In today’s world, it is very easy to confuse Insurance with Investment. One might feel that he/she is investing in their future and decreasing their future financial burden because he/she purchased an insurance policy. Let’s take a look at the definition of insurance and investment.

Insurance refers to a contract or policy in which an individual or entity receives financial protection or reimbursement against losses. It protects the insured against risk of losses or damage.

Investment, on the other hand, refers to an asset or item acquired with the goal of generating income or appreciation. For example, real estate, mutual funds, shares etc.

With the increase in types of insurance policies and persuasive insurance sales representatives, people tend to think of insurance as investments. However, Insurance merely provides protection in the event of loss, which may or may not arise. In case of no loss or damage, sum total of all the insurance premium paid is profit for the insurance company.

On the other hand, the main purpose of an investment is to generate income by providing returns (dividends and interest) and/or capital gains (value appreciation; increase in price). Insurance does not provide any substantial returns. It merely provides reimbursement in the event of loss/damage and therefore, it is not an investment.

Do you need Insurance? If yes, what kind?

Insurance planning is essential to protect against different kinds of risks and to be financially prepared in case of loss or damage to life or property. However, it should not be used a means to invest.

There are different types of insurance which can be broadly classified into Personal, Property and Liability. There are three types of insurance that you must have to protect against risk, not as an investment: Health insurance, Term life insurance and Automobile insurance.

Health insurance is a must to ensure that in case of an accident or injury, hospital and medical bills don’t eat away your savings.

Term life insurance ensures that in case of death of the earning member of the family, the family has enough to survive for a substantial period of time. Term life insurance has a fixed period and hence, has a very low monthly premium with a decent coverage. However, if the policy expires and the insured is still alive, the insured does not get any amount back. So, this policy should only be taken by the earning member at the right life stage in case he/she does not own enough assets to leave behind for his/her family.

Automobile Insurance (third party) is mandated by the Government of India on the purchase of a vehicle and hence, every vehicle owner should have one.

Other types of insurances sold and bought in the name of ‘investment’ like Endowment plans, Money back policy and the new policy called Unit-linked insurance plans (ULIP) which allows you to invest in the stock market should be avoided at all costs.

It is much more profitable to invest in the market through mutual funds or investor’s Demat account than to do the same through insurance companies. The rate of return in the market is much higher and it doesn’t cost as much as Insurance.

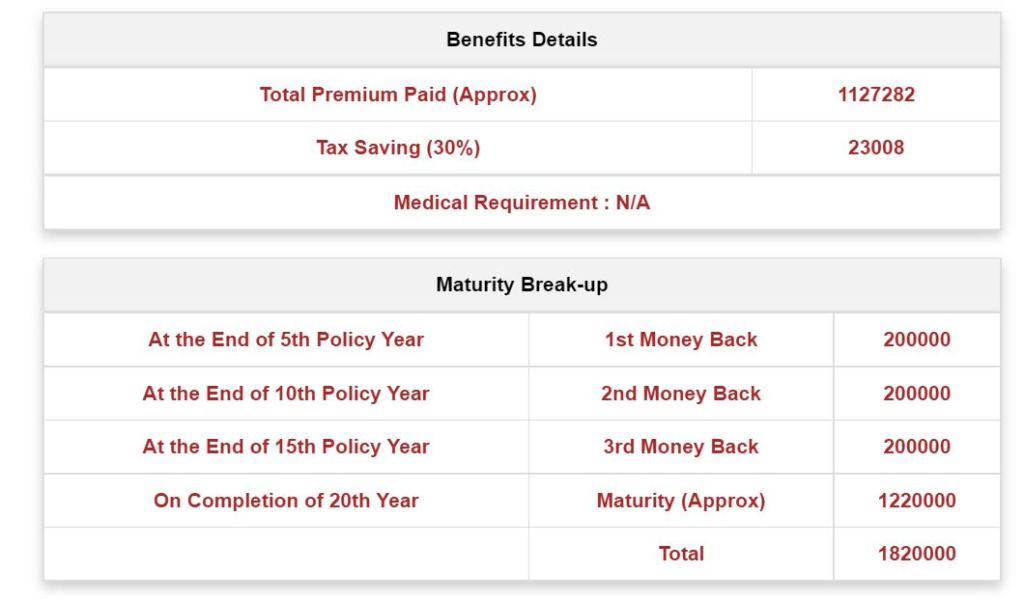

For example, if you buy Money Back insurance plan with a policy term of 20 years with ₹10,00,000 assured cover, the monthly premium calculated on LIC premium calculator comes out to be around ₹6300-6500 per month.

As calculated above, the total premium paid is ₹11,27,282 and the total amount received is ₹18,20,000. The total profit/return (approx.) is only ₹6,90,000 in 20 years. The return on investment (Return/Total Amount paid x 100) is only 61%.

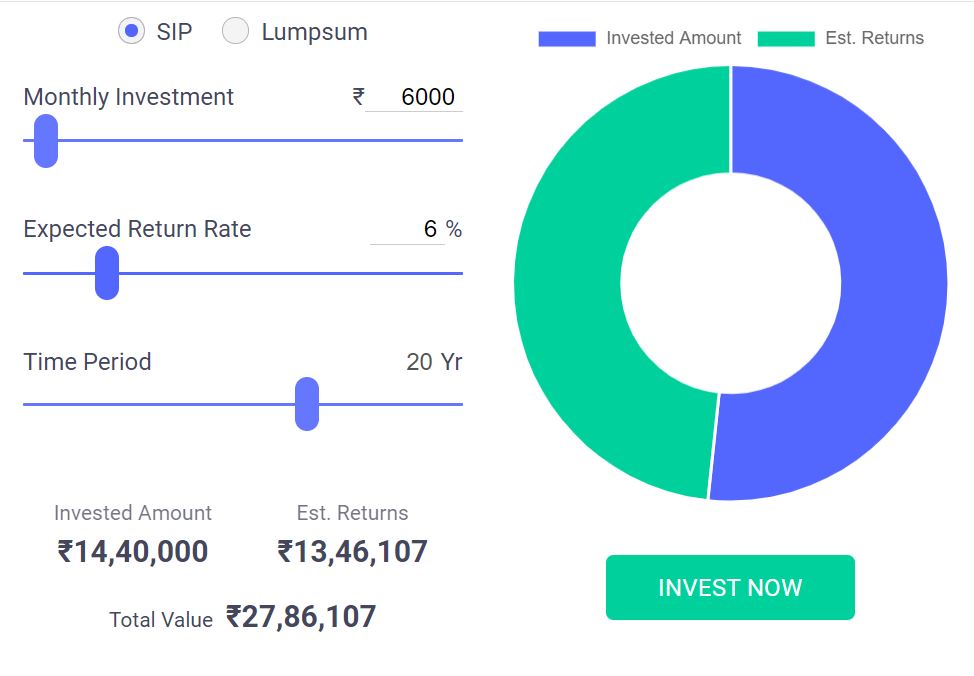

However, if the same amount is invested in SIP of any instrument with a return rate of just 6% for the same time period (20 years), the returns (calculated on Groww SIP calculator) are much higher.

₹6000 rupees invested monthly in any instrument with a return rate of only 6% for 20 years gives a return of ₹13,46,000 making the total value of the investment ₹27,86,000. The ROI (Return/Total Amount paid x 100) in this scenario is 93%.

Conclusion

Although Insurance is an essential part of Financial Planning to protect against different kinds of risks which varies from person to person, it should not be mixed with Investment. For greater returns and growth, investors should directly invest in the market or in any other instrument which suits their risk appetite and capacity.

This helped me so much! Wonderfully explained

LikeLiked by 1 person

An Eye-opener to know the difference… Thank you for providing the clarity

LikeLiked by 1 person