Globalization has many meaning depending on the circumstance and on the individual who is talking about. There is one of the term of Globalization is a process of the “reconfiguration of geography, so that social space is not entirely mapped in terms of territorial distance, territorial places and territorial borders.” The simple term of globalization refers to the integration of economies of the world through uninhibited trade and financial flows, as also through mutual exchange of technology and knowledge. Ideally, it also contains free inter country movement of labor.

Indian society drastically changes after urbanization and globalization. The economic policies has direct influence in forming the basic framework of the Indian economy. The government shaped administrative policies which aim to promote business opportunities in every country, generate employment and attract global investment. In which the Indian economy witnessed an impact on its culture and introduction to other societies and their norms brought various changes to the culture of this country as well. The developed countries have been trying to pursue developing countries to liberalize the trade and allow more flexibility in business policies to provide equal opportunities to multinational firms in their domestic market. The International Monetary Fund (IMF) and World Bank helped them in this endeavor. Liberalization began to hold its foot on barren lands of developing countries like India by means of reduction in excise duties on electronic goods in a fixed time Frame.

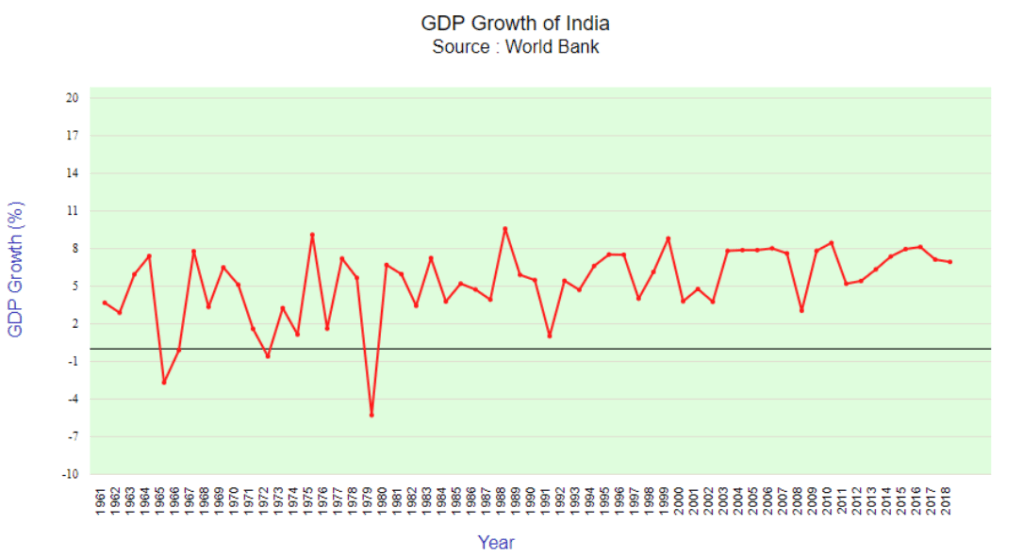

Globalization has several aspects and can be political, cultural, social, and economic, out of Financial integration is the most common aspect. India is one of the fastest-growing economies in the world and has been predicted to reach the top three in the next decade. India’s massive economic growth is largely due to globalization which was a transformation that didn’t occur until the 1990s. Since then, the country’s gross domestic product (GDP) has grown at an exponential rate.

Indian government did the same and liberalized the trade and investment due to the pressure from the World Trade Organization. Import duties were cut down phase-wise to allow MNC’s operate in India on an equal basis. As a result globalization has brought to India new technologies, new products and also the economic opportunities.

Despite bureaucracy, lack of infrastructure and an ambiguous policy framework that adversely impact MNCs operating in India, MNCs are looking at India in a big way, and are making huge investments to set up R&D centres in the country. India has made a lead over other growing economies for IT, business processing, and R&D investments. There have been both positive and negative impacts of globalisation on social and cultural values in India.

Economic Impact:

1. Greater Number of Jobs: The advent of foreign companies led to the growth in the economy which led to creating job opportunities. However, these jobs are concentrated in the various services sectors and led to rapid growth of the service sector creating problems for individuals with low levels of education. The last decade came to be known for its jobless growth as job creation was not proportionate to the level of economic growth.

2. More choice to consumers: Globalisation has led to having more choices in the consumer products market. There is a range of choices in selecting goods unlike the times where there were just a couple of manufacturers.

3. Higher Disposable Incomes: People in cities working in high paying jobs have greater income to spend on lifestyle goods. There’s been an increase in the demand for products like meat, egg, pulses, organic food as a result. It has also led to protein inflation.

Protein food inflation contributes a large part to the food inflation in India. It is evident from the rising prices of pulses and animal proteins in the form of eggs, milk and meat. With an improvement standard of living and rising income level, the food habits of people changed. People tend toward taking more protein intensive foods. This shift in dietary pattern, along with rising population results in an overwhelming demand for protein rich food, which the supply side could not meet. Thus resulting in a demand supply mismatch thereby, causing inflation.

In India, the Green Revolution and other technological advancements have primarily focused on enhancing cereals productivity and pulses and oilseeds have traditionally been neglected.

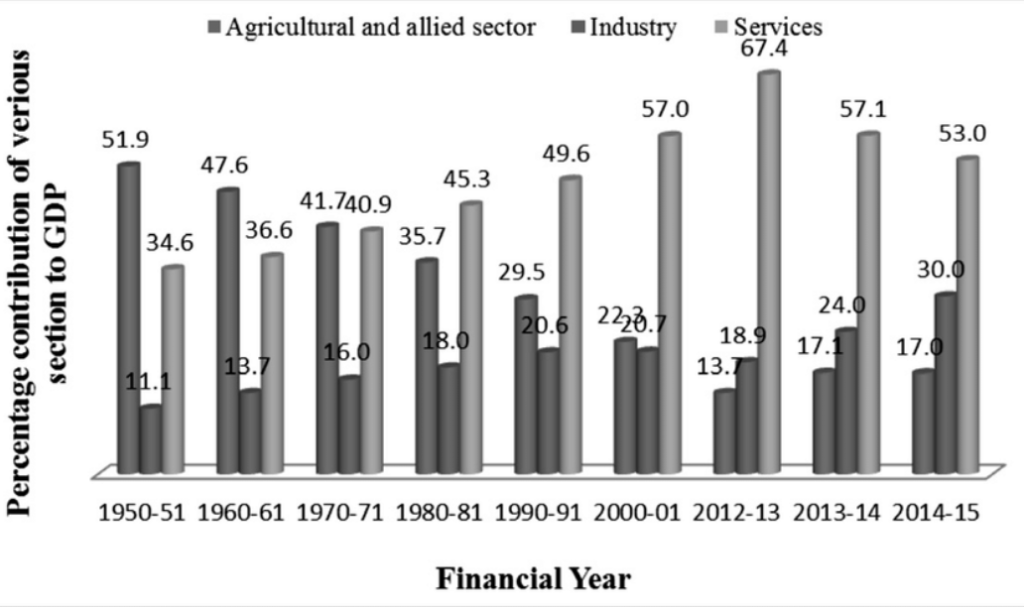

• Shrinking Agricultural Sector: Agriculture now contributes only about 15% to GDP. The international norms imposed by WTO and other multilateral organizations have reduced government support for agriculture. Greater integration of global commodities markets leads to constant fluctuation in prices.

• This has increased the vulnerability of Indian farmers. Farmers are also increasingly dependent on seeds and fertilisers sold by the MNCs.

Globalization does not have any positive impact on agriculture. On the contrary, it has few detrimental effects as the government is always willing to import food grains, sugar etc. Whenever there is a price increase of these commodities.

• Government never thinks to pay more to farmers so that they produce more food grains but resorts to imports. On the other hand, subsidies are declining so the cost of production is increasing. Even farms producing fertilizers have to suffer due to imports. There are also threats like introduction of GM crops, herbicide resistant crops etc.

• Increasing Health-Care costs: Greater interconnections of the world have also led to the increasing susceptibility to diseases. Whether it is the bird-flu virus or Ebola, the diseases have taken a global turn, spreading far and wide. This results in greater investment in the healthcare system to fight such diseases.

• Child Labor: Despite prohibition of child labors by the Indian constitution, over 60 to a 115 million children in India work. While most rural child workers are agricultural laborer’s, urban children work in manufacturing, processing, servicing and repairs. Globalization most directly exploits an estimated 300,000 Indian children who work in India’s hand-knotted carpet industry, which exports over $300 million worth of goods a year. The many effects of globalization of Indian society and has immense multiple aspects on Indian trade, finance, and cultural system. Globalization is associated with rapid changes and significant human societies. The movement of people from rural to urban areas has accelerated, and the growth of cities in the developing world especially is linked to substandard living for many.

Sources: https://www.clearias.com/effects-globalization-indian-society/

/is-it-multilevel-marketing-or-a-pyramid-scheme-2947159-FINAL-5f46e1d56e034223a43f045ed7b5ee23.jpg)

You must be logged in to post a comment.