Amid global pandemic accompanied by Russia-Ukraine crises and rising prices of fuels, the major economies across the globe are facing economic slowdown majorly in the form of peaked inflation, unstable government, industrial slowdown, low supplies and much more consequences. Some of the economies have slipped into crises, while some are struggling through the worst phase of slowdown. Industry experts have been showing aspersions that a global recession is just around the corner.

The recent survey by Bloomberg has attempted to gauge the percentage probabilities of various countries slipping into recession. The survey by Bloomberg said that risk of recession in a handful of Asian economies is rising as higher prices spur central banks to accelerate the pace of their interest rate hikes. Sri Lanka, which is in the midst of its worst economic crisis ever, has an 85% probability of falling into recession in the next year, up from a 33% chance in the previous survey by far the highest increase in the region. Economists see a 20% chance that China will enter recession, and a 25% likelihood that South Korea or Japan will enter one. Bloomberg economists also raised their expectations for a chance of recession in New Zealand, Taiwan, Australia and the Philippines to 33%, 20%, 20% and 8%, respectively. Central banks in those places have been raising interest rates to tame inflation.

India being one of the major and growing economy, also have been facing the consequences of global crises, particularly inflation. The survey report by Bloomberg for India is that it mentions that India has zero probability of slipping into recession. India literally has 0 percent chances of recession as against economic giants US and China which has 40 percent and 20 percent respectively. Although for India, surging domestic prices of key commodities is mainly on account of imported inflation, retail inflation based on consumer price index stood at 7.01%. In April, it had jumped to 8-year high of 7.79% have feared the economist about a probable recession but the case for India is much better compared to other economies.

India being the second biggest consumer of precious metals, tries to regulate the market for the precious metal. For this Prime Minister on July 29 laid the foundation of India International Bullion Exchange (IIBX), based at Gujarat International Finance Tec-City, or GIFT City in western Gujarat state.

India imported 1,069 tonnes of gold in 2021, up from 430 tonnes a year ago. Indian households own an estimated collective 25,000 tonnes of gold, which passes from one generation to the next. New Delhi has been trying to monetise these holding to reduce the imports. Gold is tightly regulated in India and currently only nominated banks and agencies approved by the central bank can import gold and sell to dealers and jewellers. The opening of the international bullion exchange is aimed to standardize the gold pricing in India. It further seeks to it easier for small bullion dealers and jewellers to trade.

Currently, there are nominated banks and agencies who have been approved by the central bank to conduct trade or import gold and sell it to dealers.

“IIBX with its technology-driven solutions, will facilitate transition of Indian bullion market towards a more organised structure by granting qualified jewellers a direct access to import gold directly through the exchange mechanism,” the exchange said in a statement.

The International Bullion Exchange shall be the Gateway for Bullion Imports into India, wherein all the bullion imports for domestic consumption shall be channelized through the exchange, as per a government’s notification.

The exchange ecosystem is expected to bring all the market participants at a common transparent platform for bullion trading and provide an efficient price discovery, assurance in the quality of gold, enable greater integration with other segments of financial markets and help establish India’s position as a dominant trading hub in the World.

How will the evolution of the web have an effect on Financial Services? This is a question that puts many financial institutions in peril but is it really something that will put banks out of business?

What is Web 3.0?

Web 3.0 is a new evolution phase that is coming into reality. The web as we know, is evolving into something more secure with more opportunities and various features. A lot of people don’t understand Web 3.0 and are scared of it. This will be a massive change on how we see the internet and how we will use it. It is going to be a decentralized platform and it will be individualized wherein you can customize your internet browsing experience.

The Royal Bank of Canada is utilizing millions of data points to train its own AI, resulting in fewer client calls and faster application delivery. Meanwhile, BNY Mellon, the world’s largest cross-border payments service provider, improved its fraud prediction accuracy by 20%. By researching real-time market data within nanoseconds, AI and high-performance computing (HPC) are combining to provide better and faster trading intelligence.

What does this mean for Financial Services?

Web 3.0 is transforming the finance sphere slowly into a decentralized place. Basically, you don’t need a financial institution governing your transaction or authorizing them. The transaction will only be initiated by you and reaches the receiver, in a matter of moments, without any middlemen. Using cryptocurrency, you can make transactions over blockchain that eliminates that bank server from between. Cryptos are digital assets that let users transact directly without a payment service provider in the intermediary, which means that they enable new forms of capital. Although Bitcoin remains comparatively low now, it still may provide effective money governance by preserving and protecting the data or memory of what our money represents. Then there is the unparalleled manipulation of fiat money. We can observe how central banks have significantly extended their balance sheets since the GFC and the ongoing pandemic COVID-19.

DeFi

DeFi is short for decentralized finance where there are no middlemen between you and the receiver. The transaction will be on the blockchain where the transaction time is reduced from time of hours/days, to moments that you can count on your hands. With DeFi, you can perform all transactions and services that are offered by traditional banks, without the bank in between. Now, you might wait for your transaction to be passed through because your bank should allow it and then it has to pass through the bank’s server.

DeFi uses cryptocurrency as the main currency because they are programmed using blockchain technology. There is a huge difference between CeFi and DeFi.

Effect on Financial Services

Undoubtedly, Web 3.0 has opened its doors for infinite opportunities and many FinTechs are utilizing them while traditional institutions are being left behind. These organizations are investing in their technology and its improvement in this rapidly changing market. These FinTechs’ major part of investment is into AI which are being programmed to understand the different problems faced by people and able to give out the solutions in a matter of seconds. This dependance on AIs is being constantly improved which are learning from their own errors and giving better and more efficient solutions. A survey by NVIDIA , according to it, nearly 83% of finance service professionals say that AI is essential for the companies’ success. It is also said that AI can improve company growth by 20%.

Conclusion

Web 3.0 is bringing so many opportunities while improving the present technology and organizations that are utilizing it will not be taking rest anytime soon. This technology is just going to become better and better. Every single day that we see this technology step up just shows that we are not done with technology, it can be better and more efficient and these companies are proving that to use everyday. Web 3.0 is showing more freedom of speech and thoughts than the present restricted web 2.0, decentralization is going to put back the control back in the hand of the User.

“Where there is life, there is growth

Where there is age, there is evolution.”

~Charles Darwin

Thank you so much for reading this article. I have added information from different websites and I thank them for their view on this topic. Do leave comments on different aspects of Web 3.0 that you think will change us.

The links to pages that helped me understand Web 3.0 better:

Inflation is a term we here very frequently in today’s world. Several economies of the world are now in the crunches of inflation. In this situation, let us read about inflation in detail.

What is inflation?

In economics, inflation is a general increase in prices of goods and services in an economy. When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation corresponds to a reduction in the purchasing power of money. The opposite of inflation is deflation, a sustained decrease in the general price level of goods and services. The common measure of inflation is the inflation rate, the annualized percentage change in a general price index. As prices do not all increase at the same rate, the consumer price index (CPI) is often used for this purpose.

Causes of inflation:

There were different schools of thought as to the causes of inflation. Most can be divided into two broad areas: quality theories of inflation and quantity theories of inflation.

Currently, the quantity theory of money is widely accepted as an accurate model of inflation in the long run. Consequently, there is now broad agreement among economists that in the long run, the inflation rate is essentially dependent on the growth rate of the money supply relative to the growth of the economy. However, in the short- and medium-term inflation may be affected by supply and demand pressures in the economy, and influenced by the relative elasticity of wages, prices and interest rates.

The quality theory of inflation rests on the expectation of a seller accepting currency to be able to exchange that currency at a later time for goods they desire as a buyer. The quantity theory of inflation rests on the quantity equation of money that relates the money supply, its velocity, and the nominal value of exchanges.

Measures of inflation

Consumers’ cost of living depends on the prices of many goods and services and the share of each in the household budget. To measure the average consumer’s cost of living, government agencies conduct household surveys to identify a basket of commonly purchased items and track over time the cost of purchasing this basket. The cost of this basket at a given time expressed relative to a base year is the consumer price index (CPI), and the percentage change in the CPI over a certain period is consumer price inflation, the most widely used measure of inflation.

Core consumer inflation focuses on the underlying and persistent trends in inflation by excluding prices set by the government and the more volatile prices of products, such as food and energy, most affected by seasonal factors or temporary supply conditions. Core inflation is also watched closely by policymakers. Calculation of an overall inflation rate—for a country, say, and not just for consumers—requires an index with broader coverage, such as the GDP deflator.

Types of inflation

Cost-Push Effect

Cost-push inflation is a result of the increase in prices working through the production process inputs. When additions to the supply of money and credit are channeled into a commodity or other asset markets and especially when this is accompanied by a negative economic shock to the supply of key commodities, costs for all kinds of intermediate goods rise.

Built-in Inflation

Built-in inflation is related to adaptive expectations, the idea that people expect current inflation rates to continue in the future. As the price of goods and services rises, workers and others come to expect that they will continue to rise in the future at a similar rate and demand more costs or wages to maintain their standard of living. Their increased wages result in a higher cost of goods and services, and this wage-price spiral continues as one factor induces the other and vice-versa.

Demand-Pull Effect

Demand-pull inflation occurs when an increase in the supply of money and credit stimulates overall demand for goods and services in an economy to increase more rapidly than the economy’s production capacity. This increases demand and leads to price rises.

RBI governor, Shaktikanth Das, on May 4 2022 revised the repo rates. On this context, let us look more about the credit control measures adopted by Reserve bank of India.

Reserve bank is the apex body to control the banking system in India. As we all know banks are the major link in money supply. Thus, RBI can control the money in the economy by controlling the banks. These policies are termed as monetary policy.

RBI could adopt either quantitative or qualitative methods.

Quantitative methods

Statutory Liquidity Ratio

Statutory Liquidity Ratio or SLR is the minimum percentage of deposits that a commercial bank has to maintain in the form of liquid cash, gold or other securities. It is basically the reserve requirement that banks are expected to keep before offering credit to customers. The SLR is fixed by the RBI and is a form of control over the credit growth in India.

The government uses the SLR to regulate inflation and fuel growth. Increasing the SLR will control inflation in the economy while decreasing the statutory liquidity rate will cause growth in the economy. The SLR was prescribed by Section 24 (2A) of Banking Regulation Act, 1949.

Cash Reserve Ratio

CRR is an essential monetary policy tool used for controlling the money supply in the economy, a regulation implemented in almost every nation by the Central Bank of that country.

CRR rate is the minimum percentage of cash deposits (as specified by RBI) that must be maintained by every commercial bank as per the requirement of the Central Bank.

Cash Reserve Ratio Rate is computed as a percentage of the net demand and time liabilities of each bank. Net Demand and Time Liability is reached with the total of the savings account, current account, and fixed deposit balances.

Bank rate

Bank rate is a rate at which the Reserve Bank of India (RBI) provides the loan to commercial banks without keeping any security. There is no agreement on repurchase that will be drawn up or agreed upon with no collateral as well. The RBI allows short-term loans with the presence of collateral. This is known as Repo Rate. Bank Rates in India is determined by the RBI. It is usually higher than a Repo Rate on account of its ability to regulate liquidity.

Open market operations

Open market operations refer to the selling and purchasing of the treasury bills and government securities by the central bank of any country in order to regulate money supply in the economy.

It is one of the most important ways of monetary control that is exercised by the central banks. Under this system, the central bank sells securities in the market when it wants to reduce the money supply in the market. It is done to increase interest rates. This policy is also known as the contractionary monetary policy.

Similarly, when the central bank wants to increase the money supply in the market, it will purchase securities from the market. This step is taken to reduce the rate of interest and also to help in the economic growth of the country. This policy is known as the expansionary monetary policy.

Qualitative methods

Margin Requirement:

Margin requirement refers to the difference between the current value of the security offered for loan (called collateral) and the value of loan granted. It is a qualitative method of credit control adopted by the central bank in order to stabilize the economy from inflation or deflation.

Rationing of Credit:

Rationing of credit refers to fixation of credit quotas for different business activities which is introduced when the flow of credit is to be checked particularly for speculative activities in the economy.

Moral Suasion:

The central bank makes the member bank agree through persuasion or pressure to follow its directives which is generally not ignored by the member banks. The banks are advised to restrict the flow of credit during inflation and be liberal in lending during deflation.

Disinvestment is a philosophy of new economic policy of India. It is complete denationalization of assets. India adopted Disinvestment of government’s equity in PSUs and the opening up of closed areas to private participation. In recent years, the issue of privatization have been brought to the forefront due to the large scale fiscal deficits that the government has been facing.

The New Industrial Policy announced on 24th July, 1991, was an attempt to meet conditionalities imposed by IMF and World Bank in exchange of loan. The new economic policy was increasing the role and importance of the private sector in Industrial economy of the country and various measures were announced to achieve this purpose.

In August 1996, a five member Disinvestment was set up under the chairmanship of G V Ramakrishna former planning commission member and former chairman of SEBI with an aim to introduce mass ownership and promoting worker’s shareholding. The process was expected to eventually transform the existing state owned enterprises into public owned companies. Before measure the full fledged Disinvestment strategy; there are few terms of reference for the commission as to draw long term investment programme within 5 to 10 years for PSU referred it. To determine the extent Disinvestment in each PSU;prioritize PSUs referred to it by the core group terms if the overall disinvestment programme.

Source: Business Standard

To supervise the overall sale process and take decisions on the instrument as well as pricing. To select the financial advisors for the specified PSU to facilitate the investment process. Ensure the appropriate measures are taken during the investment process to Protect the interest of the affected employees.

Objectives of Disinvestment

The following objectives were stated in July 1991 are :-

• To improve overall economic efficiency

• To reduce fiscal deficit

• To diversify the ownership of PSU for enhancing efficiency of individual enterprises.

• To reduce the financial burden on the government.

• To improve public finance.

• To encourage wider share of ownership.

• To introduce, completion and market discipline.

• To raise funds for technological upgradation modernization and expansion of public sector enterprises

Rangarajan Committee on PSU Disinvestment, Krishnamurthy reconstituted in November 1992 with C Rangarajan as its chairman. To devise criteria for selection of public sector units for disinvestment during1992 – 1993. Advise on limits on the percentage of equity to be sold respect of each unit. To indicate the modus operandi of investment. Lay down criteria for valuation of equity shares of PSUs and make other recommendations related to disinvestment.

Methods of Disinvestment

The policy on Disinvestment has evolved considerably from the time of industrial policy of 24th July, 1991 stated that in order to raise resources and encourage wider public participation, a part of the government’s shareholding in the public sector would be offered to mutual fund, financial institutions, general public and workers.

When minority shareholding of the central government in 30 individual CPSEs was sold to select financial institutions. On recommendation of Rangarajan Committee in 1993 scope for investment continue to increase and evolve over the time To meet the targets traditional modes like IPO (Initial Public Offer) and FPO (Follow on Public Offer).

The government revived schemes like strategic sakes, made significant. Refinements in order to maintain sale through auction methods and over the time introduced new ideas like ETF for CPSEs to broader base choice alternatives available for Disinvestment.

Methods that adopted in 2017 – 2018 for investment

• Offer for Sale (OFS) the kind of sales shares by promoters through stock exchange mechanism adopting auction routes.

• Initial Public Offering are listed in CPSE or sales by government out of shareholding.

• Strategic Sale are substantial portion of the Government shareholding of a Central Public Sector Enterprise (CPSE) along with transfer of management control. Buy their own share by cash rich PSUs. Institutional Placement Program (IPP) only Institutions can participate.

• CPSE Exchange Traded Fund Disinvestment through ETF routes allows sale of government of India stake in various CPSEs across diverse sectors through a single product offering.

Indian economy is one of the developing economies in the world and is expected to reach new heights in the coming decades. But a sizeable population of this economy particularly the poor, underprivileged, disadvantaged and vulnerable group of people does not have access to most basic financial services. Formal lending agencies often left the poor unbanked on account of high levels of transaction cost incurred in lending to the poor. Their access to formal banking channels was constrained to their resource base as well as the nature of formal credit institutions. The demand for collateral security that a micro- borrower did not possess, the credit worthiness of the poor, high transaction cost due to difficulties in screening, and unattractive business proposition due to tiny savings and loans, were the deterrents faced by the formal lending institutions in loaning to the poor. Consequently, the poor continued to be dependent on informal sector lending, paying exorbitant rates of interest or underselling the product and their labor power to the creditor. Formal financial system was less accommodative to women.

The realization that this sort of unequitable development could not lead to the well -being of the society raised the need for financial inclusion. Financial inclusion is delivery of financial services like bank accounts, savings product, remittances and payment services, insurance, financial advisory services and micro credit to weaker sections in rural and urban areas at an affordable cost. It also involves actions to provide access to formal financial system like nationalized banks. Government of India and Reserve bank of India have taken series of measures and have experimented various alternatives to take financial services to the masses, but the task is stupendous, hence the pace of work should be accelerated and sustained. Since the formal banking system was limited to collateral based lending, there arose a need for developing a new system for financing the marginalized sections.

Microfinance by providing small loans and facilities to those who have been excluded from commercial financial services, has wider scope in the area of financial inclusion. The basic idea of microfinance is that poor people are ready and willing to pull themselves out of poverty if given access to economic inputs. The need for informality in credit delivery and easy access is denoted by the fast growth of microfinance providers in reaching out to small borrowers. The major microfinance providers in India are SHG-Bank linkage model, Non- Banking Financial Institutions and some trusts. Among these initiatives Self Help Groups have emerged out as an efficient alternative as they are uniquely positioned among the beneficiaries. Many of them operate over a limited geographical area, have a greater understanding among the rural poor, enjoy greater acceptability among the people and have flexibility in operations providing a level of comfort to their clientele. This fills the existing gap between formal financial networks and unfinanced poor weaker sections which is the intention of financial inclusion.

The SHG-bank linkage program gained extensive acceptance amongst NGO community and bankers. Establishing one million SHGs, the NABARD envisioned covering one third of the rural population in India. By the year 2002–03, promulgations were made for linking 200,000 SHGs. Visually perceiving SHG-bank linkage program emerging as a major way of banking with the poor in the ensuing years, the task force on microfinance estimated that at least 25,000 bank branches, 4000 NGOs, and 2000 federations of SHGs involving 0.10 million personnel of these institutions would scale up microfinance to a great magnitude.

For example, in Kerala, Kudumbashree Mission has emerged as one of the renowned Self-help group initiatives on a worldwide basis. Even though it was incorporated with the mission of women empowerment, it has grown out as source for economic empowerment for the marginalized sections of the society. It has outnumbered several other financial institutions in the case of provision of microfinance and has emerged out as a reliable tool for financial inclusion.

Business refers to the Organization or enterprising entity engaged in commercial, industrial or professional activities. Business activities have existed since ancient ages and over the period it has evolved according to the changes in its environment. Earlier it was limited to mere exchange of goods in return for other and then with the change in conditions it has reached to a stage where people could buy a good or avail a service from a seller who is miles apart even without face-to-face interface.

In the era of globalization, the scope of a business is very large. There are several examples of businesses growing into huge enterprises from a small virtual venture which even lacked a physical existence in its early stages. Similar to the steps of a ladder, there are several stages like local business, regional business, national business, international business and global business.

Local business

Local business is the first stage of a business enterprise and it exists in the limits of a locality. A local area comprises of surrounding neighborhoods, adjacent areas where native community lives. The local economy is the most primitive form of economy. It existed since ages. It focuses on a particular locality and acts according to the culture and traditions of the society. The customer base of a local business is very limited as its area of operation is only that locality.

Regional business

Regional business concentrates on different regions of a nation. A region is a unit on earth’s surface that has unifying and defining characteristics. It focuses on a regional area and provides a variety of commodities. It is a business between different areas within a country. Credit sales play an important role in this business. It helps in developing better quality infrastructure and transportation facilities

National business

National business is one that operates within the borders of a particular country. It has a business and customer base across a nation and understands the culture of the country. Since a national business has more locations than a local or regional business, it can be more competitive with its pricing. A nation is an organized political union of its member states.

International business

International business is business among different nations. Nations satisfy each other’s needs by supplying their surpluses and in return brings home the scanty resources. International means It means interaction between two or more nations. It is used as an analog to the word foreign.

Global business

It is a business which operates worldwide. It is the pinnacle of any business enterprise. Global means means entire Earth and not just one or two nations. It is synonymous to universal and worldwide. It has a wider scope than international business.

The basic idea to be imbibed from this topic is that no business becomes huge overnight. Just like human beings, a business also takes time to grow. Not all local businesses emerge out as global giants. Only those firms which could identify the changes in the environment and could act accordingly would be able to reach its pinnacle.

Kudumbashree, a community organization of Neighbourhood Groups (NHGs) of women in Kerala, has been recognized as an effective strategy for the empowerment of women in rural as well as urban areas: bringing women together from all spheres of life to fight for their rights or for empowerment. The overall empowerment of women is closely linked to economic empowerment. Women through these NHGs work on a range of issues such as health, nutrition, agriculture, etc. besides income generation activities and seeking micro credit.

Kudumbashree differs from conventional programs in that it perceives poverty not just as the deprivation of money, but also as the deprivation of basic rights. The poor need to find a collective voice to help claim these rights. Kudumbashree was conceived as a joint program of the Government of Kerala and NABARD implemented through Community Development Societies (CDSs) of Poor Women, serving as the community wing of Local Governments. Kudumbashree is formally registered as the “State Poverty Eradication Mission” (SPEM), a society registered under the Travancore Kochi Literary, Scientific and Charitable Societies Act 1955. It has a governing body chaired by the State Minister of LSG. There is a state mission with a field officer in each district. This official structure supports and facilitates the activities of the community network across the state.

KUDUMBASHREE MICROFINANCE

This system operates by encouraging women to form small homogenous groups under the SHG-bank linkage program. The members of these minute groups were encouraged to meet frequently and amass minute thrift amounts from their members. They were also taught simple accounting methods to enable them to maintain their accounts. Individually these poor could never have had enough savings to open a bank account. The first step in establishing links with the formal banking system opened up when the pooled savings enabled them to open a formal bank account in the denomination of the group. These were followed by frequent group meetings. Pooled thrift was utilized to impart lean loans to members for meeting their diminutive emergent needs saving them from debt traps/ money lenders who demanded unusually high rates of interest and accelerated their empowerment through group dynamics, decision-making, and funds management. Peer- screening effect was engendered as borrowers themselves undertook the task of credit evaluation and reduced the transaction costs, community members had much more preponderant information than banks. Peer monitoring effect induced group members to utilize their imprests in productive ways. The desire to preserve valuable ties induced borrowers to spend extra effort if compulsory to secure timely payments. These ties were valuable because they sanctioned members’ borrowing and provided business connections. Moreover, a very consequential feature of group-lending was the collateral effect. Gradually the pooled thrift grew and soon 11 they were adept in receiving external funds in multiples of their group savings. Bank loans enabled the group members to undertake income- generating ventures.

The various microfinance activities taken up by Kudumbashree are:

Thrift and credit operations

NHGs are instrumental in thrift mobilization, encouraging the poor to save and to avail low -cost formal credit. They facilitate easy and timely credit to the unreached. The amount of loan to members and the purpose for which the loan should be utilized are decided by the NHG. The repayment is collected weekly during the NHG meetings. It is estimated that the thrift mobilized is on an average Rs 40 per month per member.

Linkage Banking.

NHG-Bank linkage scheme is one of the flagship programmes of Kudumbashree. NABARD SHG-Bank linkage grading procedures are applied while selecting eligible NHGs for availing loan. The NHGs are rated on the basis of a 15 -point index developed by NABARD. Bank will provide loans to those NHGs who pass 80 % of marks in the grading.

Matching Grant.

Matching grant is an incentive provided to NHGs. This grant linked to amount of thrift mobilized, performance of NHG in the Grading and loan availed from banks. An amount of 10% of the savings of the NHG subject to a maximum of Rs 5000/- is provided as matching grant to each NHG. The grant is released based on their assessment rated using 15-point grading criteria developed by NABARD.

Interest Subsidy for Linkage loan.

Govt of Kerala has introduced a new interest subvention scheme to promote Bank Linkage Program among Kudumbashree Neighborhood Groups. Under this scheme all Kudumbashree NHGs are eligible for interest subvention to avail the loan facility at an interest rate of 4% on credit up to Rs. 3 lakhs. The interest subsidy would be provided as annual instalments to the NHGs.

KAASS.

KAASS, the Kudumbashree Accounts & Audit Service Society; is a homegrown enterprise to ensure proper account keeping in the community network. Each district has been furnished with a KAASS team that has been 12 drawn from commerce graduates and is guided by professional chartered accountants

Digitization of MIS’ and repayment Info System (E- SHAKTI)

Keeping in view the Government of India’s mission for creating a digital India, NABARD has launched a project for digitization of all Self -Help Group (SHG) in the country.

The Account Aggregator framework, introduced by the RBI, aims to make financial data more accessible by creating data intermediaries called Account Aggregators (AA) which will collect and share the user’s financial information from a range of entities that hold consumer data called Financial Information Providers (FIPs) to a range of entities that are requesting consumer data called Financial Information Users (FIUs) after obtaining the consent of the consumer.

For example, if a user wishes to apply for a loan, the lender (an FIU) will require access to the previous financial statements of the user – which reside with the user’s Bank (an FIP) – in order to check their creditworthiness. Here’s how an AA will facilitate the flow of information:

The FIU will request the AA to share the desired financial information.

The AA will request the user for their consent to share financial information with the FIU. The Account Aggregator must interact with the customer using either a web-based or a mobile app-based client.

If the user consents, the AA will request the FIP (the User’s bank in this case) to share the financial information.

The FIP will transfer the information, which will be encrypted, to the AA, which will then transfer it to the FIU.

Roles of each party:

Banks act as financial data providers. They supply the data required for Reserve bank of India to create a database of the account data and create reliable rankings.

Lenders act as financial data seekers. The lenders or financial institutions who provide fund to people acts as the seekers or demands the data aggregated by the Reserve bank.

Non-banking finance corporations act as mediums of communication between banks and lenders and they are the links.

Third-party service providers work with AAs.

Process

An individual or business opens an account with an account aggregator. Then, they link their bank accounts, insurance policies, etc. — which are accounts containing the customer’s financial data.

The customer can provide consent to a lender to access their financial data through the NBFC-AA.

After consent is provided, the account aggregator seeks permission from the financial data providers to access the customer’s data.

The data is sent to the account aggregator, which, in turn, empowers lenders to better evaluate the customer’s financial profile and risk associated with providing a loan.

Banks involved at present are:

These are the banks which act as the data providers:

State Bank of India

ICICI Bank

Axis Bank

IDFC First Bank

Kotak Mahindra Bank

HDFC Bank

IndusInd Bank

Federal Bank.

Advantages

Data scattered around the financial system can be made available under a single database.

This helps the institutions build a better understanding of potential customers and tailor their services accordingly.

It also enables the free flow of data between banks and financial service providers.

Helps financial institutions to make better assessment of creditworthiness of individuals and thus make better loan decisions.

Helps to eliminate the limitations of credit rating agencies.

Helpful for creditworthy customers

Disadvantages

It faces the issue of data privacy.

It is proposed as a self- Regulator framework, which would be an issue.

This data could be used for several other purposes.

The management of the finance of a state or whether Public authority endowed with taxing and spending power known as Financial administration. Efficiency and economy are two watch words of Public finance. Financial administration desire to raise, spend and account for the funds needs to fulfill the Public expenditure.

It involves the activities of “four agent executive” which needs and spend funds, that grants the funds and infuse them to particular ministries and departments of the Finance Ministry, that hold the strong bond on expenditure and audit; they will decide which fund use in what manner.

Financial administration of Government depicted as two main elements such as budgeting, financial control and fiscal & monetary policies. These elements incorporate a variety of subjects like various types of budget system, parliamentary financial control, delegation of financial powers, tax policies and tax administrative problem.

Scope of financial Administration

Source : CFO Share

Financial administration increasing it’s magnitude and complexity. It involves the discipline of economics, political science, commerce, management, statistics, philosophy and International Relations.

Fiscal policy, economic policy, fiscal planning, monetary policy , planning and management are parts of financial Administration. Constitutional law, financial administration, economy, socio – economic development are creating relation with Public Administration. To look at Administration of Public financial institutions and Public enterpriser. Budgeting performance and management accounting. Financial accounting and management accounting, financial auditing and management auditing are the wider version of financial Administration.

Financial administration at different levels and their interest relations at federal state and local states. Regulatory financial administration for regulating financial institutions by the private sector. Promote education, training and research in financial Administration. Ensure ethics and integrity of financial administration. Corporate Financial administration experience in developed and developing society. Financial control by the legislature, executives and judiciary.

Significance of financial Administration

Financial administration role is to ensure the economic growth of a country. It is more important for developing countries which increasing it’s socio – economic and infrastructural problems like poverty, unemployment and other economic related issues. Financial administration acquiring importance in the area of financial planning, protecting funds, improves standard of living, Allocation of funds, Economic Growth and stability and taxation planning.

Nature of Financial administration

Source : Unblast.com

Financial administration capture wider spectrum of development. Financial administration based on old and new economic methods that put forward the straight method for improving the economy. Financial administration conceive as a aggregate values of generation, regulation and distribution of monetary resources which is eligible for the sustenance and growth of Public organization.

Some scholars view this as traditional perspective, emphasis upon that set of Administrative functions in a public organization which relate to an arrangement of flow of funds as well as to regulating mechanism and processes which ensure proper and productive utilisation of these funds. The core of pure theory of Public finance us that Public finance should deal with the problem of Public income, Public expenditure and public debt in more practical way without any relation to a set of values and premises of the political party in power. As per to the intellectual of modern age, financial Administration is broad concept, it is an integral part of the overall management process of public administration except only raising Public funds. It discuss three important theories of Public finance i . e the socio political theory by (Wagner Edgeworth and pigou), the functional theory of Keynesian perspective and activiting view of modern Public finance theorists.

Financial inclusion may be defined as the process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups such as weaker sections and lower income groups at an affordable cost. Financial inclusion, broadly defined, refers to universal access to a wide range of financial services at reasonable cost. These not only include banking products, but also other financial services such as insurance and equity products.

INDICATORS OF FINANCIAL INCLUSION

As per the general laid down standards following are the key indicators of financial inclusion:

· Formal banking system

This refers to the existence and usage of banking services which are regulated by formal mechanism.

· Formal credit

The usage of formal or recognized credit providers indicates the presence of an inclusive financial system.

· Insurance

Apart from formal lending and depositing the citizens will also have access to proper insurance providers in a well inclusive financial system.

· Savings options

An inclusive financial system should provide attractive options to deposit the saved funds irrespective of the customer background.

· Modern banking

Each and every user should have access to modern banking services like electronic banking, mobile banking, internet banking, etc.

FACTORS AFFECTING FINANCIAL INCLUSION

Access to financial services have been recognized as an important aspect of development and more emphasis is given to extending financial services to low-income households. The lack of financial services limits the range of financial services and 7 credits for households. There are multiple factors which have affected the access to financial services, like

· Place of living

The area of operation of banks are limited to some specific geographical areas which leaves a significant portion of the rural population unbanked.

· Absence of legal identity and gender biasness

Due to lack of financial independence and unemployment there exists a bias on the basis of gender in having access to formal financial services.

· Limited knowledge of financial services

Illiteracy and lack of proper knowledge about banking system has led to reluctance towards formal banking practices among deprived classes.

· Level of income and bank charges

The charges and fines levied by banks make them less attractive for some classes of society.

· Rigid terms and conditions

Since formal banking system is subject to strict rules and regulations, many finds it difficult.

NEED FOR FINANCIAL INCLUSION

Financial inclusion broadens the resource base of the financial system by developing a culture of savings among large segment of rural population and plays its own role in the process of economic development. Further by bringing low -income groups within the perimeter of formal banking sector, financial inclusion protects their financial wealth and other resources. Financial inclusion also mitigates the exploitation of vulnerable sections by the usurious money lenders by facilitating easy access to formal credit.

India is a nation with a major chunk of the population living under vulnerable conditions. So, it is the duty each and every privileged section to lift the conditions of the underprivileged. Financial inclusion will pave a path of uplifting the society and empowering the people.

We all are consumers in some way or the other. Even before we are born, we are consumers and this cycle completes only after our death. In this era of consumerism, it is extremely difficult for one to not be a consumer and being a consumer is something to be ashamed of.

Even though being a consumer is not bad, exploitation by consumer is something to worry about. Unlike a socialist economy in a capitalist world, the producers produce what the consumers demand. So, the responsibility vested with the consumer is rising day by day. When a consumer makes an irresponsible choice, he is encouraging the producer to be exploitative. Realising this power of consumers, a new term has originated, green consumer.

Who is a green consumer?

A green consumer is a person who makes a wise choice. They buy a product or avail a service after considering the environmental impact. They check the components of the product, the environmental effects of the product and such aspects in detail.

Economic, social, and cultural forces have set the framework for green consumerism. This is because it is a social attitude and movement in the modern era, especially aimed at encouraging people to be more aware of the firms’ production processes and only to buy or use products and services that do not harm the environment. For this reason, green consumerism has created a balance between the buyers’ behaviours and the organizations’ profit objectives as it mostly based on the sustainable and pro-environmental behaviour of consumers.

Why is it important to be a green consumer?

From second half of the twentieth century, world has started its efforts for environment conservation. Even though commerce and industries are one of the largest contributors to environment degradation, they were the last to act for environment protection. One such arena is green consumerism. In a world which spins on the axis of consumerism it is important for a consumer to make environment friendly choices. Also, there is shift in the mindset of the businesses from seller centric to consumer centric approach. Recognizing this immense power vested with them consumers could influence the market to produce environment friendly goods. Also, the fact that environment degradation could lead even to the extinction of humankind has opened the eyes of general public.

How to be a green consumer?

Use paraben free products.

Use cloth bags and don’t demand plastic carry bags.

Promote organic goods.

Avoid using synthetic materials that could harm the world

Avoid pollutants while choosing products.

Use recycled products.

Avoid the practice of use and throw.

Give importance to energy efficiency.

Practice modern methods of environment protection.

Shop according to the need.

Minimize paper usage

Check energy labels in daily utility products

Avoid using bottled water

Reduce electricity consumption

Reduce your carbon footprint

Check for environment friendly certification.

Ultimately change of mindset is the most significant factor in green consumerism. It requires people to avoid certain comforts and embrace the difficult but fruitful path. It is the duty of consumers to influence the producers to shift towards a greener path. The consumer is the king in the present scenario. They should use their power for the good of the world.

Let us all strive to act green for a better future. We should lead a sustainable living and preserve what inherited for the coming generations.

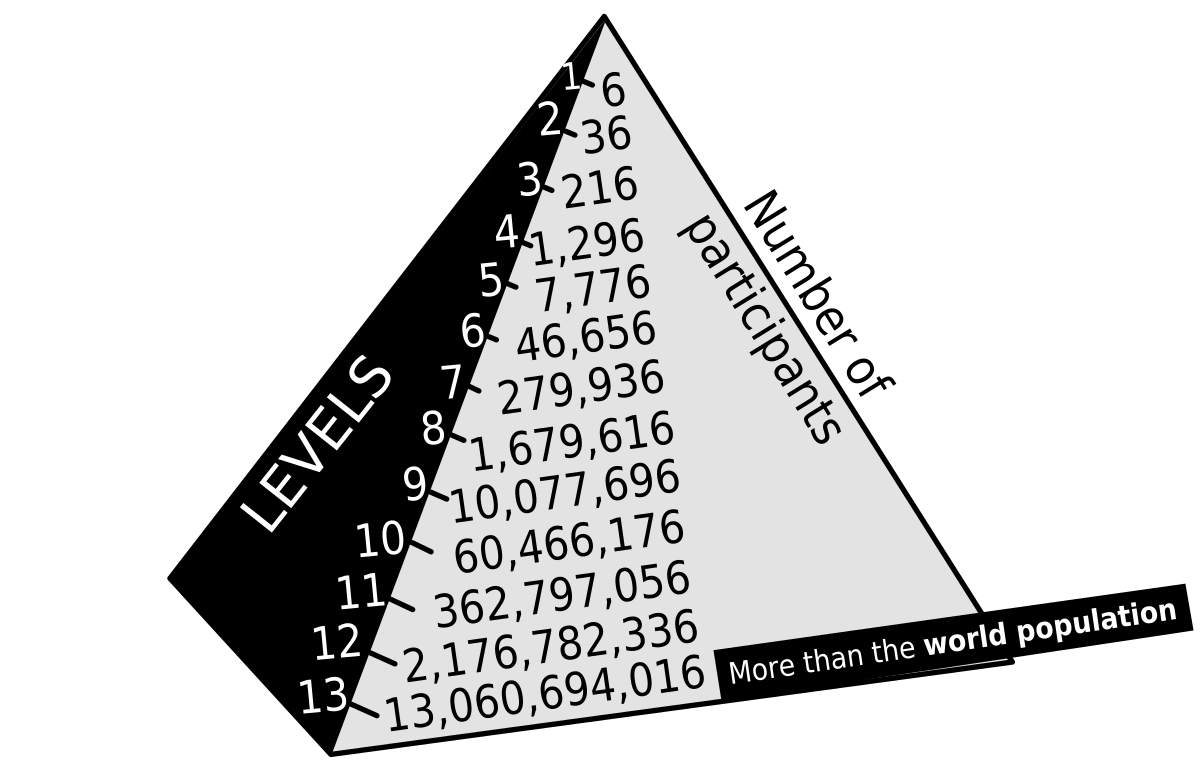

A pyramid scheme is a fraudulent system of making money based on recruiting an ever-increasing number of “investors.” The initial promoters recruit investors, who in turn recruit more investors, and so on. The scheme is called a “pyramid” because at each level, the number of investors increases. The small group of initial promoters at the top require a large base of later investors to support the scheme by providing profits to the earlier investors.

Let’s assume the following: Founder Mike sits alone at the top of the heap, represented by the number “one.” Assume Mike recruits 10 second-tier people to the level directly below him, where each newbie must issue him a cash payment for the privilege of joining. Not only do those buy-in fees funnel directly into Mike’s pocket, but each of the 10 new members must then recruit 10 tier-three members of their own (totaling 100), who must pay fees to the tier-two recruiters, who must send a percentage of their takes back up to Mike. According to the hard-sell pitches made at recruitment events, those bold enough to take the pyramid plunge will theoretically receive substantial cash from the recruits below them. But in practice, the prospective member pools tend to dry up over time. And by the time a pyramid scheme invariably shuts down, the top-level operatives walk away with loads of cash, while the majority of lower-level members leave empty-handed. It should be noted that because pyramid schemes heavily rely on fees from new recruits, the vast majority do not involve the sale of actual products or services with any intrinsic value.

Unfortunately, these types of scams sometimes prey on people who need income quickly. For example, if you lost your job and are having a hard time finding a new job, you might be more willing to look into an opportunity that offers a fast return. But avoid the temptation to overlook the feeling that something is too good to be true. Instead, take a moment to calm yourself so you can make a legitimate plan after losing your job. Go over your budget—or create one for the first time—so you can manage your money in the best way possible while you try to increase your income.

How to Spot a Pyramid Scheme

Pyramid schemes and MLM sound a bit alike, don’t they? Here are some signs of a pyramid scheme, provided by the US Securities and Exchange Commission, to help you understand whether you’re considering a scam or a legitimate MLM opportunity:

You’re not selling something real. Legitimate MLMs sell tangible goods—many times there’s a ready-made market for them.

Get-rich-quick promises. If you’re being offered overnight success, get-rich-quick guarantees, or passive income promises, it’s probably too good to be true. People who make money with legitimate MLMs put a lot of time and effort into their businesses.

The company can’t prove it generates retail income. If the business can’t show you financial statements that demonstrate income from the sale of product, it could be generating all its income from recruiting people into the pyramid.

Strange or unnecessarily complex commission processes. Legitimate MLMs have easy-to-understand, product-based commissions.

The Bottom Line

Pyramid schemes are illegal in many countries. The model of profiting by using the network effect often traps individuals into recruiting their acquaintances, which can feel slimy for everyone involved and can ultimately strain relationships. Some people may shoot their shot each time and invest in multiple schemes losing money each time. Victims of pyramid schemes are often embrassed into silence and keep blaming themselves for not being tenacious enough to earn the promised returns, when in truth it’s the system that is faulty. Get rich quick schmes never work and will allways have some strings attached to it that can put people into legal trouble. Vigilance and knowledge about where your money goes are important factors that people must know, preventing them from falling pray for traps like the pyramid scheme.

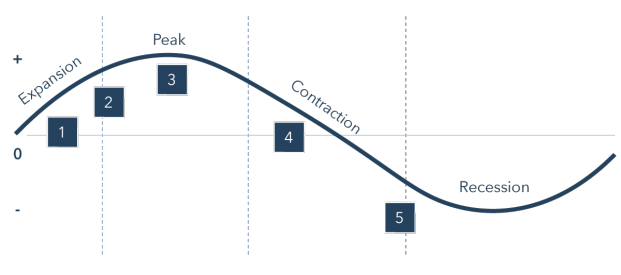

The National Bureau of Economic Research (NBER) defines a recession as “a significant decline in activity spread across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.” A recession is also believed to be signalled when businesses cease to expand, the GDP diminishes for two consecutive quarters, and the unemployment rate rises. The nature and causes of recessions are simultaneously evident and uncertain. Recessions are, in essence, a cluster of business failures being realized simultaneously. Firms are forced to reallocate resources, scale back production, limit losses, and, usually, lay off employees. Those are the clear and visible causes of recessions. There are several different ways to explain what causes a general cluster of business failures, why they are suddenly realized simultaneously, and how they can be avoided.

What Causes a Recession?

Some recessions can be traced to a clearly-defined cause. For instance, the recession of 1973-1975 began as a result of the 1973 oil crisis. However, most recessions are caused by a complex combination of factors, including high interest rates, low consumer confidence, and stagnant wages or reduced real income in the labour market. Other examples of recession causes include bank runs and asset bubbles.

Psychological Factors of a Recession

Psychological factors are frequently cited by economists for their contribution to recessions also. The excessive exuberance of investors during the boom years brings the economy to its peak. The reciprocal doom-and-gloom pessimism that sets in after a market crash at a minimum amplifies the effects of real economic and financial factors as the market swings. Moreover, because all economic actions and decisions are always to some degree forward-looking, the subjective expectations of investors, businesses, and consumers are often involved in the inception and spread of an economic downturn.

Economic Factors of a Recession

Real changes in economic fundamentals, beyond financial accounts and investor psychology, also make critical contributions to a recession. Some economists explain recessions solely due to fundamental economic shocks, such as disruptions in supply chains, and the damage they can cause to a wide range of businesses. Shocks that impact vital industries such as energy or transportation can have such widespread effects that they cause many companies across the economy to retrench and cancel investment and hiring plans simultaneously, with ripple effects on workers, consumers, and the stock market. There are economic factors that can also be tied back into financial markets. Market interest rates represent the cost of financial liquidity for businesses and the time preferences of consumers, savers, and investors for present versus future consumption. In addition, a central bank’s artificial suppression of interest rates during the boom years before a recession distorts financial markets and business and consumption decisions.

What Are the Indicators of a Recession?

Economists determine whether an economy is in recession by looking at a variety of statistics and trends. Factors that indicate a recession include:

Rising in unemployment

Rises in bankruptcies, defaults, or foreclosures

Falling interest rates

Lower consumer spending and consumer confidence

Falling asset prices, including the cost of homes and dips in the stock market

All of these factors can lead to an overall reduction in the Gross Domestic Product (GDP). The European Union and the United Kingdom define a recession as two or more consecutive quarters of negative real GDP growth.

Impact of Covid-19 Pandemic on the Economy

In February 2020, the National Bureau of Economic Research (NBER) announced that according to their data, the U.S. was in a recession due to the economic shock of the widespread disruption of global and domestic supply chains and direct damage to businesses across all industries. These events were caused by the COVID-19 epidemic and the public health response. Some of the underlying causes of the two-month recession (and economic hardship) in 2020 were the overextension of supply chains, razor-thin inventories, and fragile business models. The pandemic-related recession, according to NBER, ended in April 2020, but the financial hardship caused by the pandemic is still impacting Americans.

/is-it-multilevel-marketing-or-a-pyramid-scheme-2947159-FINAL-5f46e1d56e034223a43f045ed7b5ee23.jpg)

You must be logged in to post a comment.