS OF FOREIGN COMPANIES FROM 15% TO 5% , RESULTING IN MORE FUNDS TO SUPPORT LOCAL PROJECTS.

TAX INCENTIVES

INCOME EARNED FROM DIVIDENDS , INSTRESTS , MUTUAL FUNDS BY NRI’s . THE CAPITAL GAINS ARE TAXED AT 50% OF THE RATES APPLICABLE IN NEXT 30 YEARS.

INTRESTS , ROYALITY DIVIDENDS SHOULD BE TAXED AT 5% FOR OVERSEAS INDUSTRIES . GOVERNMENT HOLDING 3 TO 4 YEARS OF MONOTARIUM FOR LOW COST BORROWINGS .

SHARES ISSUED BY NRI’s WILL BE PROVIDED RELAXATION ON THE FUNDS RECIEVED BY THEM . THEY ARE SUBJECT TO SIMPLE DOCUMENTS SUCH AS BANKS FOREIGN INWARD , KYC DOCS ETC.

TO STRUCTURE OUTSIDE BUSINESSES IN INDIA , SO INDIAN LAWS WILL BE APPLICABLE . FOR INSTANCE , SETTLE THE BUSINESS IN MUMBAI FROM SINGAPORE , AN OFF SHORE INVESTMENT.

EVERYTHING WITH THE OBJECTIVE OF BECOMING SELF-RELIANT !

Market refers to all such system or arrangements that bring the buyers and sellers in contact with each other to settle the sale and purchase of goods.

PERFECT COMPETITION- It is a form of form of market where there is large no. of buyers and sellers of a homogeneous product whose price is determined by forces of supply and demand. An individual buyer has no control over price.

FEATURES- i) Large no. of buyers and sellers: All producers contribute insignificantly to the market. A firm can sell any amount of good at given price it cannot influence market price. So firm is considered as price taker, not maker.

ii) Homogeneous Product- Zero degree of product differentiation led uniform price in market. There is no selling or advertisement costs.

iii) Free entry and exit conditions- Firm earn only normal profits in long run as in case of extra normal profits new firms will join industry and supply increases causing fall in price and vice-versa.

iv) Perfect knowledge on the part of buyers and sellers- The buyers know in full about the commodity sold and the price prevailing in the market. The sellers know the potential sales at various price levels in the market.

v) Independent decision making- Firms do not form trusts or cartels so we have maximum output and minimum price.

vi) Absence of transport cost- If transport costs are incurred, prices should be different in different sectors of the market.

vii) Perfect mobility of factors of production- It leads to uniform price of factor, no matter who hires it.

In the long run, perfectly competitive firms will react to profits by increasing production. They will respond to losses by reducing production or exiting the market. Ultimately, a long-run equilibrium will be attained when no new firms want to enter the market and existing firms do not want to leave the market, as economic profits have been driven down to zero.

Accounting is used to keep a record of all transactions in the business. The accounting process includes summarizing, analyzing and reporting these transactions to oversight agencies, regulators and tax collection entities. It helps to handle all the documentation at a particular place. Accounting is a necessary function for decision making, cost planning, and measurement of economic performance measurement. Accounting process help to derive inference about the profit and loss transactions of the business. Accounting also helps organizations to plan their finances by developing budgets and forecasts.

CLASSIFICATION OF ACCOUNTING- i) Financial Accounting: This process help to develop the balanced sheets of a firm i.e. the net cash flow during a particular time period. These sheets are also called financial statements. This is important to develop by every organisation operating as it help to know the requirement of loan and net profits as a whole.

ii) Cost Accounting: It help to track down the production cost of the commodity on large scale. The difference between financial and coast accounting is that; In cost accounting, money is cast as an economic factor in production, whereas in financial accounting, money is considered to be a measure of a company’s economic performance.

iii) Managerial Accounting: A managerial accountant must be careful in communicating confidential information and to whom. They work with their managers to analyze and create a budget to meet the needs of the short and long-term goals of the organization.

iv) Tax accounting: As the name suggest, it help to track the annual tax reports to be given as income tax. This helps to reduce tax burden on the firm.

v) Public accounting: Public accounting refers to businesses that provide accounting advice to clients based on their needs. They can work in auditing, assist with tax returns, consult on procedures tailored to the installation of technology or computer programs and provide legal advice.

ACCOUNTING CYCLE- The summoning of all type of accounting gives us what we called an accounting cycle. It help the organisation to establish a system of check and balances.The sequence of steps starts when a transaction occurs and ends with its entry in financial reporting.

To have a successful business having a crucial knowledge of accounting is necessary.

5 Latest Sustainable Development Goals in the Corporate World.

Sustainable Development Goals by private firms has increased noticeably since the last decade. Many big corporates like Google, Apple, Dell, Tech Mahindra, Hero MotoCorp, etc. are working with the view of sustainable development since the beginning. Let’s look at some recent sustainable development goals and initiatives by private firms.

1. Microsoft

Microsoft is setting multiple sustainable development goals and adopting different approaches to tackle environmental degradation. The company recently launched its initiative ‘Zero waste by 2030’ focusing on carbon, water, ecosystems, and waste.

Building Microsoft Circular Centers to reuse and repurpose servers and hardware in their data centers.

Eliminate single-use plastics in packaging.

Improve their waste accounting technology.

Invest in circular economy ventures.

Help employees to reduce their own waste footprints.

Microsoft headquarters, Redmond. Source: Microsoft

2. Vestas

It is the first renewable energy manufacturer verified by ‘Science-based target initiatives’ for its sustainable development goals. Vestas has earlier made many contributions to environment protection.

Vestas announced its green initiative to become carbon neutral, without using offsets, by 2030.

IPCC in a recent report, states that limiting the rise in the global temperature to 1.5°C, as stated in the Paris Agreement, will significantly reduce the risk of extreme affects from climate change.

Reduce greenhouse gas emissions by 45% within its own supply chain.

Carbon neutrality and minimize energy consumption.

100% renewable electricity for offices and data centers.

Remote jobs to reduce travel emissions.

Support other organizations in their climate actions.

Help employees to volunteer for environmental causes.

4. Crown

Packaging firm ‘crown’ laid out their initiative ‘Twentyby30’ containing 20 sustainable development goals aiming to get accomplished by 2025, 2030, and 2050. The initiatives include:

Send zero waste to landfill

Make aluminum and steel cans 10 percent lighter to reduce the usage of packaging material.

Increase the recycling of its plastic strapping by 10 percent.

5. Salesforce

The latest initiative of this AI-based CRM firm is to achieve 100% renewable power by 2022. This renewable energy deal is in collaboration with Bloomberg, Cox Enterprises, Gap Inc., and Workday, Inc. and with guidance from LevelTen. The sustainable development goal is to provide renewable energy at a small scale, available to everyone. Currently, renewable energy contracts are made at a high scale involving large investments which are not feasible for small-scale organizations and individuals.

It is an illegal practice in which businesses plot and devise to allow over another to secure contracts at higher prices, thereby undermining free – market competition. Bid rigging infringe antitrust laws and is closely related to horizontal price – fixing, in that both offenses include collusion between supposed competitors in the same market group.

Bid Rigging comes about in situations in which companies are required to competitively bid contracts.

Competitively bid contracts are very well-known in the marketplace, particularly in government and education, where agencies are generally required to the minimal bid of a contract. It is not usual for competitors in same marketplace to plot to allow one or other to win a competitive bid in rotation. Then end result is that each of the companies will make a profit, often at a price well above that which they would have earned in a truly competitive market. The added costs resulting from the rigged bid are passed on to taxpayers, ratepayers and consumers.

COLLUSIVE BIDDING

Collusive bidding refers to agreements by contractors or suppliers in a particular trade or area to cooperate to defeat the competitive bidding process in order to inflate prices to artificially high levels. It can occur in large and small contracts. Where collusive bidding is well established prices can rise substantially, in some cases by as much as several hundred percent.

Collusion in international projects often involves corruption, in which government officials and procurement personnel under their direction sponsor or facilitate the collusion in exchange for bribes. All or part of the corrupt payments often end up in the coffers of local political parties where they are used to offset campaign and other expenses.[1]

INTRODUCTION

The Competition Act, 2002, (as amended), [the Act], follows the philosophy of modern competition laws and aims at nurturing and promoting competition and at protecting Indian markets against anticompetitive practices by enterprises. The Act prohibits anticompetitive agreements, exploitation of dominant position by enterprises, and regulates combinations (mergers, amalgamations and acquisitions) with a view to ensure that there is no adverse effect on competition in India.

The Act forbids any agreement which causes, or is likely to cause, significantcontrary effect on competition in markets in India. Any such agreement is considered void.

An agreement may be parallel i.e. between enterprises, persons, associations, etc. engaged in indistinguishable or similar trade of goods or provision of services, or it may be vertical i.e. amongst enterprises or persons at different stages or levels of the production chain in different markets.

Bid rigging or collusive bidding is one of the horizontal agreements, which shall be presumed to have appreciable adverse effect on competition under Section 3 of the Act.

UNDER THE COMPETITION ACT, 2002

The Competition Act, 2002 (‘Act’), ‘bid rigging’ has been defined in the Explanation to Section 3(3) as:

“An agreement, between enterprises or persons referred to in sub-section 3 engaged in identical or similar production or trading of goods or provision of services, which has the effect of eliminating or reducing competition for bids or adversely affecting or manipulating the process for bidding.”

Section 3(1) of the Act prohibits and Section 3(2) of the Act makes void all agreements by enterprises or persons in respect of production, supply, distribution, storage, acquisition or control of goods or provision of services which cause or are likely to cause appreciable adverse effect on competition within India.

Further, Section 3(3)(d) of the Act uses both expressions viz., ‘bid-rigging’ and ‘collusive bidding’. Both these terms are normally used interchangeably to describe many forms of illegal anti-competition bidding. However, common thread running through these activities is that they involve some kind of agreement or informal arrangement among bidders, which limits competition.

The act treats agreement between bidders which result into bid rigging on presumptive rule approach, meaning hereby that once the essential ingredients constituting bid rigging are established there is no need to further launch into an elaborate inquiry to find out impact of such conduct on the market and adverse effect on competition is presumed.

In that situation, the burden shifts on the contravening parties to rebut the presumption by showing that their conduct does not result into “appreciable adverse effect on competition in India.”

DIFFERENT KINDS

Collusive bidding or bid rigging may be of different kinds, for instance-

agreements to submit identical bids;

agreements as to who shall submit the lowest bid;

agreements for the submission of cover bids (voluntary inflated bids);

agreements not to bid against each other, agreements on common norms to calculate prices or terms of bids;

agreements to squeeze out outside bidders;

Agreements designating bid winners in advance on a rotational basis, or on a geographical or customer allocation basis.

It is to be noted that an ‘agreement’ between ‘competing bidders’ is a sine qua non for establishing contravention of Section 3 of the Act.

FORMS OF BID RIGGING

Bid rigging may take many forms, but most bid rigging conspiracies usually fall into one or more of the following categories:

BID SUPRESSION

In bid suppression schemes, one or more competitors who otherwise would be expected to bid, or who have previously bid, agree to refrain from bidding or withdraw a previously submitted bid so that the designated winning competitor’s bid will be accepted.

COMPLEMENTARY BIDDING

Complementary bidding (also known as ‘cover’ or ‘courtesy’ bidding) occurs when some competitors agree to submit bids that are either too high to be accepted or contain special terms that will not be acceptable to the buyer. Such bids are not intended to secure the buyer’s acceptance, but are merely designed to give the appearance of genuine competitive bidding. Complementary bidding schemes are the most frequently occurring forms of bid rigging, and they defraud purchasers by creating the appearance of competition to conceal secretly inflated prices.

BID ROTATION

In bid rotation schemes, all conspirators submit bids but take turns to be the lowest bidder. The terms of the rotation may vary; for example, competitors may take turns on contracts according to the size of the contract, allocating equal amounts to each conspirator or allocating volumes that correspond to the size of each conspirator. A strict bid rotation pattern defies the law of chance and suggests that collusion is taking place.

SUBCONTRACTING

Subcontracting arrangements are often part of a bid rigging scheme. Competitors, who agree not to bid or to submit a losing bid, frequently receive subcontracts or supply contracts in exchange from the successful bidder. In some schemes, a low bidder will agree to withdraw its bid in favor of the next low bidder in exchange for a lucrative subcontract that divides the illegally obtained higher price between them.

Almost all forms of bid rigging schemes have one thing in common: an agreement among some or all of the bidders, which predetermines the winning bidder and limits or eliminates competition among the conspiring vendors.

THE PRIMER ADS

Some of the industry conditions favorable to collision are:

There are few sellers

Higher degree of standardization of products, making it easy for competitive firms to agree on a common price structure

Repetitive purchases enabling the vendors to know of the other bidders

Bid rigging can be difficult to detect. However, suspicions may bearoused by unusual bidding or something a bidder says or does. An agreement (in collusion) not to respond to an invitation to tender until after discussions with other persons invited to tender, is also a bid rigging offence. Certain patterns in bids can give rise to suspicion of collusion. Situations of suspicious behavior includethe following (illustrative and not exhaustive):

The bid offers by different bidders contain same or similar errors and irregularities (spelling, grammatical andcalculation). This may indicate that the designated bidwinner has prepared all other bids (of the losers).

Bid documents contain the same corrections and alterationsindicating last minute changes.

A bidder seeks a bid package for himself/herself and alsofor the competitor.

A bidder submits his/her bid and also the competitor’sbid.

A party brings multiple bids to a bid opening and submitsits bid after coming to know who else is bidding.

A bidder makes a statement indicating advance knowledgeof the offers of the competitors.

A bidder makes a statement that a bid is a ‘complementary’,‘token’ or ‘cover’ bid.

A bidder makes a statement that the bidders have discussedprices and reached an understanding.

In exercise of powers vested under Section 19 of the Act, the Commission may inquire into any alleged contravention under subsection (3) of Section 3 of the Act that proscribes bid rigging.

The Commission, on being satisfied that there exists a prima facie case of bid rigging, shall direct the Director General to cause an investigation and furnish a report. The Commission has the powers vested in a Civil Court under the Code of Civil Procedure in respect of matters like summoning or enforcing attendance of any person and examining him on oath, requiring discovery and production of documents and receiving evidence on affidavit. The Director General, for the purpose of carrying out investigation, is also vested with powers of civil court besides powers to conduct ‘search and seizure’.

Under section 33 of the Act, , during the pendency of an inquiry into bid rigging, the Commission may temporarily restrain any party from carrying on the offending act until conclusion of the inquiry or until further orders, without giving notice to such party, where it deems necessary.

After the inquiry, the Commission may pass inter- alia any or all of the following orders under section 27 of the Act:

1) Direct the parties to discontinue and not to reenter such agreement;

2) Direct the enterprise concerned to modify the agreement.

3) Direct the enterprises concerned to abide by such other orders as the Commission may pass and comply with the directions, including payment of costs, if any

4) Pass such other orders or issue such directions as it may deem fit.

The Commission may impose such penalty as it deems fit. The penalty can be up to 10% of the average turnover for the last three preceding financial years upon each of such persons or enterprises which are parties to bid-rigging or collusive bidding. In case the bid-rigging or collusive bidding agreement referred to in sub-section (3) of section 3 has been entered into by a cartel.

The Commission may impose upon each producer, seller, distributor, trader or service provider included in that cartel, a penalty of up to 3 times of its profit for each year of the continuance of such agreement or 10% of its turnover for each year of the continuance of such agreement, whichever is higher. The penalty can therefore be severe, and result in heavy financial and other cost on the erring party.

Section 46 of the Act empowers the Commission to impose lesser penalty upon a party in a cartel if it makes true, full and vital disclosure leading to busting of the cartel. However, during the investigation if it is found that the party has not complied with the condition on which lesser penalty was imposed or disclosure is not vital or false evidence has been furnished, the party may not receive the leniency.

The Competition Appellate Tribunal (COMPAT) is established under Section 53A to hear and dispose of appeals against any direction issued or decision made or order passed by the Commission under specified sections of the Act.

An appeal has to be filed within 60 days of receipt of the order / direction / decision of the Commission.

Microsoft is in advanced talks to acquire the United States operations of the Chinese owned video app TikTok, according to people with knowledge of the discussions, in a deal that would be a concession to White House pressure and make the software giant a major player in social media.

A sale to Microsoft, likely for billions of dollars, would be a win for both TikTok and its parent company, Bytedance Ltd., where executives had feared that the U.S. government would force device makers to take TikTok out of their app stores, according to another person familiar with the matter.

As U.S. president, Trump previously has issued three orders stopping M&A deals involving foreign parties, through the inter-agency Committee on Foreign Investment in the United States.

A deal could be completed by Monday, according to people familiar with the matter. The talks involve representatives from Microsoft, Bytedance and the White House. Talks are fluid, and a deal may not come together.

In a statement to Media, a TikTok representative said: “While we do not comment on rumors or speculation, we are confident in the long-term success of TikTok. Hundreds of millions of people come to TikTok for entertainment and connection, including our community of creators and artists who are building livelihoods from the platform. We’re motivated by their passion and creativity, and committed to protecting their privacy and safety as we continue working to bring joy to families and meaningful careers to those who create on our platform.”

A group of ByteDance investors including Sequoia and General Atlantic, who want to acquire control of TikTok amid the concerns over its Chinese ownership, have valued TikTok at about $50 billion,

The billionaire’s Berkshire Hathaway Inc. spent at least $1.7 billion buying shares of the bank in the last two weeks of July, building its stake to about $25 billion, based on the minimum purchase prices disclosed in regulatory filings. The holdings are Berkshire’s second-largest common stock bet, behind Apple Inc.

A Securities and Exchange Commission filing showed Buffett’s conglomerate bought 21.2 million shares of the banking giant between Tuesday and Thursday. That increased Berkshire stake in Bank of America by $522 million and sets its total position in the bank at 11.8%.

Buffett’s conglomerate piled even further into Bank of America stock after getting a green light earlier this year from the Federal Reserve. The purchases came after the shares slumped almost 30% this year. They’re up 4.3% this month.

Bank shares have been hit lately as concerns about the economy keep interest rates low. Bank of America shares are off by 29% this year.

Though Buffett voiced his usual upbeat tone on the American economy during Berkshire’s annual shareholder meeting in May, he did acknowledge the extreme pressure the Covid19 pandemic is having on certain industries.

Register and Records required to be maintained by an enterprise: An Introduction

The Companies Act, 2013 (the Act) and the rules framed there under (“the Rules”) lays down that every Company incorporated under the Act has to maintain Statutory Registers (“the Registers”). With various provisions incorporated in Companies Act, 2013, it is made clear that every company governed under Companies Act, 2013 is required to maintain statutory registersat its registered office until the dissolution of the company.

Some important requirements relating to registers and records are as below:

1. The Registers need to maintained and kept updated and should be kept at the Registered Office of the Company.

2. Some of the Registers are required to be kept open for inspection by Directors, Members, Creditors and by other persons.

3. A Company is also required to provide the extracts of the Registers, if demanded by Directors, Members, Creditors and by other persons on payment of specified fees.

4. Hence, it is important for all the companies (including one person company incorporated in India to maintain statutory registers.

Place of Keeping the Records and Registers

Unless otherwise notified, it is assumed that statutory registers are kept at the address of the registered office of the company. Such registers may also be kept at any other place in India in which more than one-tenth of the total number of members entered in the register of members reside, if approved by a special resolution passed at a general meeting of the company.

Inspection of Statutory Registers

Companies are required by law to make their statutory registers available for public inspection at their registered office or the address as notified to the Registrar during business hours . The registers shall be open for inspection by any member, debenture-holder, other security holder or beneficial owner without payment of any fees and by any other person on payment of prescribed fees.

Suggested Method of Keeping Statutory Registers

The companies have an option to keep all of their statutory registers together in a bound or loose-leaf folder or book. This ensures all important company documents are filed together and easily accessible for inspection purposes. Furthermore one may also keep digital copies instead of, or in addition to the paper registers.

The “Startup India” initiative announced by the Hon‟ble Prime Minister on 15.08.2015 aims at fostering entrepreneurship and promoting innovation by creating an ecosystem that is conducive to growth of Startup. Startup India is a flagship initiative of the Government of India, intended to build a strong ecosystem for nurturing innovation and Startups in the country that will drive sustainable economic growth and generate large scale employment opportunities.

The efforts of the government are aimed at empowering Startups to grow through innovation and design. It is intended to provide the much needed impetus for the Startups to launch and scale greater heights. In order to meet the objectives of the initiative, the Hon‟ble Prime Minister on 16th January 2016 launched the Startup India Action Plan. The Startup India Action Plan consists of 19 action items spanning across areas such as “Simplification and handholding.”

“Funding support and incentives” and “Industry-academia partnership and incubation”. Since the launch of the programme, a number of forward looking strategic amendments to the existing policy ecology have been introduced, like:

Fund of Funds For providing fund support for Startups, Government has created a „Funds for Startups (FFS) at Small Industries Development Bank of India (SIDBI) with a corpus of Rs 10,000 crore. The FFS shall contribute to the corpus of Alternative Investment funds (AIFs) for investing in equity and equity linked instruments of various Startups. The FFS is managed by Small Industries Development Bank of India (SIDBI) for which operational guidelines have been issued. In 2015- 16, Rs.500 crores was released towards the FFS corpus.

2. Credit Guarantee Fund for Startups Since debt funding for Sartups is perceived as high risk activity, a Credit Guarantee Fund for Startups is being setup with a budgetary corpus of Rs.500 crore per year, over the next four years, to provide credit guarantee cover to banks and lending institutions providing loans to Startups. Once rolled out, the scheme in the lines of credit guarantee scheme for MSME, is likely to provide a huge impetus for enabling flow of much needed credit to the Startups which may run into several thousands of crores.

3. Relaxed Norms in Public Procurement for Startups Provision has been introduced in the procurement policy of Ministry of Micro, Small and Medium Enterprises (Policy Circular No. 1(2)(1)/2016-MA dated March 10, 2016) to relax norms pertaining to prior experience/ turnover for Micro and Small Enterprises. Department of Expenditure has issued a notification for relaxing public procurement norms in respect of all Startups (including medium enterprises) by all central Ministries/ Departments.

4. Tax Incentives

(i) Income Tax Exemption on profits under Section 80-IAC of Income Tax (IT) Act: The Inter-Ministerial Board of Certification is a Board set up by Department for Promotion of Industry and Internal Trade (DPIIT) which validates Startups for granting tax related benefits.

A DPIIT recognized Startup is eligible to apply to the Inter-Ministerial Board for full deduction on the profits and gains from business (exemption under Section 80IAC of the Income Tax Act) provided the following conditions are fulfilled.

The entity should be a private limited company or a limited liability partnership, Incorporated on or after 1st April 2016 but before 1st April 2021, and Products or services or processes are undifferentiated, have potential for commercialization and have significant incremental value for customers or workflow. The deduction is for any three consecutive years out of seven years from the year of incorporation of start-up.

(ii) Tax Exemption on Investments above Fair Market Value.

– DPIIT Recognized Startups are exempt from tax under Section 56(2)(viib) of the Income Tax Act when such a Startup receives any consideration for issue of shares which exceeds the Fair Market Value of such shares.

– The startup has to file a duly signed declaration in Form 2 to DPIIT {as per notification G.S.R. 127 (E)} to claim the exemption from the provisions of Section 56(2)(viib) of the Income Tax Act.

(iii) Introduction of Section 54EE in the Income Tax Act, 1961.

Exemption from tax on long-term capital gain if such long-term capital gain is invested in a fund notified by Central Government. The maximum amount that can be invested is Rs. 50 lakh.

(iv) Amendment in Section 54GB of the Income-tax Act

Exemption from tax on capital gains arising out of sale of residential house or a residential plot of land if the amount of net consideration is invested in prescribed stake of equity shares of eligible Startup for utilizing the same for purchase of specified asset:

a. The condition of minimum holding of 50% of share capital or voting rights in the start-up relaxed to 25%

b. The period of extension of capital gains arising from for sale of residential property for investment in start-ups has been extended up to 31st March 2021.

(v) Amendment in Section 79 of Income Tax Act.

Startups can carry forward their losses on satisfaction of any one of the following two conditions:

a. Continuity of 51% shareholding/voting power or

b. Continuity of 100% of original shareholder.

Legal Support and Fast-tracking Patent Examination at Lower Costs

A scheme for Startups IPR Protection (SIPP) for facilitating fast rack filing of Patents, Trademarks and Designs by Startups has been introduced. The scheme provides for expedited examination of patents filed by Startups. This will reduce the time taken in getting patents. The fee for filing of patents for Startups has also been reduced up to 80%.

Panels of facilitators for Patents and Trademark applications have been formed to facilitate the process of patent filing and acquisition. The facilitators would provide legal guidance and handholding through the entire patent acquisition process free of cost.

Self-Certification based Compliance Regime:

Compliance norms relating to Environmental and Labour laws have been eased in order to reduce the regulatory burden on Startups thereby allowing them to focus on their core business and keep compliance costs low. Ministry of Environment and Forests (MOEF) has published a list of 36 white category industries. Startups falling under the “White category” would be able to self certify compliance in respect of 3 Environment Acts.

The Water (Prevention & Control of Pollution) Act, 1974.

2. The Water (Prevention & Control of Pollution) Cess (Amendment) Act, 2003;

3. The Water (Prevention & Control of Pollution) Act, 1981.

Further, Ministry of Labour and Employment (MOLE) has issued guidelines to State Governments whereby Startups shall be allowed to self-certify compliance in respect of Labour laws. These shall be effective after concurrence of States/UTs.

The Acts are :

The Building and Other Constructions Works (Regulation of Employment & Conditions of Service) Act, 1996.

2. The Inter-State Migrant Workmen (Regulation of Employment & Conditions of Service) Act, 1979.

3. The Payment of Gratuity Act, 1972.

3. The Contract Labour (Regulation and Abolition)) Act, 1970.

4. The Employees Provident Funds and Miscellaneous Provisions Act, 1952

5. The Employees State Insurance Act, 1948

So far 9 States have confirmed compliance to the advisory issued by Ministry of Labour and Employment (MOLE):

Under Atal innovation Mission, Niti Aayog will set up Atal Incubation Centres (AICs) in Public and Private sector. Niti Aayog has received 3658 applications (1719) from academic institutions and 1939 from non-academic instution) for setting up Atal Incubation Centres (AICs) from both Public and Private sector organizations. Under the Mission, a grant in aid of Rs.10 crore would be provided to scale up an existing incubator for a maximum of 5 years to cover the capital and operational costs in running the centre. Niti Aayog has received 233 applications for providing scale up support for established incubation centres.

8. Setting up of Startup Centres and Technology Business Incubators (TBIs)

14 Startup Centres and 15 Technology Business incubators are to be set up collaboratively by Ministry of Human Resource Development (MHRD) and the Department of Science and Technology (DST). Out of the 14 Startup Centres, 10 have been approved. Once MHRD releases its share of Rs.25 lakhs each for the Startup centres, the Startup centres would be supported by DST by December, 2016. Against the target of sanctioning 15 TBIs, 9 TBIs have been approved and other 6 TBIs, 9 TBIs have been approved and other 6 TBIs are under process of being approved.

9. Research Parks

7 Research Parks will be set up as per the Startup India Action Plan. Out of these 7 IIT Kharagpur already has a functional Research Park. Further, DST will establish 1 Research Park at IIT Gandhinagar and the remaining 5 shall be set up by Ministry of Human Resource development (MHRD) at IIT Guwahati, IIT Hyderabad, IIT Kanpur, IIT Kanpur, IIT Delhi and IISc Bangalore.

Eligibility for becoming a Startup Company

The Government of India has announced ‘Startup India’ initiative for creating a conducive environment for startups in India. The various Ministries of the Government of India have initiated a number of activities for the purpose.

An entity shall be considered as a Startup:

i. Upto a period of ten years from the date of incorporation/ registration, if it is incorporated as a private limited company (as defined in the Companies Act, 2013) or registered as a partnership firm (registered under section 59 of the Partnership Act, 1932) or a limited liability partnership (under the Limited Liability Partnership Act, 2008) in India.

ii. Turnover of the entity for any of the financial years since incorporation/ registration has not exceeded one hundred crore rupees. The words “Turnover” is as defined under the Companies Act, 2013.

iii. Entity is working towards innovation, development or improvement of products or processes or services, or if it is a scalable business model with a high potential of employment generation or wealth creation.

Provided that an entity formed by splitting up or reconstruction of an existing business shall not be considered a ‘Startup’.

An entity shall cease to be a Startup on completion of ten years from the date of its incorporation/ registration or if its turnover for any previous year exceeds one hundred crore rupees.

Recognition as Startups

The process of recognition of an eligible entity as startup shall be as under:

i. A Startup shall make an online application over the mobile app or portal set up by the DPIIT.

ii. The application shall be accompanied by –

a. a copy of Certificate of Incorporation or Registration, as the case may be, and

b. a write-up about the nature of business highlighting how it is working towards innovation, development or improvement of products or processes or services, or its scalability in terms of employment generation or wealth creation.

iii. The DPIIT may, after calling for such documents or information and making such enquires, as it may deem fit, –

a. recognise the eligible entity as Startup; or

b. reject the application by providing reasons.

Certification of the Inter-Ministerial Board for availing the Tax Benefit under Section 80-IAC

A Startup being a private limited company or limited liability partnership, which fulfils the conditions specified in sub-clause (i) and sub-clause (ii) of the Explanation to section 80-IAC of the Income Tax Act,1961(Act) may, for obtaining a certificate for the purposes of section 80-IAC of the Act, make an application in Form-1 along with documents specified therein to the Board and the Board may, after calling for such documents or information and making such enquires, as it may deem fit, –

(i) grant the certificate referred to in sub-clause (c) of clause(ii) of the Explanation to section 80- IAC of the Act; or

(ii) reject the application by providing reasons.

The Board” means the Inter-Ministerial Board of Certification comprising of the following members: (i) Joint Secretary, Department of Promotion of Industry and Internal Trade, Convener

(ii) Representative of Department of Biotechnology, Member

(iii) Representative of Department of Science & Technology, Member

Post getting recognition a Startup may apply for Tax exemption under section 80 IAC of the Income Tax Act. Post getting clearance for Tax exemption, the Startup can avail tax holiday for 3 consecutive financial years out of its first ten years since incorporation.

Eligibility Criteria for applying to Income Tax exemption (80IAC)

-The entity should be a recognized Startup

– Only Private limited or a Limited Liability Partnership is eligible for Tax exemption under Section 80IAC

– The Startup should have been incorporated after 1st April, 2016.

Tax Exemption under Section 56 of the Income Tax Act (Angel Tax)

Post getting recognition a Startup may apply for Angel Tax Exemption. Eligibility Criteria for Tax Exemption under Section 56 of the Income Tax Act:

– The entity should be a DPIIT recognized Startup

– Aggregate amount of paid up share capital and share premium of the Startup after the proposed issue of share, if any, does not exceed INR 25 Crore.

Approval for the purposes of clause (viib) of sub-section (2) of section 56 of the Act:

A Startup shall be eligible for notification under clause (ii) of the proviso to clause (viib) of sub-section (2) of section 56 of the Act and consequent exemption from the provisions of that clause, if it fulfils the following conditions:

(i) it has been recognised by DPIIT under para 2(iii)(a) or as per any earlier notification on the subject.

(ii) aggregate amount of paid up share capital and share premium of the startup after issue or proposed issue of share, if any, does not exceed, twenty five crore rupees:

Provided that in computing the aggregate amount of paid up share capital, the amount of paid up share capital and share premium of twenty five crore rupees in respect of shares issued to any of the following persons shall not be included –

(a) a non-resident; or

(b) a venture capital company or a venture capital fund;

Provided further that considerations received by such startup for shares issued or proposed to be issued to a specified company shall also be exempt and shall not be included in computing the aggregate amount of paid up share capital and share premium of twenty five crore rupees.

(iii) It has not invested in any of the following assets,─

(a) building or land appurtenant thereto, being a residential house, other than that used by the Startup for the purposes of renting or held by it as stock-in-trade, in the ordinary course of business;

(b) land or building, or both, not being a residential house, other than that occupied by the Startup for its business or used by it for purposes of renting or held by it as stock-in trade, in the ordinary course of business;

(c) loans and advances, other than loans or advances extended in the ordinary course of business by the Startup where the lending of money is substantial part of its business;

(d) capital contribution made to any other entity;

(e) shares and securities;

(f) a motor vehicle, aircraft, yacht or any other mode of transport, the actual cost of which exceeds ten lakh rupees, other than that held by the Startup for the purpose of plying, hiring, leasing or as stock-in-trade, in the ordinary course of business;

(g) jewellery other than that held by the Startup as stock-in-trade in the ordinary course of business;

(h) any other asset, whether in the nature of capital asset or otherwise, of the nature specified in sub- clauses (iv) to (ix) of clause (d) of Explanation to clause (vii) of sub-section (2) of section 56 of the Act.

Provided the Startup shall not invest in any of the assets specified in sub-clauses (a) to (h) for the period of seven years from the end of the latest financial year in which shares are issued at premium;

Explanation.─ For the purposes of this paragraph,-

(i) “specified company” means a company whose shares are frequently traded within the meaning of Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 and whose net worth on the last date of financial year preceding the year in which shares are issued exceeds one hundred crore rupees or turnover for the financial year preceding the year in which shares are issued exceeds two hundred fifty crore rupees.

(ii) the expressions “venture capital company” and “venture capital fund” shall have the same meanings as respectively assigned to them in the explanation to clause (viib) of sub Section( 2) of Section 56 of the Act.

A startup fulfilling conditions mentioned in para 4 (i) and para 4 (ii) shall file duly signed declaration in Form 2 to DIPP that it fulfills the conditions mentioned in para 4. On receipt of such declaration, the DPIIT shall forward the same to the CBDT.

Indian States with Startup policies

States have a vital role to play in promoting the Startup ecosystem. One of the core strengths of India lies in its diversity, leading to enormous opportunities for cross-learning from each other. Only four State Governments were actively supporting Startups before the launch of Startup India through a State Startup policy. The Startup movement across the country was fragmented and there was a need for consolidating standalone efforts.

Emphasis was also required simultaneously to encourage more and more States to undertake new initiatives. The national priority initiative has led to a wide spread movement across the country and presently 22 States have their own Startup policies. Many other States and Union Territories (UTs) are in the process of drafting their policies and operating guidelines.

CONCULSION

The core functioning of an enabling ecosystem in a State is a function of the policy framework and effective implementation of the same. In the journey of developing a conducive Startup community, it is important that States and UTs exchange and adopt good practices undertaken by each other. Another important role of State is to reduce the regulatory burden on budding Startup founders by simplifying labour, taxation, land, and other laws and regulations under the State purview. Many States are organizing hackathons, boot camps, pitching sessions to promote Startups. Several other States have already begun to actively setup world class incubators for Startups across various sectors.

WAY FORWARD

However, a significant effort is required to accelerate the pace of these initiatives to be at par with the pace of growth of Startups. Concerted initiatives by States will accelerate the growth of Startup ecosystems in their respective territories and transform the country into a flourishing Startup Nation.

LLP is a corporate business vehicle that enables professional expertise and entrepreneurial initiative to combine and operate in flexible, innovative and efficient manner, providing benefits of limited liability while allowing its members the flexibility for organizing their internal structure as a partnership.

The Limited Liability Partnership Act, 2008(LLP Act) does not provide an exhaustive definition. Sub-section (n) of section 2 of the Act states that “limited liability partnership” means a partnership formed and registered under this Act.

NATURE AND CHARACTERISTICS OF LLP

1. The LLP is a body corporate having separate entity from its partners and perpetual succession.

2. An LLP in India is governed by the Limited Liability Partnership Act, 2008 and, therefore, the provisions of Indian Partnership Act, 1932 are not applicable to it.

3. Every Limited Liability Partnership shall use the words “Limited Liability Partnership” or its acronym “LLP” as the last words of its name.

4. An LLP is a result of an agreement between the partners, and the mutual rights and duties of partners of an LLP are determined by the said agreement subject to the provisions of LLP Act, 2008.

5. The LLP being a separate legal entity is liable for all its assets, with the liability of the partners limited only to the amount of contributed by them just like a company. No partner will be individually liable for any wrongful acts of other partners. However if the LLP was formed for the purpose of defrauding creditors or for any fraudulent purpose, then the liability of the partners who had the knowledge will be unlimited.

6. There must be at least two designated partners in every LLP of whom one shall be resident in India.

7. Every LLP shall maintain annual accounts to show its true state of affairs. It must prepare a statement of accounts and solvency every year and file with the Registrar.

8. The Central Government may, whenever it thinks fit, investigate into the affairs of an LLP by appointing a competent Inspector.

9. A firm, private company or an unlisted public company have the option to convert itself into LLP as per the provisions of the Act. Upon such conversion, the Registrar will issue a certificate to that effect. After issuance of a certificate of registration, all the property of the firm or the company, all assets, rights, obligations relating to the company shall be vested in the LLP so formed, and the firm or the company stands dissolved.

10. The name of the firm or the company is then removed from the Registrar of Firms or Registrar of Companies, as the case may be. Like the company, an LLP can be wound up either voluntary or by the Tribunal established under the Companies Act, 2013

11. The LLP Act 2008 also enables the Central Government to apply the provisions of the Companies Act whenever it thinks appropriate.

ADVANTAGES OF LLP

Easy to form: Forming an LLP is an easy process. It is less complicated and time consuming unlike the process of formation of a company.

2. Liability: The partners of the LLP is having limited liability which means partners are not liable to pay the debts of the company from their personal assets. No partner is responsible for any other partner’s misconduct.

3. Perpetual succession: The life of the Limited Liability Partnership is not affected by death, retirement or insolvency of the partner. The LLP will get wound up only as per provisions of the LLP Act.

4. Management of the company: An LLP has partners, who own and manage the business. This is different from a private limited company, whose directors may be different from shareholders.

5. Easy transferability of ownership: There is no restriction upon joining and leaving the LLP. It is easy to admit as a partner and to leave the firm or to easily transfer the ownership to others.

6. Taxation: an LLP is not subject to Dividend Distribution Tax. (DDT). Distributed profits in the hands of the partners is not taxable. For Income Tax purposes, LLP is treated on par with partnership firms.

7. No compulsory audit required: Every business has to appoint an auditor for checking the internal management of the company and its accounts. However, in the case of LLP, there is no mandatory audit required. The audit is required only in those cases where the turnover of the company exceeds Rs 40 lakhs and where the contribution exceeds Rs 25 lakhs.

8. Fewer compliance requirements: An LLP is much easier and cheaper to run than a private limited company as there are just three compliances per year. On the other hand, a private limited company has a lot of compliances to fulfil and has to compulsorily conduct an audit of its books of accounts.

9. Flexible agreement: The partners are free to draft the agreement as they please, with regard to their rights and duties.

10. Easy to wind-up: Not only is it easy to start, it is also easier to wind-up an LLP, as compared to a private limited company.

DISADVANTAGES OF LLP

Restricted Access to Capital Markets: LLPs are small form of business and cannot get its shares listed in any stock exchange through initial public offerings. With this restriction, limited liability partnerships may find it difficult to attract outside investors to buy the shares.

2. Rights of partners: An LLP can be structured in such a way that one partner has more rights than another. So it isn’t a one vote per share system. So, some lesser partners may feel compromised if higher shareholders choose to move the business in a direction that affects their interests.

3. Public Disclosure of LLP Information: A LLP must file its Annual Returns, Financial Statements etc to the Registrar of LLPs annually. Which become public document once filed with Registrar of LLPs and may be inspected by general public including competitors by paying some fees to the Registrar of LLPs. Information disclosure can make an entity competitively disadvantaged. Competitors – especially those not required to disclose any documents – can access that information and use it to improve their own business.

4. Limitations in Formation of LLP: LLP cannot be formed by a single person. A non – resident Indian and a Foreign National willing to form a LLP in India must have one person resident in India to act as Designated Partner. Further FDI in LLP is allowed only through government route only and that too in those sectors only where 100% FDI is allowed under automatic route under the FDI Policy. This limitation makes LLP an unattractive form of business.

5. Offenses and penalties: Limited Liability Partnership Act, 2008 provides that for non-compliance on procedural matters such as delay in filing of e-forms, one has to pay default fee for every day for which the default continues. Such default fee would be payable at the rate of rupee one hundred per day after the expiry of the date of filing up to a period of three hundred days. The offense can result in either:-

(i)through payment of fine or

(ii) through payment of fine as well as imprisonment of the offender.

6. Exit Options are Not Easy for LLPs in default of Filings: A LLP who has defaulted in filings its statement of accounts and annual return with the Registrar of LLPs, willing to shut down its operations and wind up, will have to make its default good first by filing necessary e-forms with late filing fee. This provision is making LLP an unattractive form of business as in India there are many businesses that are ignorant about compliances.

7. Limitation in External Commercial Borrowings (ECB): Limited Liability Partnerships are not allowed to raise ECB. Therefore, a LLP cannot avail commercial loans from its foreign partners, FIIs, Foreign Banks, and any financial institution located outside India.

PROCEDURE FOR AN INCORPORATION OF LLP

The incorporation document shall be filed in Form FiLLiP (Form for incorporation of Limited Liability Partnership) with the Registrar having jurisdiction over the State in which the registered office of the limited liability partnership is to be situated.

If an individual required to be appointed as designated partner does not have a DPIN or DIN,application for allotment of DPIN shall be made in Form FiLLiP The application for allotment of DPIN shall not be made by more than two individuals in Form FiLLiP: an application for reservation of name may be made through Form FiLLiP: Provided also that where an applicant had applied for reservation of name under rule 18 in Form RUN-LLP (Reserve Unique Name-Limited Liability Partnership) and which has been approved, he may fill the reserved name as the proposed name of limited liability partnership.

THE SUMMARIES PROCEDURE FOR

Incorporation of LLP is as under:

Procure DSC and DIN:

Procure DSC and DIN for the individuals acting as Designated Partners of LLP. A person, who already has a DIN, is not require to obtain any new DIN. Existing DIN to be used for Designated Partner (However, DIN should have all latest details such as resident of India, name, address etc.). Any person proposed to become the Designated Partner in a new LLP shall have to make an application through eform FiLLiP. An application for allotment of DIN up to two Designated Partners, shall be filed in an e-form FILLiP with the Registrar, in case of proposed Designated Partners not having approved DIN.

2. Name reservation: The first step in incorporation of an LLP is reservation of name of the proposed LLP. There are two ways of reserving name of the proposed LLP.

i. File an application under LLP-RUN for ascertaining availability and reservation of the name of an LLP.

ii. Name can be proposed in eform FiLLiP, an application for incorporation of LLP.

3. Incorporate LLP: After reserving a name under LLP-RUN, applicant should file eform FiLLiP for incorporating a new LLP. eform FiLLiP contains the details of LLP proposed to be incorporated, Partners’/ Designated Partners’ details and consent of the Partner/ Designated Partners to act as Partners/ Designated Partners. On approval of the form, the RoC will issue the certificate of incorporation.

Where the Registrar, on examining Form FiLLiP, finds that it is necessary to call for further information or finds such application or document to be defective or incomplete in any respect, he shall give intimation to the applicant to remove the defects and re-submit the e-form within fifteen days from the date of such intimation given by the Registrar.

After re-submission of the document, if the Registrar still finds that the document is defective or incomplete in any respect, he shall give one more opportunity of fifteen days time to remove such defects or deficiencies: Provided that the total period for re-submission of documents shall not exceed thirty days.

Documents to be attached with form FiLLiP:

i. Consent of the partners.

ii. In case of the partners who are body corporates, certified true copy of the board resolution is passed by such body corporate partners.

iii. Proof of address of registered office of LLP.

iv. Subscribers’ sheet including consent.

v. Detail of LLP(s) and/ or company(s) in which partner/ designated partner is a director/ partner.

vi. Copy of approval obtained from any sectoral regulator/in-principle approval.

vii. Identity and address proof of individuals acting as Partner and/or Designated Partner.

viii. List of main objects of an LLP.

ix. If the name proposed is liked to registered trademark, NoC from the trade mark owner.