In Urban Planning or Mapping: A street index is a reference list or map that organizes the streets within a particular area. This index allows people to easily locate streets based on their names, numbers, or grid system. It might be included in city maps, directories, or GPS applications, providing a comprehensive list of streets and their locations.

In Finance or Economics: A street index can sometimes refer to a benchmark or index that tracks the performance of a specific set of stocks or financial instruments, similar to the way the Dow Jones Industrial Average or S&P 500 tracks stock market performance. In this sense, “street” could be a shorthand reference to Wall Street or financial markets in general.

In Real Estate: A street index might be used to track property values, trends, or transactions specific to various streets within a city or region. This could be used by real estate professionals or analysts to measure the relative value of properties in certain areas.

In Postal Systems or Directories: A street index might be used in postal codes or address directories, helping individuals or delivery services quickly find specific streets based on postal codes or other identifiers.

If you meant a different concept by “street index,” please clarify, and I’d be happy to provide more specific information.

The details of the financial and passport related services primarily being provided by the post offices to the customers are attached herewith.

Scheme

Features

Post Office Passport Seva Kendras (POPSK)

Currently, providing the passport services at 442 Post Offices Passport Seva Kendras

Post Office SavingsAccount (POSA)

For regular savings, withdrawals etc.Min. balance – ₹ 500/- and ₹ zero in case of Basic Savings AccountATM / Internet & Mobile Banking Facility / NEFT & RTGSPost office Savings Accounts with India Post Payment Bank account linkage for UPI, IMPS etc.

Recurring Deposit (RD)

Min. instalment (per month): ₹ 100/- and thereafter any amount in the multiple of ₹ 10/-Max. instalment: No limitTerm: 5 Years and extendable for another 5 years

Time Deposit (TD)1/2/3/5 Year(s)

Min. Deposit (Single): ₹ 1000 /- or in the multiple of ₹ 100/-Max. Deposit: No limitIncome Tax exemption for investment in 5 Year TDExtension – Twice after completion of term

MonthlyIncome Scheme (MIS)

For source of monthly incomeMin. Deposit: ₹ 1,000/- or in its multipleMax. Deposit: ₹ 9.0 lakh /- (individual); ₹ 15 lakh (in Joint)Term – 5 Years

Senior Citizens Savings Schemes (SCSS)

Special scheme for Senior CitizensFor source of quarterly incomeMin. Single Deposit: Rs. 1,000/- or in its multipleMax. Deposit: Rs. 30,00,000/-Term – 5 Year and extendable after the expiry of each block period of three years

Public Provident Fund (PPF)

Min. Initial Deposit: ₹ 500/-Max. Deposit: ₹ 1,50,000/- in a Financial YearMin. Subsequent deposit in the multiple of ₹ 50/-Income Tax exemption for investmentTax free InterestTerm – 15 Years and extendable further

Sukanya Samriddhi Yojana Account (SSA)

Special Scheme for girl childrenMin. Initial Deposit: ₹ 250/-Max. Deposit: ₹ 1,50,000/- in a Financial YearMin. Subsequent deposit in the multiple of ₹ 50/-Income Tax exemption for investmentTax free InterestTerm – 21 Years

NationalSavings Certificate – VIII Issue (NSC)

Minimum investment – ₹ 1,000/-Maximum investment: No limit – In multiples of ₹ 100/-Income Tax exemption for investmentTerm – 5 years

Kisan Vikas Patra (KVP)

Minimum investment – ₹ 1,000/-Maximum investment: No limit – In multiples of ₹ 100/-Maturity – Double the amount of investment

Mahila Samman Savings Certificate (MSSC)

Special Scheme for Women and girl childrenInvestment is allowed from 01.04.2023 to 31.03.2025Minimum investment – ₹ 1,000/-Maximum investment: ₹ 2 Lakh per individual – In multiples of ₹ 100/-3 months-time-gap between the opening of accountsTerm – Two yearsLockup period – 6 months

PM Cares for Children Scheme 2021

Special scheme for the beneficiaries identified by Ministry of Women and Child DevelopmentInitially, 4515 accounts were opened and fundedInvestment differs based on the age of child and maturity amount is ₹10 LakhMIS Interest is payable on 10 Lakh from the age of 18 to 23Maturity at the age of 23 of the account holders.

India Post Payment Bank (IPPB)

Savings and current accounts Virtual Debit Card Domestic Money Transfer services Bill and utility payments Insurance services for IPPB customers

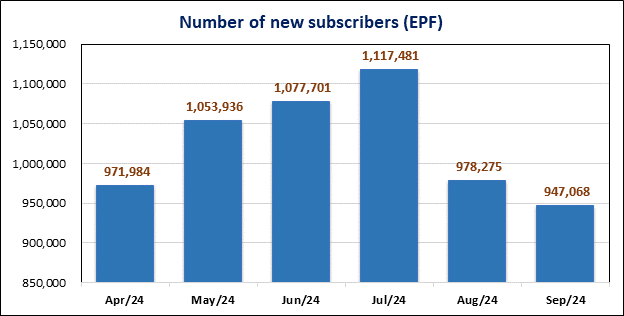

Ministry of Statistics & Programme Implementation is releasing the employment related statistics in the formal sector covering the period September 2017 onwards, using information on the number of subscribers who have subscribed under three major schemes, namely the Employees’ Provident Fund (EPF) Scheme, the Employees’ State Insurance (ESI) Scheme and the National Pension Scheme (NPS).

The total number of new EPF subscribers during the month of September, 2024 is9,47,068, which was 9,78,275during the month of August, 2024. The highest number of EPF subscribers 1,117,481 were added during July, 2024.

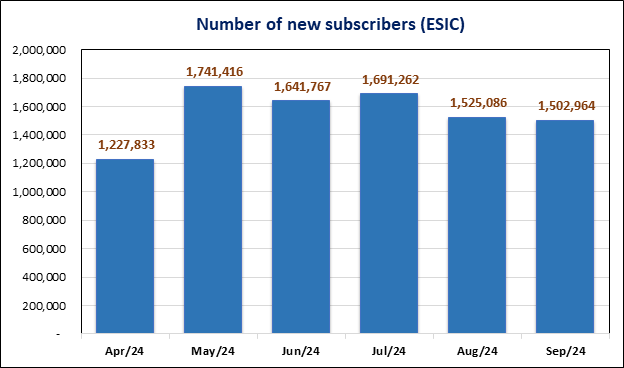

2.Employees’ State Insurance Scheme:

The newly registered employees and paying contribution under the ESI scheme during the month of September,2024 is 15,02,964which was 15,25,086 during the month of August, 2024.

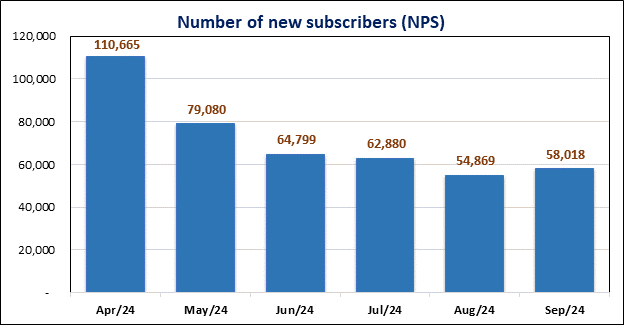

3.National Pension Scheme (NPS):

During September 2024, the NPS recorded a total of 58,018new contributing subscribers which was54,869 duringthe month of August, 2024.

Investing in value stocks has long been considered a prudent approach for investors seeking steady long-term returns. One effective way to gain exposure to a diversified portfolio of value stocks is through Value ETFs (Exchange-Traded Funds). These investment vehicles offer a cost-effective and convenient way to capitalize on the potential of undervalued companies. In this article, we will explore what Value ETFs are, their advantages, and how investors can benefit from them. Additionally, if you are starting to invest in crypto, you may consider knowing about strengthening communication.

Value ETFs are a type of exchange-traded fund that primarily focuses on investing in stocks deemed undervalued by the market. These funds typically follow an index that selects companies based on fundamental factors such as low price-to-earnings ratios, low price-to-book ratios, and high dividend yields. By investing in a basket of value stocks, investors can diversify their holdings and potentially achieve better risk-adjusted returns over time.

The Advantages of Value ETFs

Diversification: One of the key advantages of investing in Value ETFs is the instant diversification it offers. By owning shares in a single Value ETF, an investor gains exposure to a wide range of undervalued companies across different industries. This diversification can help reduce the risk associated with individual stock investments.

Lower Costs: Value ETFs are known for their cost-effectiveness. Compared to actively managed funds, which often charge higher management fees, Value ETFs typically have lower expense ratios. This means that investors can keep more of their returns, enhancing their long-term gains.

Less Active Management: Value ETFs are passively managed, meaning they aim to replicate the performance of a specific index. As a result, investors don’t have to worry about the fund manager’s active decisions, reducing the risk of human error and potential bias.

Long-Term Focus: Value investing is based on the premise that undervalued stocks will eventually realize their true worth over time. Therefore, Value ETFs tend to have a long-term investment horizon, aligning well with investors who are seeking sustainable growth rather than short-term speculation.

Considerations Before Investing

Before diving into Value ETFs, investors should conduct thorough research and consider the following factors:

Investment Goals: Assess your investment goals and risk tolerance. While Value ETFs are generally considered less volatile than growth stocks, they are still subject to market fluctuations. Investors should align their investment strategy with their financial objectives.

Expense Ratios: Compare the expense ratios of different Value ETFs. Lower expenses can significantly impact overall returns, especially in the long run.

Track Record: Review the historical performance of the Value ETFs you are considering. Past performance does not guarantee future results, but it can provide insights into how the fund has performed in various market conditions.

Fund Holdings: Examine the fund’s holdings to ensure it aligns with your investment preferences. Different Value ETFs may have varying concentrations in specific sectors or industries.

Diversification: Although Value ETFs provide broad diversification, consider how it complements your existing portfolio. Avoid over-concentrating in a single investment strategy.

Investing in Value ETFs with Online Platforms

For investors seeking to invest in Value ETFs, platforms offer a user-friendly and efficient way to access these investment vehicles. Through the platform, investors can easily research different Value ETF options, analyze their performance, and execute trades with just a few clicks.

Creating a Portfolio of Value ETFs

Selecting Multiple Funds: Diversification within Value ETFs can further reduce risk. Consider allocating funds across multiple Value ETFs to gain exposure to different value strategies.

Rebalancing: Regularly review and rebalance your portfolio to maintain the desired asset allocation. Rebalancing ensures that your investments remain aligned with your financial goals and risk tolerance.

Monitoring Performance: Keep an eye on the performance of your Value ETFs and the underlying holdings. While long-term investing is the primary focus, periodic evaluations help ensure your investments are on track.

Conclusion

Investing in Value ETFs can be a smart approach for investors seeking exposure to a basket of undervalued stocks. The benefits of diversification, lower costs, and long-term focus make Value ETFs an attractive addition to any well-rounded investment portfolio. Before investing, it is essential to conduct thorough research and consider factors such as investment goals and expense ratios. Online platforms provide a convenient way to access and invest in Value ETFs, making it easier for investors to implement their investment strategies effectively. By carefully crafting a portfolio of Value ETFs and monitoring its performance, investors can potentially unlock the rewards of value investing while managing their risk in a well-structured manner.

Property rights define the theoretical and legal ownership of resources and how they can be used. These resources can be both tangible or intangible and can be owned by individuals, businesses, and governments. In many countries, including the United States, individuals generally exercise private property rights or the rights of private persons to accumulate, hold, delegate, rent, or sell their property. In economics property rights form the basis for all market exchange, and the allocation of property rights in a society affects the efficiency of resource use.

Understanding Property Rights

Property is secured by laws that are clearly defined and enforced by the state. These laws define ownership and any associated benefits that come with holding the property. The term property is very expansive, though the legal protection for certain kinds of property varies between jurisdictions.Property is generally owned by individuals or a small group of people. The rights of property ownership can be extended by using patents and copyrights to protect:

Scarce physical resources such as houses, cars, books, and cellphones

Non-human creatures like dogs, cats, horses or birds

Intellectual property such as inventions, ideas, or words

Other types of property, such as communal or government property, are legally owned by well-defined groups. These are typically deemed public property. Ownership is enforced by individuals in positions of political or cultural power. Property rights give the owner or right holder the ability to do with the property what they choose. That includes holding on to it, selling or renting it out for profit, or transferring it to another party.

Acquiring Rights to a Property

Individuals in a private property rights regime acquire and transfer in mutually agreed-upon transfers, or else through homesteading. Mutual transfers include rents, sales, voluntary sharing, inheritances, gambling, and charity. Homesteading is the unique case; an individual may acquire a previously unowned resource by mixing his labor with the resource over a period of time. Examples of homesteading acts include plowing a field, carving stone, and domesticating a wild animal. In areas where property rights don’t exist, the ownership and use of resources are allocated by force, normally by the government. That means these resources are allocated by political ends rather than economic ones. Such governments determine who may interact with, can be excluded from, or may benefit from the use of the property.

Private Property Rights

Private property rights are one of the pillars of capitalist economies, as well as many legal systems, and moral philosophies. Within a private property rights regime, individuals need the ability to exclude others from the uses and benefits of their property. All privately owned resources are rivalrous, meaning only a single user may possess the title and legal claim to the property. Private property owners also have the exclusive right to use and benefit from the services or products. Private property owners may exchange the resource on a voluntary basis.

Private Property Rights and Market Prices

Every market price in a voluntary, capitalist society originates through transfers of private property. Each transaction takes place between one property owner and someone interested in acquiring the property. The value at which the property exchanges depends on how valuable it is to each party. Suppose an investor purchases $1,000 in shares of stock in Apple. In this case, Apple values owning the $1,000 more than the stock. The investor has the opposite preference, and values ownership of Apple stock more than $1,000.

Financial literacy is the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing. Financial literacy is the foundation of your relationship with money, and it is a lifelong journey of learning. The earlier you start, the better off you will be, because education is the key to success when it comes to money.

Read on to discover how you can become financially literate and able to navigate the challenging but critical waters of personal finance. And when you have educated yourself, try to pass your knowledge on to your family and friends. Many people find money matters intimidating, but they don’t have to be, so spread the news by example.

Understanding Financial Literacy

In recent decades financial products and services have become increasingly widespread throughout society. Whereas earlier generations of Americans may have purchased goods primarily in cash, today various credit products are popular, such as credit and debit cards and electronic transfers. Indeed, a 2019 survey from the Federal Reserve Bank of San Francisco showed that consumers preferred cash payments in only 22% of transactions, favoring debit cards for 42% and credit cards for 29%.

Other products, such as mortgages, student loans, health insurance, and self-directed accounts, have also grown in importance. This has made it even more imperative for individuals to understand how to use them responsibly. Although there are many skills that might fall under the umbrella of financial literacy, popular examples include household budgeting, learning how to manage and pay off debts, and evaluating the tradeoffs between different credit and investment products. These skills often require at least a working knowledge of key financial concepts, such as compound interest and the time value of money. Given the importance of finance in modern society, lacking financial literacy can be very damaging to an individual’s long-term financial success.

Being financially illiterate can lead to a number of pitfalls, such as being more likely to accumulate unsustainable debt burdens, either through poor spending decisions or a lack of long-term preparation. This in turn can lead to poor credit, bankruptcy, housing foreclosure, and other negative consequences. Thankfully, there are now more resources than ever for those wishing to educate themselves about the world of finance. One such example is the government-sponsored Financial Literacy and Education Commission, which offers a range of free learning resources.

Strategies to Improve Your Financial Literacy Skills

Developing financial literacy to improve your personal finances involves learning and practicing a variety of skills related to budgeting, managing and paying off debts, and understanding credit and investment products. Here are several practical strategies to consider.

Create a Budget—Track how much money you receive each month against how much you spend in an Excel sheet, on paper, or with a budgeting app. Your budget should include income (paychecks, investments, alimony), fixed expenses (rent/mortgage payments, utilities, loan payments), discretionary spending (nonessentials such as eating out, shopping, and travel), and savings.

Pay Yourself First—To build savings, this reverse budgeting strategy involves choosing a savings goal (say, a down payment for a home), deciding how much you want to contribute toward it each month, and setting that amount aside before you divvy up the rest of your expenses.

Pay Bills Promptly—Stay on top of monthly bills, making sure that payments consistently arrive on time. Consider taking advantage of automatic debits from a checking account or bill-pay apps and sign up for payment reminders (by email, phone, or text).

Setting financial goals is essential for personal finance management and budgeting. In order to efficiently manage spending, savings and investments and be financially secure, one must set financial goals.

Being unprepared and spending mindlessly can be quite risky. One should be as prepared as they can be in case of emergencies or financial crises.

Moreover, saving and investing your earnings can help you grow your wealth and utilise your earnings in a profitable manner.

Before setting goals

Financial goals and objectives can vary from person to person depending on their income, investments, expenses, life stage/age, needs etc. Hence, it is important to assess the objective and duration of the goal by following the steps mentioned below-

Identify starting point: Set a date for implementing the plan and its duration

Set priorities: Identify your objectives; Are you saving to invest or to buy or to set up an emergency fund?

Document your spending: Calculate your monthly expenditure. Analyse them and try to reduce them.

Pay down your debt:Reduce your debt and pay it off first to reduce your interest expenses.

Secure financial future: Implement the plan to become financially secure.

Most importantly, financial goals should be S.M.A.R.T – Specific, Measurable, Attainable, Relevant, Time-based.

Specific: Financial goals should be specific in terms of objective, time and amount.

Measurable: Goals should be measurable and expressed in monetary terms. For example, goal to be rich is not measurable as it is a subjective term. Hence, an amount limit suitable for every person should be set.

Attainable: A reasonable amount and time and limit should be set so it is possible to achieve them. For example, saving up to buy a car on a monthly salary of ₹30,000-₹40,000 within one year is not realistic and attainable.

Relevant: Every individual’s financial goal should be relevant to and in sync with their individual financial needs and objectives. For example, if a person wants to save up for retirement, they should focus on saving to invest in schemes specially designed for retirement planning.

Time-based: In order to achieve a goal, it should have an end period which motivates one to achieve it. They cannot be never ending as different stages of life have different financial requirements. At the end of the time period, one should evaluate and see if they were successful in achieving it or not.

Duration of Financial goals

As mentioned above, setting time-based goals is very important. Duration of each goal varies and is dependent on its nature and the income and expenses of the individual. For example, saving up to buy a TV should take between 3-6 months depending on the saving capacity of each individual. However, saving up for retirement takes years of planning, saving and investing.

Financial goals can be classified into Short-term, Mid-term and Long-term goals.

Short-term goals have a duration of 2 or less than 2 years. Example- Stick to weekly/monthly budget, reduce unnecessary expenses.

Mid-term goals have a duration of 2-years. Example- Build and diversify portfolio.

Long-term goals have a duration of more than 5 years. Example- Make a retirement plan and implement it.

In today’s world, it is very easy to confuse Insurance with Investment. One might feel that he/she is investing in their future and decreasing their future financial burden because he/she purchased an insurance policy. Let’s take a look at the definition of insurance and investment.

Insurance refers to a contract or policy in which an individual or entity receives financial protection or reimbursement against losses. It protects the insured against risk of losses or damage.

Investment, on the other hand, refers to an asset or item acquired with the goal of generating income or appreciation. For example, real estate, mutual funds, shares etc.

With the increase in types of insurance policies and persuasive insurance sales representatives, people tend to think of insurance as investments. However, Insurance merely provides protection in the event of loss, which may or may not arise. In case of no loss or damage, sum total of all the insurance premium paid is profit for the insurance company.

On the other hand, the main purpose of an investment is to generate income by providing returns (dividends and interest) and/or capital gains (value appreciation; increase in price). Insurance does not provide any substantial returns. It merely provides reimbursement in the event of loss/damage and therefore, it is not an investment.

Do you need Insurance?If yes, what kind?

Insurance planning is essential to protect against different kinds of risks and to be financially prepared in case of loss or damage to life or property. However, it should not be used a means to invest.

There are different types of insurance which can be broadly classified into Personal, Property and Liability. There are three types of insurance that you must have to protect against risk, not as an investment: Health insurance, Term life insurance and Automobile insurance.

Health insurance is a must to ensure that in case of an accident or injury, hospital and medical bills don’t eat away your savings.

Term life insurance ensures that in case of death of the earning member of the family, the family has enough to survive for a substantial period of time. Term life insurance has a fixed period and hence, has a very low monthly premium with a decent coverage. However, if the policy expires and the insured is still alive, the insured does not get any amount back. So, this policy should only be taken by the earning member at the right life stage in case he/she does not own enough assets to leave behind for his/her family.

Automobile Insurance (third party) is mandated by the Government of India on the purchase of a vehicle and hence, every vehicle owner should have one.

Other types of insurances sold and bought in the name of ‘investment’ like Endowment plans, Money back policy and the new policy called Unit-linked insurance plans(ULIP) which allows you to invest in the stock market should be avoided at all costs.

It is much more profitable to invest in the market through mutual funds or investor’s Demat account than to do the same through insurance companies. The rate of return in the market is much higher and it doesn’t cost as much as Insurance.

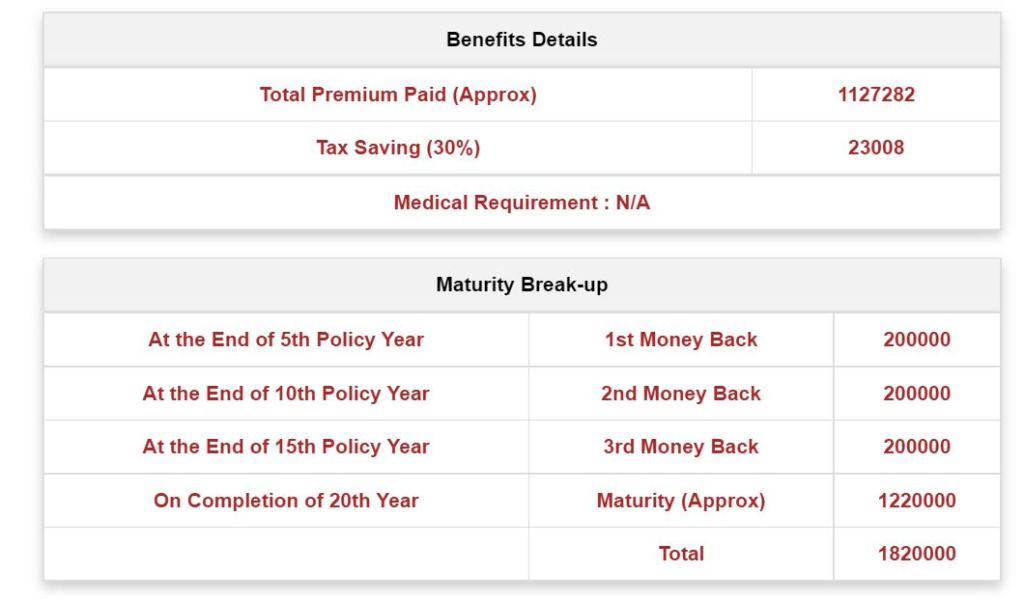

For example, if you buy Money Back insurance plan with a policy term of 20 years with ₹10,00,000 assured cover, the monthly premium calculated on LIC premium calculator comes out to be around ₹6300-6500 per month.

As calculated above, the total premium paid is ₹11,27,282 and the total amount received is ₹18,20,000. The total profit/return (approx.) is only ₹6,90,000 in 20 years. The return on investment (Return/Total Amount paid x 100) is only 61%.

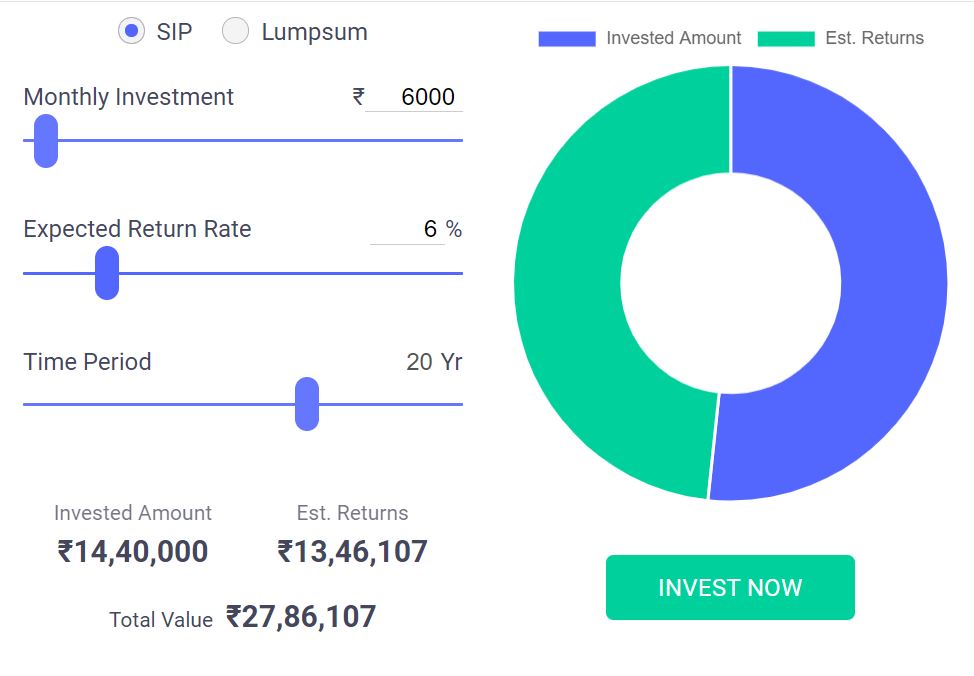

However, if the same amount is invested in SIP of any instrument with a return rate of just 6% for the same time period (20 years), the returns (calculated on Groww SIP calculator) are much higher.

₹6000 rupees invested monthly in any instrument with a return rate of only 6% for 20 years gives a return of ₹13,46,000 making the total value of the investment ₹27,86,000. The ROI (Return/Total Amount paid x 100) in this scenario is 93%.

Conclusion

Although Insurance is an essential part of Financial Planning to protect against different kinds of risks which varies from person to person, it should not be mixed with Investment. For greater returns and growth, investors should directly invest in the market or in any other instrument which suits their risk appetite and capacity.

You must be logged in to post a comment.