The ASEAN-India and Thailand trade relations have witnessed significant growth over the years, leading to positive impacts on the economies of the participating countries. This paper highlights the benefits and opportunities arising from the flourishing trade relations between India, Thailand, and ASEAN countries, including enhanced market access, increased trade volume, and strengthened economic ties. The study also sheds light on the challenges faced by the ASEAN-India and Thailand trade relations, such as non-tariff barriers and limited infrastructure. The paper concludes that the ASEAN-India and Thailand trade relations have the potential to be a driving force for economic growth and regional integration, and recommends measures to further enhance the trade and investment ties between the regions.

Keywords:

ASEAN, India, Thailand, Trade Relations, India and Thialand

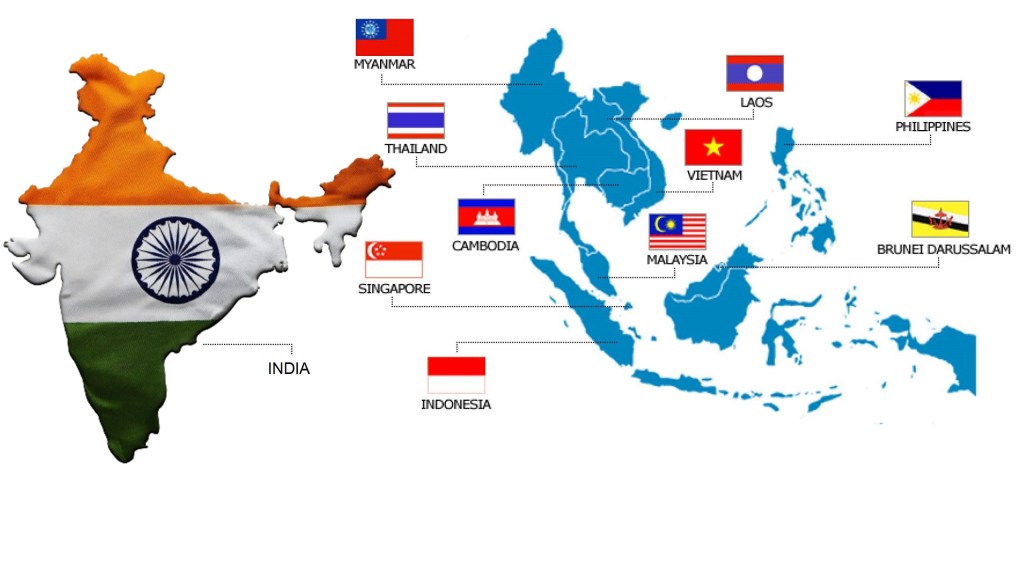

The aim of the Association of Southeast Asian Nations (ASEAN) is to promote economic, political, and security cooperation among its member countries in Southeast Asia. ASEAN was established on August 8, 1967, with the signing of the ASEAN Declaration, also known as the Bangkok Declaration. The founding members of ASEAN were Indonesia, Malaysia, the Philippines, Singapore, and Thailand. Brunei Darussalam joined in 1984, Vietnam in 1995, Laos and Myanmar in 1997, and Cambodia in 1999.

ASEAN’s role in Asia is significant. It is a regional organization that fosters economic integration and cooperation, political stability, and social progress among its member states. ASEAN plays an important role in promoting peace, security, and stability in the region, as well as in enhancing regional economic growth and development. ASEAN also serves as a platform for dialogue and cooperation between the member states and with other countries in the region and beyond. It has established several partnerships with countries such as China, Japan, South Korea, India, and the United States, among others.

In recent years, ASEAN has become increasingly important in the evolving regional security architecture of Asia, particularly with the rise of China and its growing influence in the region. ASEAN-led forums such as the East Asia Summit (EAS) have become key platforms for discussing security issues in the region, including the South China Sea disputes.

India and Thailand share a long-standing historical and cultural relationship that dates back several centuries. India and Thailand have been trading partners for over two thousand years, with cultural and economic exchanges flourishing during the ancient times along the land and sea routes. In recent times, India and Thailand have developed a strong strategic partnership based on shared values and interests. The two countries have close economic ties, with Thailand being one of India’s important trading partners in the ASEAN region. The total trade between India and Thailand stood at USD 13.76 billion in 2020-21.

India’s main exports to Thailand include gems and jewelry, machinery, iron and steel, organic chemicals, and vehicles. Thailand’s main exports to India include pearls, precious stones, electrical machinery, boilers, machinery, and parts. India and Thailand also cooperate in areas such as defense, security, tourism, and cultural exchanges. In the defense sector, the two countries have been conducting joint military exercises, and Thailand has purchased military hardware from India.

Tourism is another area of cooperation, with over a million tourists from each country visiting the other annually before the COVID-19 pandemic. Cultural exchanges between the two countries are also vibrant, with several cultural festivals and events being held in each other’s countries. India and Thailand also collaborate in regional forums such as ASEAN, BIMSTEC, and the Mekong-Ganga Cooperation. The two countries share a commitment to promoting regional integration and connectivity in the region.

The 13th Meeting of the India Thailand Joint Trade Committee (JTC) took place in New Delhi today. Ms. Auramon Supthaweethum, the Director General of Department of Trade Negotiations, Ministry of Commerce of Thailand, and Ms. Indu C. Nair, the Joint Secretary, Department of Commerce, Ministry of Commerce & Industry, India, co-chaired the meeting. This was the first in-person meeting of the JTC since its revival in 2020, after a 17-year hiatus.

Thailand is an important trading partner for India in the ASEAN region, with a total trade of USD 16.89 Billion in 2022-23, accounting for 13.6% of India’s total trade with ASEAN. India exports gems and jewelry, mechanical machinery, auto and auto components, and agricultural products, especially marine products, to Thailand.

During the meeting, the chairs reviewed the current status of bilateral trade and discussed the need to identify new potential products and priority sectors to expand bilateral trade. They also discussed market access issues and technical barriers faced by exporters and agreed to resolve them through regular and sustained bilateral discussions. India raised concerns about the restrictions it faces in exporting marine, poultry, and meat products.

Both sides identified several potential commodities and sectors for a stronger partnership, such as value-added marine products, smartphones, electric vehicles, food processing, and pharmaceuticals. They also agreed that there is a vast scope for collaboration in the service sector and decided to explore establishing mutual recognition/cooperation arrangements in nursing, accounting, audio-visual, and medical tourism. The meeting also reviewed the progress of the ongoing efforts to connect India’s Unified Payment Interface (UPI) with Thailand’s Prompt Pay Service and the settlement of trade transactions in local currency.

Some recommendations for enhancing the India and Thailand trade relations are:-

Strengthen bilateral economic engagement through the establishment of joint ventures, investment, and technology transfer.

Enhance connectivity between the two countries by improving transport links, including air and sea connectivity.

Promote cooperation between small and medium enterprises (SMEs) in both countries to enhance trade and investment.

Work towards establishing mutual recognition/cooperation arrangements in various sectors, including nursing, accounting, audio-visual, and medical tourism.

Address trade barriers and technical issues faced by exporters through regular and sustained bilateral discussions.

Explore the possibility of signing a Free Trade Agreement (FTA) to further enhance economic engagement between the two countries.

Overall, there is significant potential for India and Thailand to deepen their trade and economic partnership. By addressing trade barriers, promoting cooperation in key sectors, and enhancing connectivity between the two countries, India and Thailand can further strengthen their relationship and realize the untapped potential of their trade and economic ties.

References

Sivadasan, S. K., Susheel, M. A., & Bindu, C. (2012). India-Thailand Bilateral Trade A Review against the Backdrop of the Framework Trade Agreement. ABAC Journal, 32(3).

Asher, M. G., & Sen, R. (2005). India-East Asia integration: A win-win for Asia. Economic and Political Weekly, 3932-3940.

Chenoy, A. M. (2023). The Multipolar Global Political Economy. Economic & Political Weekly, 58(2), 31.

Francis, S. (2011). A sectoral impact analysis of the ASEAN-India free trade agreement. Economic and Political Weekly, 46-55.

Marwah, R. (2020). Reimagining India–Thailand Relations: A Multilateral and Bilateral Perspective.

Nataraj, G., & Sekhani, R. (2015). China’s One Belt One Road: An Indian Perspective. Economic and Political Weekly, 67-71.

Sen, R., Asher, M. G., & Rajan, R. S. (2004). ASEAN-India economic relations: current status and future prospects. Economic and Political Weekly, 3297-3308.

Employees who work in a company are expected to know well the core values, culture and goals of the organization, so that employees can get to know the company where they work well. However, outsourcing employees who basically come from service providers outside the company do not know about this. Therefore it is difficult for outsourcing employees to grow their work loyalty to the company where they work. Meanwhile, loyal employees are related to the goals, objectives, culture and values of the organization. Employee loyalty can go up and down, one of which is due to job satisfaction factors. Job satisfaction felt by employees can increase employee work loyalty. Therefore, we need a motivator in the form of meeting physical and non-physical needs. This need is an encouragement or motivation for employees to work in a company. This study aims to determine the effect of job satisfaction and work motivation on work loyalty of outsourcing employees. This study uses a quantitative approach with research participants totaling 100 outsourcing employees obtained through sampling techniques. The analysis method used is simple and multiple regression. Based on the data analysis that has been done, it is known that there is an effect of job satisfaction on work loyalty of outsourcing employees by 54.3%, there is an effect of work motivation on work loyalty of outsourcing employees by 47.1% and there is an effect of job satisfaction and work motivation which together affect work loyalty of outsourcing employees by 25.7%, the remaining is influenced by other factors outside the research.

Keywords: Job Satisfaction, Work Motivation, Work Loyalty, Outsourcing

Products and services that have quality will certainly be able to compete globally to improve their competitive position in the increasingly global market. Companies can save costs and maintain quality by relying more on external service providers for activities that are seen as complementary to their core business. This is related to outsourcing which functions as a partnership to improve the company’s business (Elmuti., Grunewald., & Abebe, 2010).

One of the complementary activities to improve the company’s business is recruitment. Every prospective employee who is accepted feels unclear about their employment status, namely outsourcing employees or permanent employees. Employee status is a condition that distinguishes one employee from another in the company. Employment status is a person’s position in doing work, namely whether the person’s position is as a laborer or employee. The status of outsourcing employees is included in non-permanent employees and their employment status is included in outsourcing employees (Barthos, 2001).

Outsourcing is the delegation of daily operations and management of a business process to an external party (an outsourcing service provider). Through delegation, management is no longer carried out by the company, but is delegated to the outsourcing service company (Soewondo, 2004). In addition, according to Wahyuningtyas & Utami (2018) Outsourcing is an effort to obtain skilled workers and reduce the burden and costs of the company in improving the company’s performance so that it can continue to be competitive in facing global economic and technological developments by handing over the company’s activities to other parties.

The handover of HR activities to outsourcing services is widely used by organizations around the world, because it is considered profitable. As is the case in the telecommunications industry of Pakistan. In the telecommunications sector of Pakistan, external recruitment companies or so-called outsourcing are known to have high work loyalty. Although they do not know the core values, culture, and goals of the organization well, employees are still able to grow their work loyalty. Employees can quickly adapt to their work environment because a comfortable work environment is created so that employees feel at home and are willing to stay in the company as long as they are still needed by the company. Work loyalty is related to the goals, objectives, culture, and values of the organization. Employees are able to know and adapt to this after they have been in an organization for a long time (Jamil & Naeem, 2013).

According to Flippo (2013) Work loyalty itself is the determination and ability to obey, carry out and practice something that is obeyed with full awareness and responsibility. Robbins (2006) defines loyalty as the willingness to protect and save oneself. While Hasibuan (2002) describes loyalty as loyalty reflected by the willingness of employees to maintain and defend the organization inside and outside of work.

Work loyalty is fundamental to the industry because loyal employees will provide high work results along with work efficiency (Elmuti, Grunewald, & Abebe, 2010). Companies that fail to create strategic HR practices can lose valuable employees due to lack of employee loyalty to the company (Meyer & Allen, 1997). Through outsourcing, companies generate profits through HR which is the company’s most valuable asset. While HR itself will feel disadvantaged, so that employees are unable to grow their loyalty in working in the company where they work (Jamil & Naeem, 2013).

Employee loyalty in an organization is absolutely necessary for the success of the organization itself, one of the factors that causes employee work loyalty to increase or decrease is job satisfaction (Citra. L.M., & Fahmi. M, 2019). According to Colquitt, LePine, & Wesson (2012) Job satisfaction is a level of pleasant feeling obtained from the assessment of one’s work or work experience. In addition, according to Mathis and Jackson (2000) job satisfaction is a positive emotional state resulting from the evaluation of work experiences carried out by an individual.

Achieving employee job satisfaction will increase employee work loyalty. Job satisfaction expresses a number of conformities between a person’s expectations about his/her work, which can be in the form of work performance given by the company and the rewards given for his/her work. In essence, a person is encouraged to be active because he/she hopes that it will bring a better and more satisfying situation than the current situation. So working is a form of activity that aims to obtain job satisfaction (Mathis and Jackson, 2000).

Job satisfaction can be seen from employees who feel happy with their work. They will give more attention, imagination and skills in their work. Therefore, a motivator is needed for employees, namely providing physical and non-physical needs. These needs are an encouragement for employees in carrying out activities in a company. This encouragement is called work motivation (Arianty, Bahagia, Lubis, & Siswadi, 2016).

According to Vroom (in Setiawan, 2015) work motivation is how much effort is made to achieve certain results or rewards. Meanwhile, according to Purnama (2008), work motivation is the entire process of providing work motivation to subordinates in such a way that they are willing to work sincerely in order to achieve organizational goals efficiently and economically.

Based on the results of research conducted by Jamil & Naeem (2013) showed that work loyalty has an impact on outsourcing employees. This means that work loyalty that grows in each individual does not depend on the status of the employee, whether permanent or outsourcing. Employee loyalty that grows in the outsourcing company has a positive impact on employee engagement, employees have a sense of attachment to the organization or company where the employee works. In addition, research conducted by Wibowo & Sutanto (2013) also stated that the results of the study showed that there was an influence of job satisfaction and work motivation on employee loyalty in the sales department where if the work motivation of employees in the sales department increased, then the loyalty of employees in the sales department would increase. The regression results also showed that employee loyalty CV. Pratama Jaya was influenced by job satisfaction and work motivation, which was 66.7%. Another study conducted by Thanos, Pangemanan, and Rumokoy (2015) also stated that work motivation and job satisfaction had a significant partial effect on employee loyalty at PT Kimia Farma Apotek.

Based on the explanation that has been presented previously, the hypothesis that can be developed in this study are:

H1: job satisfaction and work motivation affect work loyalty in outsourcing employees;

H2: job satisfaction affects work loyalty in outsourcing employees;

H3: work motivation affects work loyalty in outsourcing employees.

RESEARCH METHODS

The population in this study were outsourcing employees and had the following characteristics: outsourcing employees, had worked for 6 months to 3 or more, because it is expected that during this period of work, real behavior can be seen which is reflected as an action of their loyalty in working for the company where the outsourcing employee works.

The sample (subject) of the study consisted of 100 outsourcing employees who had the same characteristics as the population. Sampling was carried out using non-probability sampling techniques and with purposive sampling types. The answer choices on each scale range from 1 – 6 ranging from strongly disagree to strongly agree.

Job satisfaction in this study can be seen through the scores obtained in the job satisfaction scale according to Spector, (1994) namely aspects of salary, promotion, superiors, benefits, non-material rewards, working conditions, coworkers, nature of work, and communication. This measuring instrument contains 36 items divided into 17 favorable items and 19 unfavorable items. One example of an item in the job satisfaction scale is “I feel paid a fair amount for the work I do”. Based on the results of the analysis of the reliability test of the job satisfaction scale, a Cronbach alpha of 0.870 was found, which means that the scale is reliable in measuring job satisfaction.

Work motivation in this study can be seen through the scores adapted by researchers from Tremblay, MA, Blanchard, CM, Taylor, S., Villeneuve, M., and Pelletier, LG (2009) which are arranged based on the form of work motivation according to Deci & Ryan (2000) namely amotivation, intrinsic motivation, external regulation, projected, identified, integrated, extrinsic motivation. This measuring instrument contains 18 favorable items. One example of an item in the work motivation scale is “The awards given by the company are appropriate”. Based on the results of the analysis of the reliability test of the work motivation scale, a Cronbach’s alpha of 0.840 was found, which means that the scale is reliable in measuring work motivation.

Work loyalty in this study is known based on the score obtained through the work loyalty measurement scale adapted by Asih (2018) which is compiled based on aspects of work loyalty, namely obeying regulations, being responsible, dedicated and honest in working. This measuring instrument contains 32 items divided into 30 favorable items and 2 unfavorable items. One example of an item in the work loyalty scale is “I like to work hard, am agile and always want to do my best for the company”. Based on the results of the analysis of the reliability test of the work loyalty scale, a Cronbach’s alpha of 0.967 was found, which means that the scale is reliable in measuring work loyalty.

The data processing technique in this study used simple and multiple regression tests.

RESULTS AND DISCUSSION

Based on the results of the reliability test in this study to determine the consistency of the measuring instrument based on items that have been declared to have good discrimination power and proven by the Alpha Cronbach technique with the help of the IBM SPSS Statistic version 23 program. According to Azwar (2012) the reliability coefficient on the scale that shows high consistency and stability of values, namely 0.70 to 1. Based on the results of the reliability test that has been carried out, the scale of job satisfaction, work motivation and work loyalty is known to have good alpha Cronbach reliability test values, this means that the reliability coefficient on the scale as a whole shows high consistency and stability of values. The results of the reliability test on the three variables can be seen in the following table:

Table 1. Reliability Test

Variable

Alpha Cronbach

Result

Job Satisfaction (X1)

0,870

Reliable

Work Motivation (X2)

0,840

Reliable

Work Loyalty (Y)

0.967

Reliable

Based on the results of the study, it is known that the variables of job satisfaction and work motivation have an effect on work loyalty in outsourcing employees. The results of the regression test on the three variables can be seen in the following table:

Table 2. Regression Test

Variable

F

R

R Square

Sig

Job Satisfaction (X1)

117,576

0,739

0,543

0,000

Work Motivation (X2)

87,160

0,686

0,471

0,000

Job Satisfaction (X1) and Work Motivation (X2)

16,773

0,507

0,257

0,000

on Work Loyalty (Y)

Effect of Job Satisfaction on Work Loyalty

Based on the results of data analysis on the job satisfaction variable, the F value is 117.576 and the significance coefficient is 0.000 (p <0.01), meaning that the job satisfaction variable has a very significant effect on work loyalty. The R value on job satisfaction of 0.739 indicates a positive relationship direction and a strong relationship. The R Square value of 0.543 means that job satisfaction affects work loyalty by 54.3%, the remaining 45.7% is influenced by other factors.

These results indicate that the hypothesis that states that there is an effect of job satisfaction on work loyalty in outsourcing employees is accepted. This means that the satisfaction felt by employees in working can increase or decrease their work loyalty to the company. The results of this study are in line with research conducted by Susilowati and Supriyadi (2018) which states that job satisfaction affects work loyalty by 34.3%. The higher the job satisfaction felt by employees, the higher the employee’s work loyalty to the company.

Employees who are satisfied will achieve work loyalty within the company. Job satisfaction is basically something that is individual, while each individual has a different level of satisfaction. In a company, leaders must pay serious attention to the job satisfaction of the employees they lead, because job satisfaction has a chain with the organization’s human resources, organizational performance, and the sustainability of the organization itself (Husni., Musnadi., and Faisal, 2018).

Effect of Work Motivation on Work Loyalty

Based on the results of data analysis on the work motivation variable, the F value is 87.160 and the significance coefficient is 0.000 (p <0.01), meaning that the work motivation variable has a very significant influence on work loyalty. The R value on work motivation of 0.686 indicates a positive relationship direction and a strong relationship. The R Square value of 0.471 means that work motivation affects work loyalty by 47.1%, the remaining 52.9% is influenced by other factors. These results indicate that the hypothesis that there is an influence of work motivation on work loyalty in outsourcing employees is accepted. This means that work loyalty can grow and increase if the motivation felt by employees in working also increases.

The results of this study are in line with research conducted by Swadarma and Netra (2020) which states that there is a positive and significant influence between work motivation and employee loyalty at Rame Cafe Jimbaran of 41.6%. If motivation increases, employee loyalty will increase. High work motivation in employees will make employees work harder in carrying out their work. On the other hand, with low work motivation, employees do not have work enthusiasm, give up easily and have difficulty completing work (Husni., Musnadi., and Faisal, 2018).

The growing employee work motivation can come from themselves or from outside themselves. According to Herzberg (in Robbins & Judge, 2006) stated that basically motivation is divided into two main types, namely, intrinsic motivation and extrinsic motivation. Intrinsic motivation is motivation related to themselves to feel satisfied such as achievement, appreciation, responsibility, opportunities to advance, and the work itself. While extrinsic motivation is motivation from outside themselves such as physical working conditions, interpersonal relationships, company policies and administration, supervision, salary, and job security.

Effect of Job Satisfaction and Work Motivation on Work Loyalty

Based on the results of data analysis on the variables of job satisfaction and work motivation, the F value is 16.773 and the significance coefficient is 0.000 (p <0.01), meaning that the variables of job satisfaction and work motivation have a significant influence on work loyalty. The R value on job satisfaction and work motivation of 0.507 indicates a positive relationship direction and a strong relationship. The R square value of job satisfaction and work motivation of 0.257 means that job satisfaction and work motivation together affect work loyalty by 25.7%, the remaining 74.3% is influenced by other factors.

These results indicate that the hypothesis that states that there is an influence of job satisfaction and work motivation on work loyalty in outsourcing employees is accepted. This means that the satisfaction and motivation in working felt by outsourcing employees can foster their work loyalty in their workplace. The results of this study are in line with research conducted by Husni., Musnadi., And Faisal (2018) which states that job satisfaction and work motivation owned by prison employees in Aceh Province have an effect on the emergence of employee work loyalty. In addition, another study conducted by Citra and Fahmi (2019) also stated that job satisfaction and work motivation together have an influence of 73.9%, while the remaining 26.1% of work loyalty is influenced by other variables.

Employee loyalty is a positive employee attitude towards the company where they work. Employees with a high level of loyalty can work not only for themselves but also for the benefit of the company. Therefore, the role and duties of a leader in acting and making decisions are very influential, so that they can be a benchmark for actions and motivation for employees in all forms and positive activities that will later build enthusiasm and job satisfaction and even employee work loyalty itself (Citra and Fahmi, 2019).

Based on the results of the study, it can be concluded that job satisfaction influences work loyalty in outsourcing employees by 54.3%, the rest, 45.7% is influenced by other factors outside the study. Furthermore, work motivation influences work loyalty in outsourcing employees by 47.1%, the rest, 52.9% is influenced by other factors outside the study. Thus, job satisfaction and work motivation influence work loyalty in outsourcing employees by 25.7%, the rest, 74.3% is influenced by other factors outside the study.

Based on the results of the study, the following suggestions can be submitted so that employees are expected to continue to reflect work loyalty in their workplaces such as in terms of obeying regulations, being responsible, dedicated and honest in working.

REFERENCES

Arianty, N., Bahagia, R., Lubis, AA, & Siswadi, Y. (2016). Human Resource Management. Medan: Perdana Penerbitan.

Asih, DB. (2018). Contribution of extrinsic work motivation and intrinsic work motivation to work loyalty. Thesis. Gunadarma University: Jakarta.

Basir Barthos. (2001). Human resource management: a macro approach. Jakarta: Bumi Aksara.

Citra. LM, & Fahmi. M. (2019). The influence of leadership, job satisfaction and work motivation on employee loyalty. Scientific journal of master of management. 2(2). 214-225.

Colquitt, J., LePine, J., & Wesson, M. (2012). Organizational Behavior: Improving Workplace Performance and Commitment (3rd Edition). New York: McGraw-Hill Education.

Elmuti. D., Grunewald. J., & Abebe. D.(2010). Consequences of outsourcing strategy on employee quality of work life, attitudes, and performance. Journal of business strategy. 27(2). 178-203.

Hasibuan, M.S.P. (2002). Human resource management. Jakarta: Bumi Aksara.

Husni., Musnadi. S., & Faisal. (2018). The influence of work environment, comfort and motivation on job satisfaction and its impact on employee loyalty in Aceh Province. Journal of Master of Management. 2(1). 88-98.

Jamil. R., & Naeem. H. (2013). The impact of external outsourcing recruitment process on employee commitment and loyalty: empirical evidence from Pakistan’s telecommunications sector. Journal of business and management. 8(2). 69-75.

Jamil. R., & Naeem. H. (2013). The impact of outsourcing external recruitment process on the employee commitment and loyalty: empirical evidence from the telecommunication sector of Pakistan. Journal of business and management. 8(2). 69-75.

Mathis, R. L., & Jackson, J. H. (2000). Human resource management 9th ed. Cincinnati: South -Western College Publishing.

Mathis, R.L., & Jackson, J.H. (2000). Human resource management 9th edition. Cincinnati: Southwest College Publishing.

Ni’mah. I., & Nasif. K. (2016). Analysis of outsourcing employee welfare from the perspective of PT Spirit Krida Indonesia employees. Journal of Islamic economics. 4 (2). 300-317.

Ni’mah. I., & Nasif. K. (2016). Analysis of outsourcing employee welfare from the perspective of PT Spirit Krida Indonesia employees. Journal of Islamic Economics. 4 (2). 300-317.

Pelletier, L.G., Rocchi, M.A., Vallerand, R.J., Deci, E.L., Ryan, R.M. (2013). Validation of the revised sport motivation scale (SMS-II). Journal Psychology of Sport and Exercise. 14 (1). 329-341

Pelletier, LG, Rocchi, MA, Vallerand, RJ, Deci, EL, Ryan, RM (2013). Validation of the revised sports motivation scale (SMS-II). Journal of Sport and Exercise Psychology. 14 (1). 329-341 Robbins, S. (2006). Organizational Behavior. Jakarta: PT. Indeks Grup Gramedia.

Robbins, S. (2006). Organizational behavior. Jakarta: PT. Indeks Grup Gramedia.

Smith, P. C., Kendall, L. M., & Hulin, C. L. (1969). Measurement of satisfaction in workandretirement. Chicago: Rand McNally.

Spector, P.E. (1985). Measurement of human service staff satisfaction: development of the Job satisfaction survey. American journal of community psychology. 13 (6). 693-713.

Spector, PE. (1985). Measuring human service staff satisfaction: development of a job satisfaction survey. American journal of community psychology. 13 (6). 693-713.

Susilowati, F., & Supriyadi, I. (2018). Work loyalty caused by job satisfaction in construction company employees. Orbith Journal. 14 (2). 97-103.

Susilowati, F., & Supriyadi, I. (2018). Work loyalty caused by job satisfaction in construction company employees. Orbit Journal. 14 (2). 97-103.

Suwondo, Candra. (2004). Outsourcing; Implementation in Indonesia. Jakarta: Gramedia.

Swadarma, I. P. S., & Netra, I. G. S. K. (2020). Compensation, work motivation, and work environment influence employee loyalty at Rame Café Jimbaran seafood. Management Journal. 9 (5). 1738-1757.

Thanos, C.A., Pangemanan, S.S., & Rumokoy, F.S. (2015) The effect of job satisfaction and employee motivation on employee loyalty (case study of PT Kimia Farma Apotek in Sam ratulangi, Manado). Jurnal ilmiah berkala. 15 (4), 313-321.

Umar, H. (2005). Research methods for business theses and dissertations. Jakarta: PT. Raja Grafindo Persada.

Wahyuningtyas, Safira., Utami, H.N. (2018). Analysis of differences in performance between outsourcing employees and permanent employees. Journal of business administration. 60 (3). 96-103.

Wibowo, J., & Sutanto, E.M. (2013). The influence of leader member exchange (LMX), work motivation and job satisfaction on employee loyalty in the sales department of CV. Pratama Jaya in Madiun. Agora Journal. 1 (3), 1-9.

All G20 Finance Ministers and Central Bank Governors agreed to paragraphs 1, 4, and paragraphs 6 to 26 along with Annexes 1 and 2.

We, the Finance Ministers and Central Bank Governors of G20 countries, met on 17-18 July 2023, in Gandhinagar, India. Under the Indian Presidency’s theme of “One Earth, One Family, One Future”, we pledge to prioritize the well-being of our people and the planet and reaffirm our commitment to enhancing international economic cooperation, strengthening global development for all and steering the global economy towards strong, sustainable, balanced, and inclusive growth (SSBIG).

12Since February 2022, we have also witnessed the war in Ukraine further adversely impact the global economy. There was a discussion on the issue. We reiterated our national positions as expressed in other fora, including the UN Security Council and the UN General Assembly, which, in Resolution No. ES- 11/1 dated 2 March 2022, as adopted by majority vote (141 votes for, 5 against, 35 abstentions, 12 absent), deplores in the strongest terms the aggression by the Russian Federation against Ukraine and demands its complete and unconditional withdrawal from the territory of Ukraine. Most members strongly condemned the war in Ukraine and stressed that it is causing immense human suffering and exacerbating existing fragilities in the global economy constraining growth, increasing inflation, disrupting supply chains, heightening energy and food insecurity, and elevating financial stability risks. There were other views and different assessments of the situation and sanctions. Recognising that the G20 is not the forum to resolve security issues, we acknowledge that security issues can have significant consequences for the global economy.

It is essential to uphold international law and the multilateral system that safeguards peace and stability. This includes defending all the Purposes and Principles enshrined in the Charter of the United Nations and adhering to international humanitarian law, including the protection of civilians and infrastructure in armed conflicts. The use or threat of use of nuclear weapons is inadmissible. The peaceful resolution of conflicts, efforts to address crises, as well as diplomacy and dialogue are vital. Today’s era must not be of war.

1 China stated that the G20 FMCBG meeting is not the right forum to discuss geopolitical issues.

2 Russia dissociated itself from the status of this document as a common outcome because of references in paragraphs 2, 3 and 5.

Global economic growth is below its long-run average and remains uneven. The uncertainty around the outlook remains high. With notable tightening in global financial conditions, which could worsen debt vulnerabilities, persistent inflation and geoeconomic tensions, the balance of risks remains tilted to the downside. We, therefore, reiterate the need for well-calibrated monetary, fiscal, financial, and structural policies to promote growth, reduce inequalities and maintain macroeconomic and financial stability. We will continue to enhance macro policy cooperation and support the progress towards the 2030 Agenda for Sustainable Development. We reaffirm that achieving SSBIG will require policymakers to stay agile and flexible in their policy response, as evidenced during the recent banking turbulence in a few advanced economies where expeditious action by relevant authorities helped to maintain financial stability and manage spillovers. We welcome the initial steps taken by the Financial Stability Board (FSB), Standard Setting Bodies (SSBs) and in certain jurisdictions to examine what lessons can be learned from this recent banking turbulence and encourage them to advance their ongoing work. We will use macroprudential policies, where required, to safeguard against downside risks. Central banks remain strongly committed to achieving price stability in line with their respective mandates. They will ensure that inflation expectations remain well anchored and will clearly communicate policy stances to help limit negative cross-country spillovers. Central bank independence is crucial to maintaining policy credibility. We will prioritise temporary and targeted fiscal measures to protect the poor and the most vulnerable, while maintaining medium-term fiscal sustainability. We will ensure the coherence of the overall monetary and fiscal stances. We recognise the importance of supply-side policies, especially policies that increase labour supply and enhance productivity to boost growth and alleviate price pressures. We reaffirm our April 2021 exchange rate commitments. We also reaffirm the importance of the rules-based, non-discriminatory, fair, open, inclusive, equitable, sustainable and transparent multilateral trading system with the World Trade Organization (WTO) at its core in restoring growth and job creation and reiterate our commitment to fight protectionism and encourage concerted efforts for reform of the WTO.

While global food and energy prices have fallen from their peak levels, the potential for high levels of volatility in food and energy markets remains, given the uncertainties in the global economy. In this context, we welcome the G20 Report on Macroeconomic Impacts of Food and Energy Insecurity and their Implications for the Global Economy, informed by policy experiences shared by members and supported by analysis from the International Monetary Fund (IMF), World Bank Group (WBG), International Energy Agency (IEA) and Food and Agriculture Organisation (FAO) and take note of its voluntary and non-binding policy learnings. We look forward to an ambitious replenishment of the International Fund for Agricultural Development (IFAD) resources at the end of the year by IFAD members, to support IFAD’s fight against food insecurity.

We also take note of the discussions on assessing macroeconomic risks to SSBIG, including those stemming from climate change and various transition policies considering country-specific circumstances and different levels of development. The macroeconomic costs of the physical impacts of climate change are significant at an aggregate level and the cost of inaction substantially outweighs that of orderly and just climate transitions. We recognise the importance of international dialogue and cooperation, including in the areas of finance and technology, and timely policy action consistent with country- specific circumstances. It is also critical to assess and account for the short, medium and long-term macroeconomic impact of both the physical impact of climate change and transition policies, including on growth, inflation, and unemployment. We endorse the G20 Report on Macroeconomic Risks Stemming from Climate Change and Transition Pathways that presents an evidence-based assessment informed by policy experiences shared by members and technical inputs from the IMF, IEA, and the Network of Central Banks and Supervisors for Greening the Financial System (NGFS). Building on analysis in this Report, we will consider further work on the macroeconomic implications, as appropriate, particularly as relevant for fiscal and monetary policies, drawing on the inputs from a diverse set of stakeholders.

We remain committed to pursuing ambitious efforts to evolve and strengthen Multilateral Development Banks (MDBs) to address the global challenges of the 21st century with a continued focus on addressing the development needs of low- and middle-income countries.

Following up on the mandate from our Leaders in Bali in November 2022 and based on the updates from MDBs in Spring 2023, a G20 Roadmap for Implementing the Recommendations of the G20 Independent Review of MDBs Capital Adequacy Frameworks (CAFs) has been developed. We endorse this Roadmap and call for its ambitious implementation, within MDBs’ own governance frameworks while safeguarding their long-term financial sustainability, robust credit ratings and preferred creditor status. We also call for a regular review of the progress of implementation on a rolling basis including through engaging with MDBs, subject experts and shareholders. We commend the MDBs for their progress in implementing the CAF recommendations, especially with respect to adapting definitions of risk appetite and financial innovation. At the same time, we emphasise the need to give an additional push to CAF implementation. We appreciate the ongoing collaboration among MDBs on the timely release of Global Emerging Markets (GEMs) data and the launch of GEMs 2.0 as a stand-alone entity by early 2024. Going forward, we also encourage MDBs to collaborate in areas such as hybrid capital, callable capital, and guarantees. We appreciate the enhanced dialogue between the MDBs, Credit Rating Agencies and shareholders and encourage continued transparency in the exchange of information and rating methodologies. We take note that initial CAF measures, including those under implementation and consideration, could potentially yield additional lending headroom of approximately USD 200 billion over the next decade, as estimated in the G20 CAF Roadmap. While these are encouraging first steps, we will need continued and further impetus on CAF implementation.

Furthermore, we reiterate our call for the MDBs to undertake comprehensive efforts to evolve their vision, incentive structures, operational approaches and financial capacities so that they are better equipped to maximize their impact in addressing a wide range of global challenges, while being consistent with their mandate and commitment to accelerate progress towards Sustainable Development Goals (SDGs). Recognising the urgent need to strengthen and evolve the MDB ecosystem for the 21st century, we appreciate the efforts of the G20 Independent Expert Group on Strengthening MDBs in preparing Volume 1 of the Report, and we will examine it in conjunction with Volume 2 expected in October 2023. We take note of Volume 1’s recommendations and the MDBs may choose to discuss these recommendations as relevant and appropriate, within their governance frameworks, in due course, with a view to enhancing the effectiveness of MDBs. We look forward to a High-Level Seminar, on the sidelines of the Fourth FMCBG meeting in October 2023 on strengthening the financial capacity of MDBs. We encourage MDBs to update the International Financial Architecture Working Group (IFA WG) on their evolution efforts to better address global challenges. We welcome the March 2023 Report on Evolution of the World Bank Group and call on the World Bank to advance the implementation of the agreed actions and continue to develop further proposals that can contribute to significant progress of the Bank’s evolution exercise by the IMF/WBG 2023 Annual Meetings in Marrakech. Recognising other multilateral efforts in this area, we take note of the Summit for a New Global Financing Pact. We also look forward to an ambitious IDA21 replenishment. We acknowledge the concluding report on the 2020 Shareholding Review of the International Bank for Reconstruction and Development (IBRD) and look forward to the 2025 Shareholding Review.

We reiterate our commitment to a strong, quota-based, and adequately resourced IMF at the centre of the global financial safety net. We remain committed to revisiting the adequacy of quotas and will continue the process of IMF governance reform under the 16th General Review of Quotas (GRQ), including a new quota formula as a guide, and ensure the primary role of quotas in IMF resources, to be concluded by December 15, 2023. In this context, we support at least maintaining the IMF’s current resource envelope. We welcome the landmark achievement of the global ambition of USD 100 billion of voluntary contributions (in SDRs or equivalent) and USD 2.6 billion of grants in pledges for countries most in need and call for the swift delivery of pending pledges. We welcome the progress achieved under the Resilience and Sustainability Trust (RST) and Poverty Reduction and Growth Trust (PRGT) with pledges for the RST amounting to about USD 45.5 billion and for the PRGT to about USD 24.2 billion in loan resources and nearly USD 1.9 billion in subsidy resources, respectively, through the voluntary channelling of Special Drawing Rights (SDRs) or equivalent contributions. We call for further voluntary subsidy and loan pledges to the PRGT by the IMF/WBG 2023 Annual Meetings in Marrakech to meet the first stage PRGT fundraising needs. We look forward to the IMF delivering a preliminary analysis, by the 2023 IMF/WBG Annual Meetings, of the range of options to put the PRGT on a sustainable footing with a view to meeting the growing needs of low-income countries in the coming years. The G20 reiterates its continued support to Africa, including through the G20 Compact with Africa. We will continue to monitor progress on channelling SDRs or equivalent contributions from countries with strong external positions and look forward to the IMF Ex-Post Report on the use of SDRs in September. We will continue to monitor the effectiveness of RST supported programs and look forward to interim review scheduled for April 2024. We look forward to further progress on the exploration of viable options for channelling SDRs through MDBs, while respecting relevant legal frameworks and the need to preserve the reserve asset character and status of SDRs. We look forward to the review of precautionary arrangements (FCL, PLL and SLL) and take note of the discussions held on the IMF surcharge policy.

We welcome discussions on the potential macro-financial implications arising from the introduction and adoption of Central Bank Digital Currencies (CBDCs), notably on cross-border payments as well as on the international monetary and financial system. We welcome the BIS Innovation Hub (BISIH) Report on Lessons Learnt on CBDCs and look forward to the IMF Report on Potential macro-financial implications of widespread adoption of CBDCs to advance the discussion on this issue. We also look forward to continued discussions on the implementation of international frameworks for the use of different tools in addressing capital flow volatility based on the policy updates by the IMF, the OECD, and the BIS while being mindful of their original purpose. We reiterate our commitment to promote sustainable capital flows. To this effect, we note the OECD’s Report on Towards Orderly Green Transition – Investment Requirements and Managing Risks to Capital Flows.

We re-emphasise the importance of addressing debt vulnerabilities in low and middle-income countries in an effective, comprehensive and systematic manner. We continue to stand by all the commitments made in the Common Framework for Debt Treatments beyond the DSSI, including those in the second and final paragraphs, as agreed on November 13, 2020, and step up the implementation of the Common Framework in a predictable, timely, orderly and coordinated manner. To this end, we ask the G20 International Financial Architecture Working Group (IFA WG) to continue discussing policy-related issues linked to implementation of the Common Framework and make appropriate recommendations. We welcome the recent agreement between the Government of Zambia and official creditor committee on a debt treatment and look forward to a swift resolution. We welcome the formation of an official creditor committee for Ghana and look forward to an agreement on a debt treatment as soon as possible. We also call for a swift conclusion of the debt treatment for Ethiopia. Beyond the Common Framework, we welcome all efforts for timely resolution of the debt situation of Sri Lanka, including the formation of the official creditor committee, and we call for the resolution as soon as possible. Noting the work in developing the G20 Note on the Global Debt Landscape in a fair and comprehensive manner, we ask the G20 IFA WG to continue the development expeditiously. We encourage the efforts of the Global Sovereign Debt Roundtable (GSDR) participants to strengthen communication and foster a common understanding among key stakeholders, both within and outside the Common Framework, for facilitating effective debt treatments.

We welcome joint efforts by all stakeholders, including private creditors, to continue working towards enhancing debt transparency. We note the results of the voluntary stocktaking exercise of data sharing with International Financial Institutions. We welcome the efforts of private sector lenders who have already contributed data to the joint Institute of International Finance (IIF)/OECD Data Repository Portal and continue to encourage others to also contribute on a voluntary basis.

We emphasise the need for enhanced mobilisation of finances and efficient use of existing resources in our efforts to make the cities of tomorrow inclusive, resilient, and sustainable. To this effect, we endorse the G20 Principles for Financing Cities of Tomorrow, which are voluntary and non-binding in nature and the G20/OECD Report on Financing Cities of Tomorrow, which provides a financing strategy as well as presents a compendium of innovative urban planning and financing models. We encourage stakeholders, including the Development Financial Institutions and the MDBs, to explore the potential of drawing upon these principles in their planning and financing of urban infrastructure wherever applicable and share experiences from early pilot cases. We note the progress in outlining the enablers of inclusive cities. We also note the customisable G20/ADB Framework on Capacity Building of Urban Administration to guide local governments in assessing and enhancing their overall institutional capacity for the effective delivery of public services. We note the ongoing pilot application of the voluntary and non-binding Quality Infrastructure Investment (QII) Indicators and look forward to further discussion on their application considering the country circumstances. We thank the Global Infrastructure Hub for supporting the G20’s multi-year infrastructure agenda since 2014. We note that the GIH Board and shareholders are currently engaged in exploring a way to best sustain the value created so far. We look forward to the outcome report of the 2023 Infrastructure Investors Dialogue focused on integrating the private sector perspective in designing policies for financing cities of tomorrow.

We continue to reaffirm our steadfast commitment to strengthening the full and effective implementation of the United Nations Framework Convention on Climate Change (UNFCCC) and the Paris Agreement. We recall and reaffirm the commitment made by developed countries to the goal of mobilising jointly USD 100 billion climate finance per year by 2020, and annually through 2025, to address the needs of developing countries, in the context of meaningful mitigation action and transparency in implementation. Developed country- contributors expect this goal to be met for the first time in 2023. In this context, we also support continued deliberations on an ambitious new collective quantified goal of climate finance from a floor of USD 100 billion per year to support developing countries, that helps in fulfilling the objective of the UNFCCC and implementation of the Paris Agreement.

We welcome the Sustainable Finance Working Group (SFWG) recommendations on the mechanisms to support the timely and adequate mobilisation of resources for climate finance, while ensuring support for transition activities in line with country circumstances. We also recognise the significant role of public finance, as an important enabler of climate actions such as leveraging much-needed private finance through blended financial instruments, mechanisms and risk-sharing facilities, to address both adaptation and mitigation efforts in a balanced manner for reaching the ambitious Nationally Determined Contributions (NDCs), carbon neutrality and net-zero considering different national circumstances. We welcome the recommendations for scaling up blended finance and risk-sharing facilities, including the enhanced role of MDBs in mobilizing climate finance. We underscore the importance of maximizing the effect of concessional resources, such as those of the multilateral climate funds to support developing countries’ implementation of the Paris Agreement and look forward to an ambitious replenishment of the Green Climate Fund (GCF) this year. Recognizing the importance of supporting the commercialization of early-stage technologies that avoid, abate and remove greenhouse gas emissions and facilitate adaptation, we note the recommendations on financial solutions, policies, and incentives to encourage greater private flows for the rapid development, demonstration, and deployment of green and low-carbon technologies. We reiterate the importance of a policy mix consisting of fiscal, market and regulatory mechanisms including, as appropriate, the use of carbon pricing and non-pricing mechanisms and incentives, toward carbon neutrality and net zero. We look forward to the early finalisation of the Compendium comprising the discussions on Non-Pricing Policy Levers to Support Sustainable Investment.

We reiterate our commitment to take action to scale up sustainable finance. In line with the G20 Sustainable Finance Roadmap, we welcome the analytical framework for SDG-aligned finance, and voluntary recommendations for scaling-up adoption of social impact investment instruments and improving nature-related data and reporting, informed by the stocktaking analyses, considering country circumstances. We encourage all relevant stakeholders to consider these recommendations in their actions and support for the 2030 Agenda.

We endorse the multi-year G20 Technical Assistance Action Plan (TAAP) and the voluntary recommendations made to overcome data-related barriers to climate investments. We encourage the implementation of TAAP by relevant jurisdictions and stakeholders in line with the national circumstances. We look forward to reporting on the progress made by members, international organisations, networks and initiatives in the implementation of the G20 Sustainable Finance Roadmap, which is voluntary and flexible in nature, and call for further efforts to advance the Roadmap’s recommended actions that will scale up sustainable finance, including among others the implementation of the Transition Finance Framework. We look forward to the finalisation of the 2023 G20 Sustainable Finance Report, including a review of the implementation of the G20 Sustainable Finance Roadmap. We welcome finalization of the sustainability and climate-related disclosure standards published by the International Sustainability Standards Board (ISSB) in June 2023, which provide the mechanisms that address proportionality and promote interoperability. It is important that flexibility, to take into account country- specific circumstances, is preserved in the implementation of those standards. When put into practice as above, those standards will help to support globally comparable and reliable disclosures.

We remain committed to strengthening the global health architecture for pandemic prevention, preparedness and response (PPR) through enhanced collaboration between Finance and Health Ministries under the Joint Finance and Health Task Force (JFHTF). Under the JFHTF, we welcome the participation of invited key regional organisations in the Task Force meetings as they enhance the voice of low-income countries. We welcome the discussion on the Framework on Economic Vulnerabilities and Risks (FEVR) and the initial Report for Economic Vulnerabilities and Risks arising from pandemics, created through collaboration between World Health Organisation (WHO), World Bank, IMF, and European Investment Bank (EIB). We call on the Task Force to continue refining this Framework over its multi-year work plan in order to regularly assess economic vulnerabilities and risks due to evolving pandemic threats, taking into account country-specific circumstances. We welcome the Report on Best Practices from Finance Health Institutional Arrangements during Covid-19 that will contribute towards joint finance-health sector readiness to support our response to future pandemics. We welcome the Report on Mapping Pandemic Response Financing Options and Gaps developed by the WHO and World Bank and look forward to further deliberations on how financing mechanisms could be optimized, better coordinated and, when necessary, suitably enhanced, to deploy the necessary financing quickly and efficiently, duly considering discussions in other global forums. The analysis provided by these three reports will offer important inputs for discussion in the Joint Finance-Health Ministerial Meeting in August on global response to the next pandemic threat. We welcome the conclusion of the call for proposals by the Pandemic Fund and look forward to the first round of funding in the coming months.

We reaffirm our commitment to continue cooperation towards a globally fair, sustainable and modern international tax system appropriate to the needs of the 21st century. We welcome the delivery of a text of a Multilateral Convention (MLC) on Amount A, significant progress of work on Amount B and the completion of the work on the development of the Subject to Tax Rule (STTR) and its implementation framework as set out in the July 2023 Outcome Statement of the OECD/G20 Inclusive Framework on BEPS (Inclusive Framework). We call on the Inclusive Framework to swiftly resolve the few pending issues relating to the MLC with a view to prepare the MLC for signature in the second half of 2023 and complete the work on Amount B by end of 2023. We welcome the steps taken by various countries to implement the Global Anti-Base Erosion (GloBE) Rules as a common approach. We recognise the need for coordinated efforts towards capacity building to implement the two-pillar international tax package effectively and in particular, welcome a plan for additional support and technical assistance for developing countries. We welcome the launch of the pilot programme of the South Asia Academy in India for tax and financial crime investigation in collaboration with OECD. We note the 2023 update of the G20/OECD Roadmap on Developing Countries and International Taxation. We note the Update on the Implementation of the 2021 Strategy on Unleashing the Potential of Automatic Exchange of Information for Developing Countries by the Global Forum on Transparency and Exchange of Information for Tax Purposes (“Global Forum”). We call for the swift implementation of the Crypto-Asset Reporting Framework (“CARF”) and amendments to the CRS. We ask the Global Forum to identify an appropriate and coordinated timeline to commence exchanges by relevant jurisdictions, noting the aspiration of a significant number of these jurisdictions to start CARF exchanges by 2027, and to report to our future meetings on the progress of its work. We note the OECD Report on Enhancing International Tax Transparency on Real Estate and the Global Forum Report on Facilitating the Use of Tax-Treaty-Exchanged Information for Non-Tax Purposes. We note the discussions held at the G20 High-Level Tax Symposium on Combatting Tax Evasion, Corruption and Money Laundering.

We continue to closely monitor the risks of the fast-paced developments in the crypto-asset ecosystem. We endorse the Financial Stability Board’s (FSB’s) high-level recommendations for the regulation, supervision and oversight of crypto-assets activities and markets and of global stablecoin arrangements. We ask the FSB and standard-setting bodies (SSBs) to promote the effective and timely implementation of these recommendations in a consistent manner globally to avoid regulatory arbitrage. We welcome the shared FSB and SSBs workplan for crypto assets. We look forward to receiving the IMF-FSB Synthesis Paper, including a Roadmap, before the Leaders’ Summit in September 2023, to support a coordinated and comprehensive policy and regulatory framework taking into account the full range of risks, and risks specific to the emerging market and developing economies (EMDEs) and ongoing global implementation of FATF standards to address money laundering and terrorism financing risks. In this context, we note the Presidency Note as an important input for the Synthesis Paper. We also welcome the BIS Report on The Crypto Ecosystem: Key Elements and Risks.

We continue to strongly support the work of the FSB and SSBs to address vulnerabilities and enhance the resilience of non-bank financial intermediation (NBFI) from a systemic perspective while monitoring evolving developments in NBFI. We welcome the FSB’s consultation report on revisions to the FSB 2017 recommendations on addressing liquidity mismatch in open-ended funds, and we support work to promote implementation of the FSB money market fund proposals, enhance margining practices, and address vulnerabilities from non-bank leverage. We welcome the FSB’s recommendations to achieve greater convergence in cyber incident reporting, updates to the Cyber Lexicon and Concept Note for a Format for Incident Reporting Exchange (FIRE). We look forward to the FSB’s work to identify the reporting needs and the prerequisites for and feasibility of the development of FIRE, and we ask the FSB to develop an action plan with appropriate timelines.

We welcome the FSB’s consultation Report on Enhancing Third-party Risk Management and Oversight. We expect the toolkit to support efforts in enhancing the operational resilience of financial institutions, addressing the challenges arising from their growing reliance on critical third-party service providers including BigTechs and FinTechs, as well as reducing fragmentation in regulatory and supervisory approaches across jurisdictions and in different areas of the financial services sector. We reaffirm our commitment to the effective implementation of the prioritised actions for the next phase of the G20 Roadmap for Enhancing Cross-border Payments and welcome the initiatives undertaken by SSBs and international organisations in this direction. To that end, we look forward to the FSB’s progress report in October on the implementation of this roadmap. We look forward to the G20 TechSprint 2023, a joint initiative with the BIS Innovation Hub, which will promote innovative solutions aimed at improving cross-border payments. We welcome the annual progress Report on the FSB’s Roadmap for Addressing Financial Risks from Climate Change. We endorse the revised G20/OECD Principles of Corporate Governance with the aim to strengthen policy and regulatory frameworks for corporate governance that support sustainability and access to finance from capital markets, which in turn can contribute to the resilience of the broader economy.

We welcome the progress made by the Global Partnership for Financial Inclusion (GPFI) towards the completion of the deliverables under the G20 2020 Financial Inclusion Action Plan (FIAP). We welcome the 2023 Update to Leaders on Progress towards the G20 Remittance Target and endorse the Regulatory Toolkit for Enhanced Digital Financial Inclusion of Micro, Small and Medium Enterprises (MSMEs). We endorse the voluntary and non-binding G20 Policy Recommendations for Advancing Financial Inclusion and Productivity Gains through Digital Public Infrastructure. We take note of the significant role of digital public infrastructure in helping to advance financial inclusion in support of inclusive growth and sustainable development. We also encourage the continuous development and responsible use of technological innovations including innovative payment systems, to achieve financial inclusion of the last mile and progress towards reducing the cost of remittances in line with the G20 Leaders’ directions. We also support continuous efforts to strengthen digital financial literacy and consumer protection. We endorse the G20 2023 FIAP, which provides an action-oriented and forward-looking roadmap for rapidly accelerating the financial inclusion of individuals and MSMEs, particularly vulnerable and underserved groups in the G20 countries and beyond. We also endorse the 2023 Updated GPFI Terms of Reference.

We recognise the importance of delivering on the strategic priorities of the Financial Action Task Force (FATF) and FATF Style Regional Bodies. We commit to supporting their increasing resource needs and encourage others to do the same, including for the next round of mutual evaluations. We remain committed to the timely and global implementation of the revised FATF Standards on the transparency of beneficial ownership of legal persons and legal arrangements to make it more difficult for criminals to hide and launder ill- gotten gains. We welcome the ongoing work of the FATF to enhance global efforts to recover criminal proceeds, in particular, the progress made by the FATF towards revising its standards on asset recovery and reinforcing global asset recovery networks. We reiterate the importance of countries developing and implementing effective regulatory and supervisory frameworks to mitigate risks associated with virtual assets in line with FATF Standards especially for terrorism financing, money laundering, and proliferation financing risks. In this regard, we support the FATF’s initiative to accelerate the global implementation of its standards, including the “travel rule”, and its work on risks of emerging technologies and innovations, including decentralised finance (DeFi) arrangements and peer-to-peer transactions. We look forward to the completion of FATF’s work on the use of crowdfunding for terrorism financing and on money laundering related to cyber-enabled fraud.

With a vision reminiscent of Mahatma Gandhi’s teachings, we, the Finance Ministers and Central Bank Governors of G20 countries, envisage a future in which every nation thrives, prosperity is widely shared, and the well-being of humanity and the planet are harmoniously intertwined.

Annex I: Issues for further work

This Annex lists the deliverables from various G20 Finance Track workstreams following the July FMCBG meeting.

Framework Working Group

G20 IMF Report on Strong, Sustainable, Balanced and Inclusive Growth, October 2023, in the context of increasing vulnerabilities associated with macroeconomic instabilities and financial globalisation.

International Financial Architecture Working Group

· Volume 2 of the Report of G20 Expert Group on Strengthening MDBs

Regular review of the progress of implementation of CAF recommendations on a rolling basis including through engaging with MDBs, subject experts and shareholders

· Updates from IMF on the progress of the 16th General Review of Quotas

Update from the IMF on the ex-post assessment of 2021 SDR allocation

Continued exploration of opportunities for a “User manual” for the Common

Framework presenting the experience of the first cases.

G20 IFA WG to continue developing expeditiously the G20 Note on the Global Debt Landscape in a fair and comprehensive manner.

IFA WG to continue discussing policy-related issues linked to implementation of the Common Framework and make appropriate recommendations

Technical workshops to be held under the ambit of GSDR, such as the one on Comparability of Treatment (CoT).

Improvements to sovereign debt restructuring by continuing the discussion on some specific debt instruments, including potential best practices for LICs on collateralised financing practices, exploring ways to increase private sector involvement, in particular regarding the restructuring of syndicated loans, collective action clauses, assessing the benefits and complications of state- contingent debt instruments (SCDI), and climate-resilient debt clauses in international sovereign bonds and in official bilateral lending.

IMF Report on the potential macro-financial implication of widespread adoption of CBDCs, in September 2023.

Infrastructure

Continuation of the InfraTracker 2.0 to track planned infrastructure investments across G20 member economies using publicly available sources and transition it to an online tool.

Compilation of the scope and taxonomies related to infrastructure across G-20 economies and International Organisations.

Sustainable Finance Working Group

Monitoring and reporting of progress on G20 Sustainable Finance Roadmap on the SFWG online dashboard.

Finalisation of the 2023 G20 Sustainable Finance Report.

Compendium of case studies for financing SDGs.

International Taxation

A Handbook by the OECD on Pillar Two to facilitate implementation through a common approach, especially to assist capacity-constrained jurisdictions and present the Handbook by October 2023.

Financial Sector Issues

A joint synthesis paper by the IMF and the FSB integrating the macroeconomic and regulatory perspectives of crypto assets to be submitted in September 2023.

An interim report by the BIS Committee on Payments and Market Infrastructures (CPMI) on Fast Payment Systems (FPS) interlinking governance, risk management and oversight considerations; and the final report on ISO 20022 harmonisation requirements for cross-border payments in October 2023.

FSB to provide a report on the financial stability implications of leverage in NBFI in September 2023.

FSB to provide an overall progress report on enhancing the resilience of NBFI in September 2023.

FSB to provide its Annual Report on Promoting Global Financial Stability in October 2023.

FSB to report in October 2023 its progress on the implementation of the G20 Roadmap for Enhancing Cross-Border Payments.

FSB, in coordination with the ISSB and IOSCO, to prepare a report on the progress of jurisdictions and firms on climate-related financial disclosures by October 2023.

Global Partnership for Financial Inclusion

GPFI will continue work to complete the Second Update of National Remittance Plans and present a case-study on the impact of digital remittances in reducing the cost of remittances.

GPFI will report on progress in implementing the G20 GPFI High-Level Principles on Digital Financial Inclusion.

GPFI to work on SME best practices and innovative instruments to overcome common constraints in SME financing based on GPFI SME living database.

Annex 2: Reports and Documents received

G20 Report on Macroeconomic Impacts of Food and Energy Insecurity and their implications for the global economy

G20 Report on Macroeconomic risks stemming from climate change and transition pathways

G20 Roadmap for implementing the recommendations of the G20 Independent Review of MDBs Capital Adequacy Frameworks (CAFs)

Volume 1 of the G20 Expert Group on Strengthening MDBs

BIS Innovation Hub (BISIH) Report on “Lessons learnt on CBDCs”

OECD’s report on “Towards Orderly Green Transition – Investment Requirements and Managing Risks to Capital Flows

G20 note on the total global ambition of USD 100bn of voluntary contributions for countries most in need

G20 Principles for Financing Cities of Tomorrow: inclusive, resilient and sustainable

G20/OECD Report on Financing Cities of Tomorrow

G20/ADB Framework on Capacity Building of Urban Administration

G20 Sustainable Finance Working Group Deliverables

Framework on Economic Vulnerabilities and Risks (FEVR) and the initial Report for economic vulnerabilities and risks arising from pandemics

Report on Best Practices from Finance Health Institutional Arrangements during Covid-19

Report on Mapping Pandemic Response Financing Options and Gaps developed by the WHO and World Bank

G20/OECD Roadmap on Developing Countries and International Taxation Update 2023

OECD Report on ‘Enhancing International Tax Transparency on Real Estate’

Global Forum Report on ‘Facilitating the Use of Tax-Treaty-Exchanged Information for Non-Tax Purposes’

Global Forum Update on the implementation of the 2021 Strategy on Unleashing the Potential of Automatic Exchange of Information for Developing Countries

FSB Chair’s Letters to G20 Finance Ministers and Central Bank Governors, April and July 2023.

FSB’s global regulatory framework for crypto-asset activities: Umbrella public note to accompany final framework

FSB’s high-level recommendations for the regulation, supervision, and oversight of crypto-asset activities and markets

FSB’s high-level recommendations for the regulation, supervision, and oversight of global stablecoin arrangements

BIS Report on “The crypto ecosystem: key elements and risks”.

FSB Consultation report on addressing liquidity mismatch in open-ended funds-Revisions to the FSB 2017 policy recommendations

FSB Report on Enhancing Third-Party Risk Management and Oversight: A toolkit for financial institutions and financial authorities

FSB Roadmap for Addressing Financial Risks from Climate Change: 2023 Progress Report

FSB Recommendations to Achieve Greater Convergence in Cyber Incident Reporting: Final Report

FSB Concept Note on Format for Incident Reporting Exchange (FIRE) – A possible way forward

Revised G20/OECD Principles of Corporate Governance

G20 Policy Recommendations for Advancing Financial Inclusion and Productivity Gains through Digital Public Infrastructure

2023 Update to Leaders on Progress towards the G20 Remittance Target

Regulatory Toolkit for Enhanced Digital Financial Inclusion of Micro, Small and Medium Enterprises (MSMEs)

G20 2023 FIAP

2023 Updated GPFI Terms of Reference.

2023 GPFI Progress Report to G20 Leaders

G20 Financial Inclusion Action Plan Progress Report 2021-23

The environment plays a significant role to support life on earth. But there are some issues that are causing damages to life and the ecosystem of the earth. It is related to the not only environment but with everyone that lives on the planet. Besides, its main source is pollution, global warming, greenhouse gas, and many others. The everyday activities of human are constantly degrading the quality of the environment which ultimately results in the loss of survival condition from the earth.There are hundreds of issue that causing damage to the environment. But in this, we are going to discuss the main causes of environmental issues because they are very dangerous to life and the ecosystem.

Pollution – It is one of the main causes of an environmental issue because it poisons the air, water, soil, and noise. As we know that in the past few decades the numbers of industries have rapidly increased. Moreover, these industries discharge their untreated waste into the water bodies, on soil, and in air. Most of these wastes contain harmful and poisonous materials that spread very easily because of the movement of water bodies and wind. Greenhouse Gases – These are the gases which are responsible for the increase in the temperature of the earth surface. This gases directly relates to air pollution because of the pollution produced by the vehicle and factories which contains a toxic chemical that harms the life and environment of earth. Climate Changes – Due to environmental issue the climate is changing rapidly and things like smog, acid rains are getting common. Also, the number of natural calamities is also increasing and almost every year there is flood, famine, drought, landslides, earthquakes, and many more calamities are increasing.

Development recognises that social, economic and environmental issues are interconnected, and that decisions must incorporate each of these aspects if there are to be good decisions in the longer term.For sustainable development, accurate environment forecasts and warnings with effective information on pollution which are essential for planning and for ensuring safe and environmentally sound socio-economic activities should be made known.

Early times the Indian subcontinent appears to have provided an attractive habitat for human occupation. Toward the south it is effectively sheltered by wide expanses of ocean, which tended to isolate it culturally in ancient times, while to the north it is protected by the massive ranges of the Himalayas, which also sheltered it from the Arctic winds and the air currents of Central Asia. Only in the northwest and northeast is there easier access by land, and it was through those two sectors that most of the early contacts with the outside world took place.

Within the framework of hills and mountains represented by the Indo-Iranian borderlands on the west, the Indo-Myanmar borderlands in the east, and the Himalayas to the north, the subcontinent may in broadest terms be divided into two major divisions: in the north, the basins of the Indus and Ganges (Ganga) rivers (the Indo-Gangetic Plain) and, to the south, the block of Archean rocks that forms the Deccan plateau region. The expansive alluvial plain of the river basins provided the environment and focus for the rise of two great phases of city life: the civilization of the Indus valley, known as the Indus civilization, during the 3rd millennium BCE; and, during the 1st millennium BCE, that of the Ganges. To the south of this zone, and separating it from the peninsula proper, is a belt of hills and forests, running generally from west to east and to this day largely inhabited by tribal people. This belt has played mainly a negative role throughout Indian history in that it remained relatively thinly populated and did not form the focal point of any of the principal regional cultural developments of South Asia. However, it is traversed by various routes linking the more-attractive areas north and south of it. The Narmada (Narbada) River flows through this belt toward the west, mostly along the Vindhya Range, which has long been regarded as the symbolic boundary between northern and southern India.

India’s movement for Independence occurred in stages elicit by the inflexibility of the Britishers and in various instances, their violent responses to non-violent protests. It was understood that the British were controlling the resources of India and the lives of its people, and as far as this control was ended India could not be for Indians.